Things That Go Bump In The Night: IEX, Bitcoin, And The Smart Money

From Seeking alpha

The two new transaction environments, IEX and Bitcoin, will turn the financial world on its head.

Corporations and governments are lining up their strategies.

Some promising big players: Barclays, Goldman Sachs, JP Morgan, IBM, and the UK.

The human animal prefers to live in an unchanged environment. Fear of change is an instinct in every species. For good reason. The salient factor about yesterday, in the world outside civilization where in earlier millennia human instinct was created, is that today’s creatures survived it. The instinctive moral is, make today as much like yesterday as possible, survive again. Repeat.

And this instinct, translated into the world of finance, is a fundamental tenant of investment — the greater the uncertainty of a project or investment, the greater must be its expected payoff.

Financial innovation, when it becomes an important factor in determining the future financial landscape, inevitably requires management of the normal human aversion to change. But will the innovators account for the threat they present, and defuse the fear they inspire? Or will they instead see the fear they inspire as reason to assume an adversarial posture?

As I watch the unfolding story of two developments in financial technology, the new transactions technology associated with IEX (Private) – a putative exchange that seeks, through technological change, to redress the balance between the interests of the buy side and the sell side of the market for investments; and Bitcoin – a crypto-currency that represents a new approach to the management of transfer of property rights; it seems to me that the advocates of both are not sufficiently focused on the angst they are inevitably producing. As a result, they are not managing their need to address the threat that they inevitably pose to the vast majority who are naturally averse to the dramatic change that they represent.

And how will the institutions, big and small, that inhabit the financial landscape manage these new factors in financial evolution? Conventional wisdom is that the large institutions such as the dealer banks: Bank of America (NYSE:BAC), Barclays (NYSE:BCS), Citigroup (NYSE:C), Goldman Sachs (NYSE:GS), and JP Morgan Chase (NYSE:JPM); the large exchange management firms (NYSE:ICE) and CME Group (NASDAQ:CME); and the large IT firms, IBM (NYSE:IBM), Microsoft (NASDAQ:MSFT) and Google(NASDAQ:GOOGL); will be too slow-of-foot and too invested in the old technologies to compete. They will, according to this school of thought, cede the field to the many start-ups, known as fintech firms, that are receiving the attention of investors looking for a quick kill.

My preliminary assessment is that three financial institutions, Barclays, Goldman Sachs, and JP Morgan, are doing the best job of fighting off their institutional inertia among the bigs. If they succeed, these banks will thrive in the next five years as the two technologies transform finance. IBM has recently entered the fray, with success that remains to be seen. Their press release shows an excellent command of the issues a firm like IBM will face, but the company is sitting on the fence and has not committed to a strategy yet.

And how will governments manage the financial system vulnerabilities implicit in these new technologies? In both technologies, the globe would better manage the angst the two technologies are about to create if Xanax, or possibly medicinal marijuana, were administered every week-day morning to federal regulatory executives for the next few years.

Because nothing short of hell or high water is going to stop either IEX or Bitcoin from transforming our financial system. And this will make regulation of the global financial system, as well as working for financial institutions, stressful. Yet for those of us who use the markets indirectly, investors, the result is going to be a more efficient, cheaper world.

In the early going, it appears that London will play its traditional role of entrepreneurial regulatory risk-taker. This role has served it well – notably in the rise of the Eurodollar and foreign currency markets – keeping it in the running with New York City in the completion for financial capital of the world. In the case of Bitcoin, London is actively supporting a sally into Bitcoin transactions, a joint venture between Barclays and Circle (a Boston-based fintech start-up). This is the first real retail commercial venture by a financial institution into this technology.

We have yet to learn, however, to what degree this is a “show pony,” or a “plow horse.” Is it a real commercial venture with a real exposure to the risks inherent in the technology? The answer will depend on whether the transactions involve a bank account at Barclays (show pony) or a transfer through the joint venture party in real-time without a bid-ask spread (plow horse).

Avoiding Moral Detours on the Tech Highway. A very important factor in the success of these new technologies will inevitably be the success of its managers in addressing the fear of the unknown that the technologies inspire. I am concerned that both the managers of the two technologies have fallen into a trap that things new and important should earnestly avoid. The trap is the tendency of forces behind change to allow moral content to seep into what is essentially a technological dialog. Both technologies are sliding into this trap. IEX is mistakenly portraying itself as “good.” Bitcoin is portraying itself as a “renegade.”

IEX is too good for its own good. Brad Katsuyama allowed himself to be lionized by Michael Lewis in Lewis’ book Flash Boys. Katsuyama should have run, not walked, from the notoriety created by Lewis’ book. He was associated by Lewis with the word “rigged” in describing the clone exchanges: NYSE, BATS, (:BATSBATS) and NASDAQ (NASDAQ:NASD). The word “rigged” became the focus of a famous CNBC interview – an interview that side-tracked the career of BATS President Michael O’Brien for his defense of high frequency trading (HFT). That event, and the enmity it created, has made the human element important going forward, and will cost IEX money and time.

The Lewis book and interview forced SEC Chair Mary Jo White to reject the word “rigged” publicly. And for good reason. The clone exchanges are not rigged. What they do is legal and in the public domain. This SEC denial will also have a cost to IEX. While portraying IEX in a moral light will sell books, it will retard the inevitable changes that the nascent would-be exchange will ultimately bring.

IEX is renowned for introducing the “speed bump,” a coil of fiber optic cable that slows inbound orders by 350 microseconds. The purpose of the speed bump is to prevent high frequency traders, the darlings of the clone exchanges, from front-running or otherwise using the advantage of their knowledge of orders in advance of the SEC-blessed broadcast of the Securities Information Processor (or SIP) the technology used to collect quote and trade data from different exchanges, collate and consolidate that data, and continuously disseminate real-time price quotes and trades for all stocks.

The SIP calculates the National Best Bid and Offer (NBBO) for all stocks, but because of the sheer volume of data it handles, has a finite latency period. (Latency is the difference between the speed of light and the speed of an order feed like SIP.) IEX’ speed bump allows SIP to catch up to the faster orders of High Frequency Traders (HFT) who outrace SIP by paying the clone exchanges for a head start. The speed bump, in theory, gives traders that have not paid an exchange for a speed advantage an equal opportunity to access the orders SIP displays.

That’s why, out of the dozens of exchanges in the world, only one – IEX – is not a clone of the others. At the moment the world sees IEX as a one-trick pony, the designer of the speed bump. But IEX is better understood as a group of very bright people who are going to develop many new technologies that improve the efficiency of trading. The question is, will IEX have the wisdom to minimize their opposition by not vilifying their opponents? If they don’t see the need for cooperation and even support from the powers that be, the job of changing the financial landscape will be slower and more difficult.

This makes the endorsement of the IEX by Goldman Sachs and JP Morgan Chase an important positive development and a sign that IEX’ management “gets it” now.

Bitcoin is too bad for its own good. Bitcoin’s future is also hampered by a moral posture – its renegade image. In the case of Bitcoin, users run from the fact that blockchain, the technology that drives the genius of Bitcoin, is an attractive technology for illegal transactions. They “bait and switch” blockchain’s bad rap to the crypto-currency, Bitcoin, going so far as to change the store of value that drives the economics of blockchain technology from Bitcoin to others to escape Bitcoin’s stigma. One example alternative to Bitcoin that is fashionable is Ethereum. But it is blockchain itself, the technology, that makes anonymity inexpensive. Furthermore, this anonymity is fundamental to blockchain’s value in transactions technology. One cannot hide from the very function of an innovation.

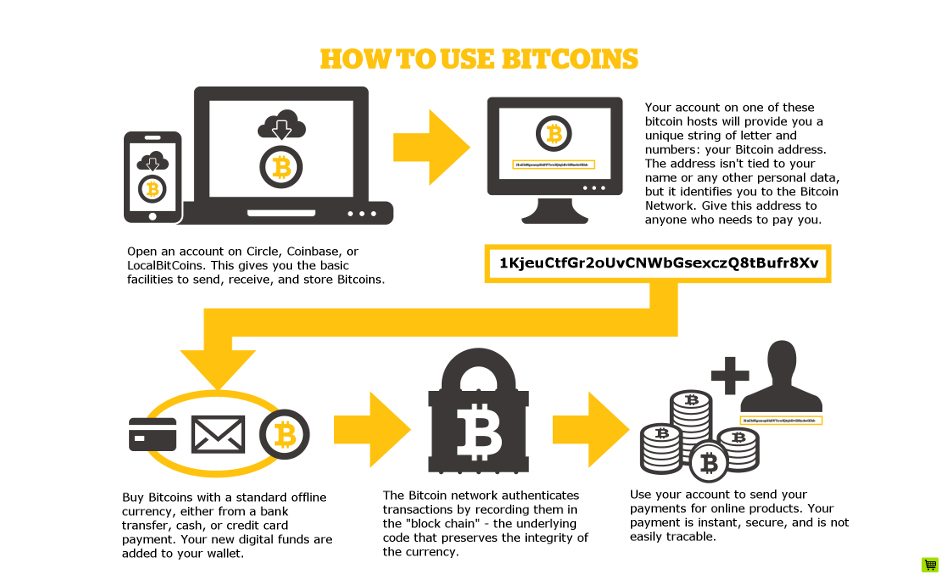

How Bitcoin works.

How Bitcoin works.

The genius of Bitcoin is the use of the computer power, the basic weapon of hackers, against these same hackers, reversing the role of computer power in offence and defense of security. One effect of this inspiration is that it is nearly impossible to identify the payer and receiver in any transaction, if anonymity is a trader’s objective. Anonymity is itself desirable – indeed often essential – in financial transactions. In securities markets, traders spend billions achieving anonymity, since knowledge of trader identity has a major negative impact on the price of a large trade. In Bitcoin, anonymity is all but costless. And blockchain tech made the cost of hacking blockchain prohibitive. This is the factor that makes the adoption of blockchain in finance inevitable. Any informed observer of the security of financial data has seen that security has become an IT arms race that will eventually fall under the weight of the prohibitive cost of firewalls and other forms of protection.

But the earliest important commercial uses of Bitcoin tended to be illegal transactions. Bitcoin became, very visibly, the store of value for payments for the drug and weapons transfer site, Silk Road, that was eventually closed by law enforcement.

And that is why, when an established market participant: governments, major financial institutions such as JP Morgan and Goldman Sachs, and major IT firms such as IBM enter the world of Bitcoin, the tendency is to call it blockchain. The pariah, Blockchain, goes unmentioned.

This is an immature reaction. It ignores a fundamental aspect of the blockchain technology. For computer power to provide the transactions security that blockchain promises, the larger the number of transactions the system processes per unit of time, the more secure it becomes. And adding new crypto-currencies only weakens the system’s security. And with no payoff. Because the currency is not the reason blockchain is useful to illegal users. It is the blockchain methodology itself. Illegal users will happily move to Etherium if that crypto-currency becomes more secure.

It was a positive sign in the UK that the first commercial application acknowledged the inevitability of Bitcoin. In a later article we will address Bitcoin paranoia and argue that the big firms should drop the effort to hide from it.