From BaaS and neobanks to FINTECH-BANK

By Vladislav Solodkiy, managing partner of a Singapore-based Life.SREDA VC

Fintech is currently undergoing a natural evolution stage. Previous three years were a «toothbrush» era: when you perform just one function, but better than anyone, and when you are irreplaceable and used every day. The long-awaited turning point came in 2015 when all services started merging with each other in some way.

The full presentation is here

And it’s understandable — if the first advanced customers were ready to bake a cake with disparate ingredients themselves, the mass customer wants to get a comfortable ecosystem of services with seamless integration allowing the customer to easily use data from one service inside the other and enjoy the benefits from their joint use.

Fintech companies around the world have now reached the potential of substituting almost any service from the banking value chain. The legitimate question to be raised then is: if there is a startup for each service a bank provides, do we really need banks? The banking industry has been and is a massive machine providing comprehensive financial services. Any bank nowadays can serve any financial need for the eligible population.

The word ‘eligible’ plays a vital role here. One of the core differences in approach to financial services between banks and fintech lies in democratization. Fintech companies often aim to serve a noble goal of global financial inclusion and making financial services more accessible for those not fitting into the credit score-based estimation of eligibility for another loan.

Putting aside the profitability factor, in 2016, fintech will become an extremely powerful vehicle that might be able to eat up even more of the banking profit than it ever was able to. While banks have always been looking to control the financial services industry, with the rise of fintech, the situation has changed drastically. Now banks are looking to collaborate with fintech so as to not to lose the links in the value chains that make them so powerful.

“In next 5 years we will see a completely different kind of financial service providers, providers who are customer focused and more agile in their services and processes”

What is important here is that major institutions are going after the fintech startups that are able to facilitate or substitute certain services in their value chain in a more cost-effective manner.

If we were to decompose a bank, there would be a fintech company that can substitute each service the bank provides. However, a single ‘problem’ remains – banks are still holding our accounts. In the most fatalistic prediction, a bank would be a back office organization maintaining an account, which is utilized by various fintech companies providing their services. So we still need a bank, but not for the reasons we needed it ten years ago. Over time banks may become sort of ‘warehouses’ bringing together fintech startups to serve each particular need of a customer.

1) Fintech-startups started to organize partnerships

In March 2016 US-based robo-advisor Wealthfront launched a new version (and vision) of its wealth management service. It integrated with tools like Venmo and Redfin to get an even more complete picture of its customers’ financial holdings. The integration, aimed squarely at millennials, is designed to help the robo-advisor come up with an even more tailored set of suggestions for investments to ensure financial health over time. It’s an interesting move, and one that positions the company to talk a better game to its core audience — the newly affluent, mid-to-late twenty- and thirty-something employees in white-collar jobs around the country.

In a blog post announcing the new features, Wealthfront chief executive Adam Nash wrote: “Wealthfront has been built from the ground up with the same social contract that is at the heart of fiduciary advisor: our clients trust us with the relevant details of their financial lives and we keep their information private and secure. Our advocacy for a fiduciary standard is based on the premise that it will lead to better far better advice and outcomes.” “The standard also sets the two companies apart from new lending companies like Earnest, CommonBond and a host of others vying for customers’ attention by managing a long-term financial commitment like a mortgage or student loans.”

German online-bank Fidor launched mPOS-acquiring with “European Square” SumUp.

Bangalore-based mPOS-startup Ezetap launched in October 2015 universal mobile wallet acceptance facility which enables such interoperability. This facility has been incorporated in the existing Ezetap Card Acceptance Platform and aims to offer merchants a unified one-stop solution for all payment acceptance. This new functionality is being launched with four of the large wallet providers in the country: Paytm, Mobikwik and FreeCharge.

“Mobile Wallet adoption has grown exponentially in India, mobile internet-connected “Smart points of sale” have unlocked new sectors to electronic payments, and the government is opening up the entire set of banking services through new technology,” the company said in a statement.

According to Vijay Shekhar Sharma, Founder & Chairman, Paytm the digital payments ecosystem is transforming the commerce experience for consumers and merchants. “Through our partnership, the Ezetap merchant base has the ability to accept payments from consumers who want to use Paytm,” he added.

![]() Zopa, the world’s first person to person (P2P) lender, recently signed a deal with Metro bank, a challenger bank in London started by Vernon Hill, who created Commerce Bank in the U.S. Metro. “This will allow the bank to lend its funds on our platform, a first of its kind in the UK,” wrote Zopa’s Mat Gazeley.

Zopa, the world’s first person to person (P2P) lender, recently signed a deal with Metro bank, a challenger bank in London started by Vernon Hill, who created Commerce Bank in the U.S. Metro. “This will allow the bank to lend its funds on our platform, a first of its kind in the UK,” wrote Zopa’s Mat Gazeley.

“This exciting development in the UK’s financial services industry is the first partnership between a UK P2P platform and a retail bank. The move will see Metro Bank receive a return by lending millions of pounds each month directly to UK consumers through Zopa.”

Zopa had previously announced a deal with Uber to help drivers buy their own cars. The alliance between Zopa and Metro will provide the lender with the funds it needs and attractive returns for Metro.

![]() Moven, Payoff and CommonBond are partnering to deliver digital financial innovation. Bank CIOs should accelerate the development of their own fintech ecosystems, partnering with disrupters to achieve digital transformation. The digital banking platform Moven announced partnerships with two online financial services providers: Payoff, which offers tools to help individuals pay down credit card debt; and CommonBond, which offers student loan refinancing tools.

Moven, Payoff and CommonBond are partnering to deliver digital financial innovation. Bank CIOs should accelerate the development of their own fintech ecosystems, partnering with disrupters to achieve digital transformation. The digital banking platform Moven announced partnerships with two online financial services providers: Payoff, which offers tools to help individuals pay down credit card debt; and CommonBond, which offers student loan refinancing tools.

Under the terms of the partnership, a Moven customer receives a $100 credit for opening a Payoff account, while a CommonBond customer receives a $200 credit and a 25-basis-point loan rate discount for paying via Moven. The Moven platform will be the primary customer experience for all three companies’ customers, offering tools and insights into financial management and goals. The Moven/Payoff/CommonBond partnership offers an interesting mix of services designed to appeal to customers who prefer to bank primarily through their mobile device and have credit card or student loan debt. Many of these customers will be younger and may not be aware of existing refinancing services from traditional banks. The incentives offered show that the partners recognize the need to motivate customers to use new services.

Also Number26, a Peter Thiel-backed German startup that’s setting out to create the bank account of the future, has announced a tie-up with London-based peer-to–peer money-transfer firm TransferWise. The partnership will give Number26 customers in-app access to a cheap international money-transfer service. “Our goal is to leverage the best banking products from around the world and make them accessible to customers with one tap, creating a fintech hub inside the Number26 app”.

Also Number26, a Peter Thiel-backed German startup that’s setting out to create the bank account of the future, has announced a tie-up with London-based peer-to–peer money-transfer firm TransferWise. The partnership will give Number26 customers in-app access to a cheap international money-transfer service. “Our goal is to leverage the best banking products from around the world and make them accessible to customers with one tap, creating a fintech hub inside the Number26 app”.

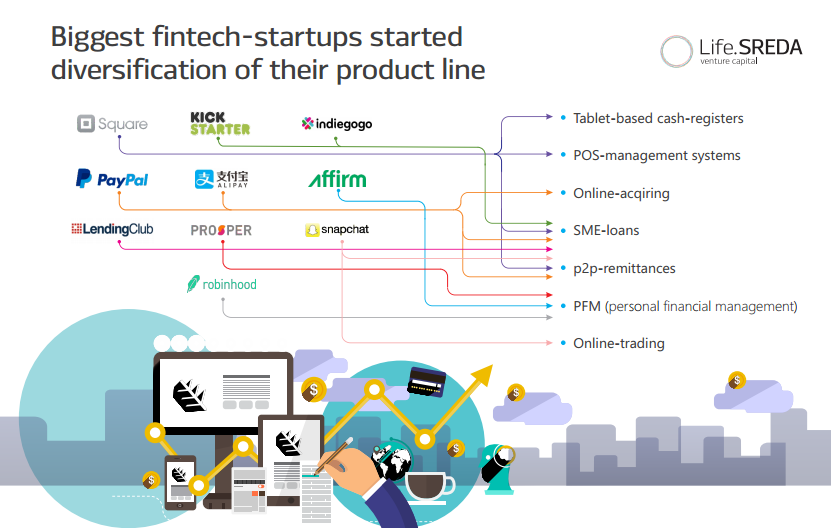

2) Biggest fintech-startups started diversification of their product line

The transition from individual services to ecosystem launched, when Square and other biggest fintech-companies have started the development of their ecosystems in 2014, this year they will further the integration of mPOS services, offline payments, loans, loyalty programs, analytical platforms and websites and applications constructors.

- mPOS-acquiring (Square, SumUp, iZettle, Payleven) going to SME-loans, p2p-remittances, tablet-based cash-registers and POS-management systems;

- E-wallets (PayPal, AliPay, Paytm) going from payments to consumer and SME- lending, online-remittances;

- P2P-lending (LendingClub, Prosper), Online-lending (Zopa, Kreditech, Avant, ZestFinance), Online-lending for students (Affirm, CommonBond, Earnest, WeFinance) going to SME-lending, car-loans, mortgage, refinancing, personal financial management (PFM);

- Crowdfunding (Kickstarter, IndieGogo) and Crowdinvesting (AngelList, RealtyMogul, Crowdcube, Coufenzi) going to SME- and p2b- lending;

- Messengers for millennials (like Snapchat) going to Personal financial management (like LearnVest) and Online-trading (like Robinhood and MotifInvesting).

- And Online-trading services going to PFM.

Square has started to think beyond what it can do in the commerce space. CEO Jack Dorsey acknowledged that his company wouldn’t be able to build everything, “so we opened up a bunch of APIs, and in that marketplace, for third-parties to actually build functionality and services that extend our ecosystem.” Build with Square compliments the company’s wide array of existing offerings. These include its App Marketplace, which showcases apps that work with the service, like Intuit QuickBooks, Xero, IFTTT, Stitch Labs, Bigcommerce, and Weebly.

Square has started to think beyond what it can do in the commerce space. CEO Jack Dorsey acknowledged that his company wouldn’t be able to build everything, “so we opened up a bunch of APIs, and in that marketplace, for third-parties to actually build functionality and services that extend our ecosystem.” Build with Square compliments the company’s wide array of existing offerings. These include its App Marketplace, which showcases apps that work with the service, like Intuit QuickBooks, Xero, IFTTT, Stitch Labs, Bigcommerce, and Weebly.

![]() Prosper, the marketplace lender focused on refinancing and credit rehabilitation, has re-launched its BillGuard PFM-app (acquired in September 2015 for $30M) under its own brand as Prosper Daily. The move brings the marketplace lender in line with a range of financial services companies that are offering one-stop windows into a user’s total financial history. The Prosper Daily app will offer BillGuard’s budgeting and spending tracking services, alerts for potential fraudulent charges, and credit monitoring. Prosper’s views the mobile app as a way to engage with potential customers even if those people can’t receive Prosper loans.

Prosper, the marketplace lender focused on refinancing and credit rehabilitation, has re-launched its BillGuard PFM-app (acquired in September 2015 for $30M) under its own brand as Prosper Daily. The move brings the marketplace lender in line with a range of financial services companies that are offering one-stop windows into a user’s total financial history. The Prosper Daily app will offer BillGuard’s budgeting and spending tracking services, alerts for potential fraudulent charges, and credit monitoring. Prosper’s views the mobile app as a way to engage with potential customers even if those people can’t receive Prosper loans.

“We turn away a lot of people from Prosper,” the company said. “We should be giving them this app so we can become a trusted partner in their financial life.” Ultimately, Prosper’s strategy is to expand its services through new mobile apps. That means the company could be coming up with new ways to deliver loans based on the financial information it gleans from the Prosper Daily app.

We expect the integration of PFM and PFP-systems, rating tools, the introduction of the possibility of direct account management and investment tools placement on platforms. In addition, existing and new platforms will actively sell financial products to their customers.

3) Open APIs integration and Bank-as-service (Baas) as a platform to unite & scale all fintech-services

Chris Skinner predicted this trend in 2009: “You’re probably all familiar with SaaS – it’s basically paying for applications as you use them, rather than buying them. These services used to cost you a fortune, but are now free or near enough. That’s where banking is going. Banking becomes plug and play apps you stitch together to suit your business or lifestyle. There’s no logical reason why Banking shouldn’t be delivered as SaaS.”

“What I’m really getting at here is that the old model of banking, where everything is packaged together around a deposit account with a cheque book, is bust. That’s why some banks are starting to white label and break apart their traditional services so that corporates can just buy-in the bits they like and want.” “This is the future bank, and old banks will need to reconsider their services to compete with this zero margin model.”

The traditional business models of Banks are being threatened by the small and agile fintech companies. “In next 5 years we will see a completely different kind of financial service providers, providers who are customer focused and more agile in their services and processes”.

Bankers for long made banking a complex process. Banks define the services and how those services will be served to the customer. Customer is at the receiving end. The status quo is being challenged, and their monopoly on how customer should conduct business is being questioned. In next few years, we will see banking-as-service model like any other service.

Traditional financial house will act payment and accounting engines, service will be build on top of those smaller traditional banks. Anyone can build customer centric service on top of the traditional banking system. This will provide customer bank agnostic services. Services will be pay per use. Customer will be free to pick and choose the service most suited to its needs. In any industry we look for building relationship when services are not transparent and simple enough to understand. Once a service is simplified, we aim to get things done. Building relationship is just an overhead. No one visits a bank to build relationship, customer builds relationship with the bank so that he can do business with ease. If he will get the same ease via different platform then why will he stick to the traditional banking model.

One of the best examples of BaaS is The Bancorp (75,000,000+ prepaid cards in U.S. distribution, 100+ private-label non-bank partners, including Simple, $232 billion combined annual processing volume). “From the start, we’ve spent most of our time and efforts behind the scenes, putting the companies who work with us – and their goals – first.

One of the best examples of BaaS is The Bancorp (75,000,000+ prepaid cards in U.S. distribution, 100+ private-label non-bank partners, including Simple, $232 billion combined annual processing volume). “From the start, we’ve spent most of our time and efforts behind the scenes, putting the companies who work with us – and their goals – first.

We’ve remained in the background, offering them the guidance, innovative thinking, and operational support they need to succeed.” “Today we’ve grown far from our roots as a branchless commercial bank to become a true financial services leader, offering private-label banking and technology solutions to non-bank companies ranging from entrepreneurial start-ups to those on the Fortune 500.”

Another BaaS-company – Singapore-based MatchMove. This concept was put into practice also by Open Bank Project. The UK government promotes the use of open data and open API in the banking and supports the exchange of information between financial institutions. Within the framework of the state initiative, the first private company will be able to create a service that combines customer data from different banks by April of 2015. The initiative called Midata has been implemented in the UK for the past few years and is aimed at opening access of citizens to information about themselves from different public and private institutions, including banks.

Another BaaS-company – Singapore-based MatchMove. This concept was put into practice also by Open Bank Project. The UK government promotes the use of open data and open API in the banking and supports the exchange of information between financial institutions. Within the framework of the state initiative, the first private company will be able to create a service that combines customer data from different banks by April of 2015. The initiative called Midata has been implemented in the UK for the past few years and is aimed at opening access of citizens to information about themselves from different public and private institutions, including banks.

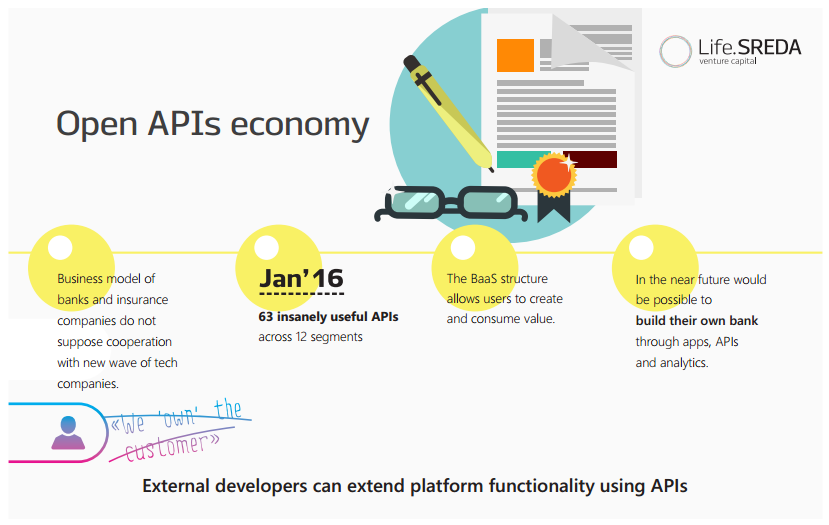

One of key development of 2015 has been the open sourcing of bank services. Chris Skinner wrote: “I’ve talked for a while now about ‘banking as a service‘ (BaaS) – first blog entry almost seven years ago – and this forecast that anyone in the near future would be able to build their own bank through apps, APIs and analytics. The core of this view was based on banking processes becoming open sourced through APIs, and in 2015 it’s finally happening. It hasn’t happened yet – this is an ongoing process – but it’s definitely happening and is taking place in three forms: voluntarily, customer demand and regulatory action.” Key protagonists of open sourcing the bank include Fidor and BBVA.

In December 2015 LetsTalkPayments.com counted 63 insanely useful APIs from fintech-startups across 12 segments “to supercharge your product”. APIs are the infrastructure that developers use to build applications to access content and other services. As FinTech startups continue to disrupt traditional financial services, banks are also waking up to the fact that offering an open API—where developers can latch on and create very specific customized app solutions—is the way to engage and retain their customers in the future.

David Brear, Chief Thinker at Think Different Group and partner at Life.SREDA BB Fund, and Pascal Bouvier, Venture Partner at Santander InnoVentures, thought, that the integration and delivery of financial services is changing as new channels, products and partnerships are being explored, and Banking as a Platform (BaaP) is one of the alternatives. There are three main reasons why financial services industry incumbent did not organize as platforms.

Current Business Models – Banking and insurance company business models do not currently lend themselves to network effects. Up until recently, banks and insurers were the perfect intermediaries. They were the best positioned to make credit or underwriting decisions. Why create a platform with partners when no one else knows how to lend or insure better than the current players? Third one: “We ‘own’ the customer”.

Up until now, how individuals or corporations interacted with one another and between themselves lent itself to a top down organization for the selling of financial services. If the industry owns the narrative of how a financial product gets pushed to an end user, why create a platform with partners? Without fintech competition, financial services industry incumbents would still need to think about platform strategies, as the root causes are much more fundamental than that.

Financial services industry incumbents need to transform into “fintech incumbents,” with a complementary platform business model to better compete. For a bank or an insurance company to become a platform for financial services, profound transformations need to happen. Becoming a “digital bank”, if taken in the strictest sense of the term (i.e. bringing distribution channels to the digital realm) is not enough. It is clear that any success in developing a platform strategy for banking (BaaP) will be largely dependent on wholesale cultural and technology mindset changes.

Traditional business models are far easier since banks are in full control. Financial services industry incumbents created products and sold them to their customers. Value was produced upstream by the banks and consumed downstream by the consumer. The BaaP structure allows users to create and consume value. At the technology layer, external developers can extend platform functionality using APIs. At the business layer, users (producers) can create value on the platform for other to consume.

In March 2016 offering what it calls Banking-as-a-Platform, FinLeap, the German fintech ‘startup factory’, has hatched its latest venture. This time the Berlin-based company builder (to use the preferred terminology) is investing and betting on the underlying regulatory and financial technology infrastructure — the picks ‘n’ shovels, if you will — in the form of solarisBank, a fully licensed digital bank designed to power an array of fintech services.

In March 2016 offering what it calls Banking-as-a-Platform, FinLeap, the German fintech ‘startup factory’, has hatched its latest venture. This time the Berlin-based company builder (to use the preferred terminology) is investing and betting on the underlying regulatory and financial technology infrastructure — the picks ‘n’ shovels, if you will — in the form of solarisBank, a fully licensed digital bank designed to power an array of fintech services.

Born out of the frustration experienced by FinLeap’s own startups when faced with the need to piggybank an existing banking license and technology in order to be able to offer various financial services, solarisBank has developed what is described as a modular-based banking toolkit, including, and crucially, various modern banking APIs. This means that it’s able to offer other fintech businesses various services that, in turn, they can offer to their own customers. These include account and transaction services, compliance and trust solutions, working capital financing, and online loans. Those services not only require a technology solution, but in many instances, a banking or e-money license too.

“We are confident that most major Internet companies will want digital banking solutions that expand their product range and offer it within a challenging regulatory environment,” says FinLeap Chair Jan Beckers in a statement. “We haven’t seen a bank that offers a technology platform like ours and can partner with so many different kinds companies and business models.”

The frictionless and straight-forward integration enables solarisBank partners to launch quickly and concentrate on their core business. In addition to the focus on technological innovation, we meet or exceed all regulatory requirements with our full bank license.”

Also, BaaS-companies can help fintech-startups with expansion to other countries. Unlike startups in other fields such as taxi aggregators (think Uber) or productivity apps that expanded very quickly across the globe, it is difficult for fintech companies to do the same. Since technological advancements allow companies to operate globally even while being physically located in one country, it presents a great opportunity to grow revenues through global expansion.

As the barriers are higher for global expansion, very few (about 25) fintech startups have successfully managed to expand globally. Factors that contribute to or decide the success of global expansion for a fintech startup include regulations, market opportunity, professional network, success in the home country, working with local industry bodies, local ecosystem, competition and flexibility of business models. Out of all these factors, regulations play a very critical role. When a startup’s business model revolves around payments, the FinTech startup has to devise a plan to smartly enter the market while following the regulations in the foreign country/continent. Many FinTech startups have also expanded globally via partnerships with other companies in the foreign country or by winning big clients in the foreign country.

4) Neo- and challenger banks as front-end of aggregation movement

If bank-as-service companies can be back-end for integration of standalone independent fintech-startups, neo- or challenger banks could be their front-end for end-users.

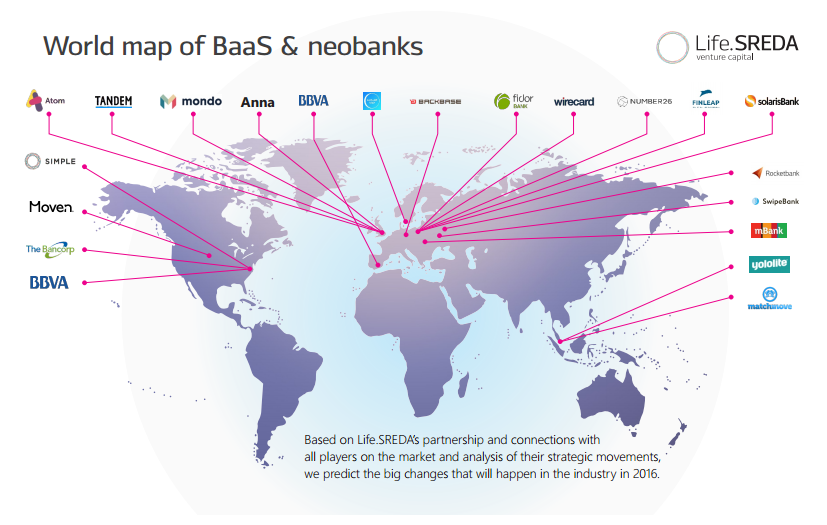

Earlier, when we talked about “mobile banking” – we meant Simple and Moven, and their competitors, or rather “followers” of the “first wave”. But now there is a second wave of interest about this topic. Atom (UK), Tandem (UK), Secco (UK), Mondo (UK), Monese (UK), Starling (UK), Anna (UK), Number26 (Germany), LunarWay (Denmark), Fidor (Germany and UK) – this time, the focus is not for the United States, but for the United Kingdom. It happened there after a number of local regulator steps to stimulate the emergence of new players and their licensing. Many interesting teams with great experience and ideas came to the flow.

German Number26 plans to systematically “rebundle” and create tight-knit integrations with other startups that focus on one specific vertical. What this could effectively mean is that through your Number26 bank account, you could access TransferWise’s cost-cutting currency exchange service, or perhaps even a Robin Hood-style stock investment service. “Our vision from the start has been to build Europe‘s first bank account for the smartphone,” added Number26 CEO and founder Valentin Stalf. “We see traditional banks as having failed to adapt to the demands of the digital generation. The response to Number26 has been fantastic and we‘re thrilled to expand to further markets.”

German Number26 plans to systematically “rebundle” and create tight-knit integrations with other startups that focus on one specific vertical. What this could effectively mean is that through your Number26 bank account, you could access TransferWise’s cost-cutting currency exchange service, or perhaps even a Robin Hood-style stock investment service. “Our vision from the start has been to build Europe‘s first bank account for the smartphone,” added Number26 CEO and founder Valentin Stalf. “We see traditional banks as having failed to adapt to the demands of the digital generation. The response to Number26 has been fantastic and we‘re thrilled to expand to further markets.”

In addition to personal banking and savings, British Atom aims to offer other services such as business banking, loans and mortgages, and potentially some kind of social media forum that it describes only as “shared wisdom” for the moment on its site.

In addition to personal banking and savings, British Atom aims to offer other services such as business banking, loans and mortgages, and potentially some kind of social media forum that it describes only as “shared wisdom” for the moment on its site.

British Tandem’s founder Ricky Knox said the aim is to differentiate the bank from the rest of the market by using customers’ data to offer good deals on the money they spend, such as utility bills as well as on financial products.

British Tandem’s founder Ricky Knox said the aim is to differentiate the bank from the rest of the market by using customers’ data to offer good deals on the money they spend, such as utility bills as well as on financial products.

![]() British Mondo has an open API from the get-go, part of a wider differentiator that’s seeing it build a “full-stack” bank with its own in-house banking tech in order to offer features that legacy banks struggle with as they are reliant on outdated software and infrastructure. “We’ve had hundreds of people attend our hackathons and they’re now some of our biggest supporters. It’s also great for recruitment!” Mondo’s CEO says.

British Mondo has an open API from the get-go, part of a wider differentiator that’s seeing it build a “full-stack” bank with its own in-house banking tech in order to offer features that legacy banks struggle with as they are reliant on outdated software and infrastructure. “We’ve had hundreds of people attend our hackathons and they’re now some of our biggest supporters. It’s also great for recruitment!” Mondo’s CEO says.

![]() Matthias Kroener, German Fidor’s chief executive, says it is more like a social network than a traditional bank, with online communities offering finance tips, peer-to-peer loans and financial market trading facilities. German bank Fidor – derived from the Latin word for trust – launched in Germany in 2009 and has offices in Berlin and Munich, as well as five staff in London (Fidor launched in September 2015 the UK).

Matthias Kroener, German Fidor’s chief executive, says it is more like a social network than a traditional bank, with online communities offering finance tips, peer-to-peer loans and financial market trading facilities. German bank Fidor – derived from the Latin word for trust – launched in Germany in 2009 and has offices in Berlin and Munich, as well as five staff in London (Fidor launched in September 2015 the UK).

In its home market, Fidor offers 25 different products, including brokerage services, precious metals trading facilities, crowdfinancing offers and even peer-to-peer loans, where customers can post on the online community that they want to borrow money, which other customers can offer to lend to them. Matthias Kröner described the approach as “a marketplace, shielded by a banking licence.”

The digital bank is unusual for two reasons — firstly, it puts a big emphasis on the idea of “community” in banking. Its message board is a key part of its offering and it encourages customers to request services, changes, and offer advice to other customers. Secondly, it’s built more like an app store than a traditional bank.

In Germany, Fidor offers core banking services but partners up with other companies to offer things like peer-to-peer loans and foreign exchange transfer.

There are several unique selling points offered by new banking players, and it presents many amazing opportunities: Mobile first; Cross-sell and up-sell; Virtual financial advisor; Data driven. I think, that it is a great opportunity for investors especially Asia to be in touch with innovative solutions in mobile banking.

This can be seen as we have achieved prior successes through exits in our first fund — Simple, Moven, Rocketbank. Developing markets like Southeast Asia fit the prerequisites for this to kick off, given their large amount of underbanked and unbanked consumers who have access to smartphones as well as low rates of home broadband and urbanization that make traditional methods inaccessible to them.

Beside Singapore in the region, the digital banking penetration is depressingly low, ranging from 13-44 percent in 2014 — even though consumers in their 20s are 50 percent more willing than their parents to try mobile banking. If banks are unable to continue to rapidly innovate and create new, user-friendly and differentiated mobile offerings and effectively advertise and distribute on these platforms, they could lose market share to existing competitors or new entrants, and their future growth and bottom line could adversely take a hit.

In other words, banks have to start disrupting themselves by acquiring new technologies and/or partnering with technopreneurs before they become a part of history. The winners will be the ones that put consumers’ digitalized lifestyles as the core strategy.

Next step: Fintech-bank as a unique bundle of independent fintech-startups

Australian-based Tyro Payments chief executive Jost Stollmann wants to see the emergence of a new financial services economy run by innovative companies that create services that work with each other. He wants fintech entrepreneurs to work together against the large banks, which he believes will use their investments in start-ups to slow innovation. Instead of hoping their businesses will be bought and adopted by big banks, he said they should aim to take the banks’ customers and revenue. “I call this the ecosystem,” he said.

“Then we can get to the critical scale and scope to disrupt the establishment. Cuddling up with banks and thinking about exit and your beach house is not helpful.” The industry is debating if financial services start-ups should work with banks to help them improve their own products and customer service, or to scale up independently of incumbents and try to compete with them. Rather than collaborating, start-ups should “compete head-on with the majors by providing new solutions and co-operating with their peers”, Mr Stollmann said.

Banks worry about a super aggregator who takes away the customer, leaving them to compete on price while the value cream is taken up by the super aggregator. Enough has been written about who the possible super aggregators could be and quite a bit has been written about the potential ‘Uberization’ of banking. The banking response could have more to do with Tesla than Uber.

Consider this: Tesla is the world’s most famous electric car (Prius, my apologies, but after Model 3, do you really want to debate this?), but it’s actually a little bit more than that. It’s a stylish, environment friendly mobility platform. Tesla has introduced constructs such as firmware and over-the-air software updates to the automobile lexicon, and the reason these are so popular is because now the car has been reimagined as a mobility platform.

And before you think that this is about self-driving cars, it isn’t. In the short-term, this is just one of the exponentially improving capabilities a Tesla car has. The real experience of Tesla includes the value it’s trying to provide to the customer – of being connected. This value is delivered at the individual car and driver level, and the collective learning from all cars that Tesla sells. It is at once a platform that iteratively adds value to the core product while learning what it is that it can learn from the use of its vehicles.

We can use while undertaking digital transformation assessment is to use the customer journey as the lighthouse towards which the value chain transformation ship comes to deliver superior customer experience. Post the digital readiness step, which is essentially ‘Digital 1.0 Banking’, the bank is ready for multi-dimensional learning. At its most basic, it’s about:

- Empathetic understanding of customer journeys – including a deeper understanding of the customer journey for existing products;

- Reinvention of the value chain that services the customer journey – truly remarkable organizations have restructured themselves around customer segments and have transformed how the value chain delivers for the customer and the organization. Post-Digital 1.0, the value chain includes an ever increasing ecosystem of partners and syndicated data systems that can potentially add hitherto inconceivable value to the customer journey.

If you ask a typical banker, the customer journey definition will entail the bank being able to trace the customer across all its channels; the old-new seamless omni-channel interaction challenge. This is a product-value-proposition-centric view. And yes, banks need to solve this, but it isn’t the customer-obsessed view. The difference is the chasm between provisioning a product conveniently versus satisfying needs. It’s a lifetime view.

If you refer back to the digital transformation framework, the ‘Y’ is called a value ecosystem. This is for a reason. It’s not feasible or viable (and perhaps even necessary) for a bank to provision every product or service that a customer may need, but it can very well be the channel through which the product is provisioned by another party. Platforms will be about ‘coopetition’ as much as they are about competition.

Philippe Gelis, CEO at KANTOX, told: “The second wave of fintech, to come in two to five years’ time, will be “marketplace banking” (or “fintech banks”). This will be a type of bank based on five simple elements:

1. A core banking platform built from scratch;

2. An API layer to connect to third parties;

3. A compliance/KYC infrastructure and processes;

4. A banking license, to be independent from other banks and the ability to hold client funds without restrictions;

5. A customer base/CRM, meaning that the fintech bank will have the customers, and a customer support team.

The products directly offered by the fintech bank will be limited to “funds holding”, comprised of: bank accounts (multi-currency); credit and debit cards (multi-currency); eWallet (multi-currency). All other services (investing, trading & brokerage; wealth management; loans, credit & mortgages; crowdfunding (equity and social); insurance; crypto-currencies; payments; remittances & FX; this list is not exhaustive) will be provided by third parties through the API, including old-school banks, financial institutions and fintech companies.

Imagine that you are a client of this “marketplace bank” and that you need a loan. You do not really care if the loan is provided to you by Lending Club or Bank of America, what you look for is a quick and frictionless process to get your loan, and the lowest interest rate possible. “It is a simple mix between an access fee to the “marketplace bank” and a revenue sharing model with the third parties providing additional services.”

Here we have a completely different approach regarding the relationship with incumbents. Fintech banks, thanks to their banking licence, will not rely any more on any bank to be and stay in business, and so will not be at the mercy of incumbents. What is even more powerful, through the marketplace, incumbents will become “clients” of fintech banks, so the system will be completely reversed.

The beauty of “marketplace banking” is that it competes directly with banks on core banking services without the need to build all the products. Most bankers are not already worried enough by fintech to react to its coming second wave. This creates a fantastic “window” for us fintech entrepreneurs, to build it, and once it’s done, it will be too late for them to react.

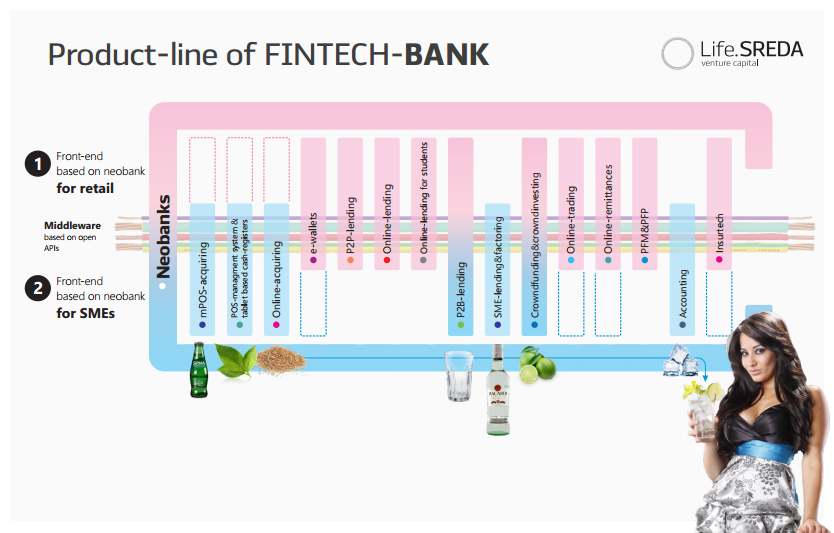

I believe, that the next step (and this step will be not about more money, but about real evolution of fintech-movement to ecosystem) in fintech will belongs to new generation of “fintech-banks” (maybe, they will be totally separated from traditional banks, maybe not, but it is harder in terms of mindset, corporate culture and processes, and old-school IT-infrastructure), which will have:

- Investment arm\fund to invest in several fintech-startups to build strong relationships with them;

- Bank-as-service platform as back-end – to host these standalone independent fintech-startups on their main market and to expend faster&cheaper to other markets;

- Neobank(s) as front-end(s) – to tailor all these services for final end-users in unique user experience.

The Full presentation: