Meniga helps incumbent banks keep fintech fear at bay

By Steve O’Hear for techcrunch.com

A VC once told me that fear was the best sales tool ever invented. That was in reference to the hockey stick growth his cybersecurity startup was seeing, thanks to a raft of stories in the media regarding high profile cases of companies being hacked. But might the same be said of banks and the pending threat of fintech? Arguably, they have much to fear.

From having some of the most lucrative and low-hanging parts of their business unbundled by upstarts, such as TransferWise (money transfer), Nutmeg (savings), and PensionBee (pensions), to out right ‘challenger’ banks that are re-inventing the current account and will lend out customer deposits in the form of overdrafts, a business model at the core of traditional banking.

And then there is the biggest elephant in the room: big tech companies. If fintech is really about monetising access to a consumer’s financial data — access that the banks are being forced to provide by upcoming EU and U.K. open banking regulation — the likes of Google, Facebook, and, to a lesser extent, Apple and Amazon, can’t afford not to jump onboard the fintech train.

Enter Meniga, a London-headquartered fintech startup, with R&D in Iceland, that provides digital banking technology to some of the world’s largest banks. Its various products include a software layer that bridges the gap between a bank’s legacy tech infrastructure and a modern API, making it easier to build consumer-friendly digital banking experiences on top and to comply with upcoming regulation such as PSD2.

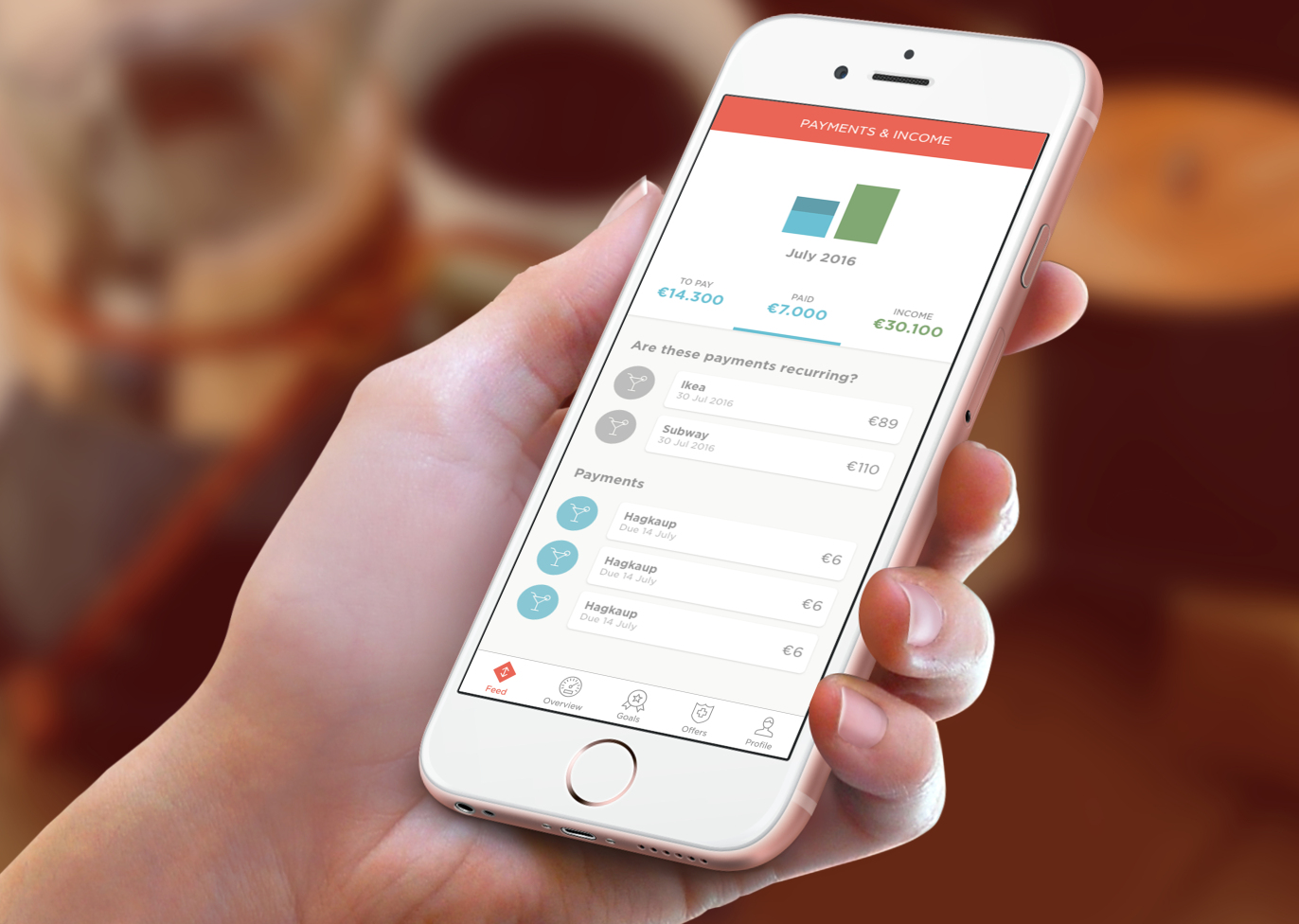

Those new digital banking experiences typically show up in a bank’s mobile app and include things like personal finance manager functionality, a Facebook-esque activity feed to help customers keep track of their spending, or the new Fitbit-inspired “Challenges” module, a kind of financial health tracker that harnesses social and gamification to gently nudge a bank’s customers into better budgeting.

“Today’s banks are under pressure to innovate and improve their customer experiences online and yet they are beholden to legacy processes and legacy systems and are usually ill equipped to provide their customers with world class user experience in digital banking,” Meniga co-founder and CEO Georg Ludviksson tells me.

“Meniga has built a reputation as a strong innovation partner to banks and its software solutions help some of the world’s largest banks utilise their data to make their online and mobile banking more personalised and inspiring”.

Ludviksson’s coining of Meniga as an “innovation partner” to banks isn’t simply startup speak, nor is it bluster (the Meniga founder talks in soft, considered Icelandic tones). The company holds five-day onsite design sprints with its banking clients, and last year it conducted more than 80 user testing sessions in four countries — again, many of them in partnership with the banks.

In addition, Meniga operates what Ludviksson says is a unique “sandpit” concept that sees the fintech startup offer a direct to consumer product for Icelanders that serves as a testing ground for product testing and R&D that in turn benefits its clients. “It’s a website with free personal finance tools with over 30 per cent of all Icelandic households registered. The site’s users are consumers from all walks of life with every personality type,” he says.

Meniga is also working with banks to introduce new data-driven services and business models. The idea is to enable digital banking users to “better understand, manage and make the most of their money” by providing personal finance tools, insights and tailored offers, such as via its card-linked offers product for merchants.

It’s a classic data play: give us access to your financial data and we’ll give you something of value in return. Banks, after all, sit on a heck of a lot of data, which they rarely do a good job of exploiting, for their own benefit or that of their customers. Meniga is helping to change that, whilst the task of trying to persuade banks to embrace a digital-first way of thinking before a new or old competitor does, is becoming a lot easier.

Meanwhile, the company, which counts the likes of Santander, Intesa, Commerzbank, ING Direct, and mBank as clients, has closed €7.5 million in new funding, bringing total raised to €21 million since being founded in 2009. The round was led by Nordic VC Industrifonden, with participation from existing investors Velocity Capital, Frumtak Ventures and Kjolfesta.