Square’s bets beyond a register brought in $253M last year as it posts a largely positive fourth quarter

By Matthew Lynley,

Square posted a largely successful fourth quarter that showed continuing growth with its Cash App — with users spending around $90 million on its Cash card in December, putting it on a potentially $1 billion run rate.

That would offer another significant avenue for Square to snap up additional customers as it looks to chip away at the alternatives available for directly sending cash between users. While popularized by Venmo, many companies have gone after this space — including Apple, where you can send money over iMessage — and its massive popularity through services abroad are showing the appeal for a company like Square. The rest of the report was largely above analyst expectations, though it got a slight dig for missing a near-term forecast for its earnings.

Square is looking less and less like just the point-of-sale system that it was when it went public, though that still accounts for a significant portion of its business. But as it diversifies into new services revenue, especially with new products like Square Capital and the Cash App, it’s finding new ways to sell a growth (and stability) story to Wall Street that’s so far delivered for its shares over the past year. Those subscription- and services-based components generated $253 million in 2017, according to the company.

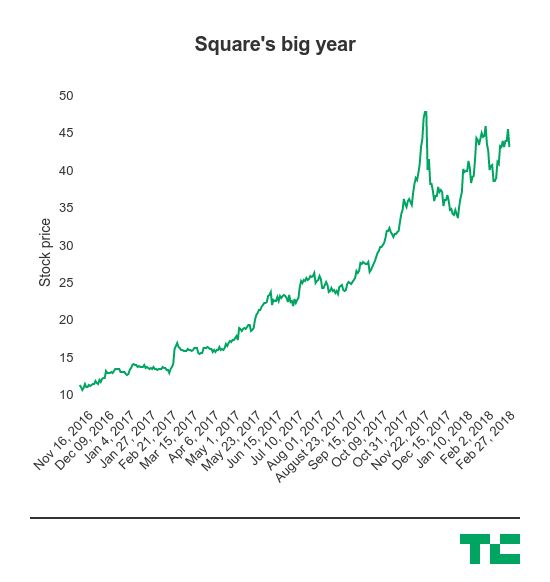

For the most part, the stock went nowhere after today’s earnings report, which more or less equates to a continuing run that’s sent its shares skyrocketing in the past year. Square’s shares have risen more than 150 percent over the past 12 months, sending it to a valuation north of $17.8 billion — a valuation wildly higher than its initial public offering when there were many questions about whether it could be a successful business.

Here’s the final slash line:

- Q4 adjusted earnings: 8 cents per share, compared to analyst expectations of 7 cents per share.

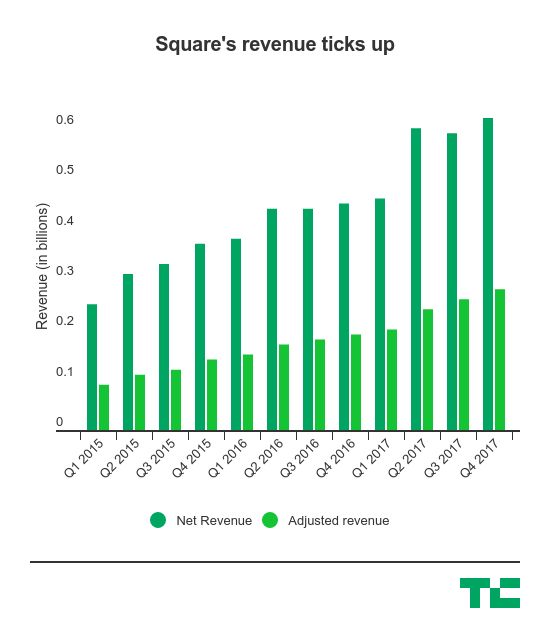

- Q4 adjusted revenue: $283 million, compared to Wall Street estimates of $266.3 million (up 47 percent year-over-year).

- Q1 revenue forecast: $292.5 million midpoint, compared to analyst estimates of $271.9 million.

- Q1 adjusted earnings forecast: 4 cents per share (midpoint), compared to analyst estimates of 8 cents per share.

- FY2017 subscription and services- based revenue (including Caviar, Cash and Square Capital): $253 million (up 95 percent year-over-year).

- Q4 gross payment volume: $17.9 billion (up 31 percent year-over-year).

- Cash App users: 7 million monthly active customers.

For one of the first times, as Square recently opened up bitcoin buying and selling in its Cash App, cryptocurrency operations are now falling under the “risk factors” for the company — a set of boilerplate statements made about the general risks it faces that it thinks it needs to disclose to investors. A significant part of that risk seems to stem from the evolving state of regulation around cryptocurrency. There’s a pretty meaty section in the risk factors in its main filing, which we’ve included below:

We recently introduced a feature to the Cash App that permits our customers to buy and sell bitcoin. Bitcoin is not considered legal tender or backed by any government, and it has experienced price volatility, technological glitches and various law enforcement and regulatory interventions. We do not believe that the bitcoin platform involves offering participants securities that are subject to the registration or other provisions of the federal or state securities laws. We also do not believe the feature subjects us to regulation under the federal securities laws, including as a broker-dealer or an investment adviser, or registration under the federal commodities laws. However, the regulation of cryptocurrency and crypto platforms is still an evolving area and it is possible that a court or a federal or state regulator could disagree with one or more of these conclusions. If we fail to comply with regulations or prohibitions applicable to us, we could face regulatory or other enforcement actions and potential fines and other consequences. Further, we might not be able to continue operating the feature, at least in current form, and to the extent that the feature is viewed by the market as a valuable asset to Square, the price of our Class A common stock could decrease. Additionally, there is no specific accounting guidance in U.S. GAAP covering accounting for cryptocurrencies, which means the accounting can be complex and subject to challenge or scrutiny. The final conclusions on the accounting treatment for our cryptocurrency transactions could affect the presentation of our results of operations.

Square’s revenue continued to grow at a pretty decent clip year-over-year, and we’re starting to see some trends of it beginning to look more and more healthy even as it looks to diversify its business beyond just its point-of-sale through services like the Cash App, its meal delivery service Caviar and Square Capital. Subscription revenue — which includes those services — accounted for $253 million in revenue, and Square Capital in the fourth quarter had 47,000 business loans totaling $305 million.