E-Wallets: Game of giants

By 2019, eMarketer estimates that the total value of transactions made by tapping a phone on an in-store terminal will reach $210 billion, up from $8.7 billion in 2015. For banks and retailers, that presents an opportunity to take on Apple Pay and Google’s Android Pay – and maybe save on transaction fees to boot.

Read our full research “Money of the Future”. Download PDF (20MB)The mobile-payment field is getting crowded despite slow consumer adoption. About 1 percent of U.S. households making at least $75,000 a year were expected to do their holiday shopping using a mobile wallet, according to Bankrate’s Money Pulse survey.

ApplePay

Apple Pay was launched last year, with lots of fanfare and support by the credit card industry. Partnering with the banks that issue credit cards overcame the resistance that early entrants in mobile payments had faced. It also solved critical technology and infrastructure problems and offered the credit card industry a new avenue for growth.

Apple Pay isn’t a household name yet, but it is growing steadily and is likely to become one. Most recently, Apple announced a deal with China’s UnionPay, the state-run sole issuer of bankcards, to allow it to operate nationwide in the People’s Republic.

China became the fifth country to support the contactless payment service. It’s currently live in the US, the UK, Canada, and Australia, but the company said it plans to bring it to Hong Kong, Spain, and Singapore soon. With UnionPay, Apple has a powerful partner — the association is responsible for clearing China’s bank card payments — but Apple Pay may face stiff competition from established mobile payment services, including Tencent’s WeChat, and Alibaba’s AliPay.

Apple Pay is, however, a Trojan horse. Once Apple has established its platform, it won’t need the banks and credit cards any more. It will be able take advantage of another new technology, the blockchain, to offer an alternative payment option. Blockchain is the core technology behind Bitcoin, and functions as a transparent ledger of transactions, concurrently hosted on numerous computers around the world — allowing the creation of digital currencies and virtual banks.

Apple Pay is, however, a Trojan horse. Once Apple has established its platform, it won’t need the banks and credit cards any more. It will be able take advantage of another new technology, the blockchain, to offer an alternative payment option. Blockchain is the core technology behind Bitcoin, and functions as a transparent ledger of transactions, concurrently hosted on numerous computers around the world — allowing the creation of digital currencies and virtual banks.

To be clear, Apple’s payment application has not taken off yet and works only on the latest model of its smartphones. According to data from payments-industry tracker Pymnts.com, as of October 2015, only 15 percent of all iPhone 6/6s users had tried Apple Pay. That is an increase from 9 percent in November 2014, but is hardly enough to set the world on fire. More significantly, only 5.1 percent of all Apple Pay eligible transactions (meaning, in which the store has an Apple Pay terminal and the shopper has an iPhone 6/6s) are running through the service. Because iPhone 6/6s models remain a small proportion of all iPhones in use, Apple Pay is capturing only a tiny volume of transactions.

But Apple has time on its side. And you can bet that Apple understands that the prize in play for global mobile payments is a larger market than that for phones, music, and computers combined. In classic Apple fashion, it is positioning itself to be a disruptive broker.

Apple’s advantages are that the iPhone has a cult-like following. And every time users buy a new phone or upgrade to a new version of iOS, Apple has a chance to convince them to try Apple Pay.

Let’s just take it as a given that Apple Pay achieves significant market penetration. What then? Another upstart payments company, Square, gives us a flavor of what is possible when technology companies control the payments infrastructure. Square is now offering loans to its merchants without the merchants even requesting it. What’s more, it is basing the loan offering on the transaction volume it sees the merchant processing. And Square is taking repayment directly out of the transaction stream. Apple could easily do something like this, either for consumers or for merchants. With data and coverage come insights and smarter ways to do business (for example, send you targeted ads based on your credit limit).

Evidence that Apple wants to combine payments and iMessage is piling up. And it looks like the tech giant doesn’t plan to stop there. A patent filing published in December 2015 indicates that Apple is not only looking at allowing people to send money over its text messaging service, but other services built into the iOS platform, including phone calls, email, and calendar invites. Companies like Apple file patents that go unused all the time, but the application shows that Apple is paying attention to a key trend in the technology industry: the convergence of messaging and payments.

The patent hints at how the functionality may work. The image shows two iPhone users chatting in the iMessage app, with a payment option popping up in the top-right corner when one party asks the other to pay them back for lunch. The images also show the ability to send payments to more than one recipient, and an option to set how much money is sent. Other major tech firms are looking to integrate payment features inside messaging apps. Facebook Messenger added the ability for users to pay their friends earlier this year, and recently added the ability to order a ride from Uber within the app. This kind of functionality is already common in Asia, where apps like WeChat—which has 650 million monthly users—let users buy food, order taxis, pay bills, check bank statements, and more.

A Sept. 2015 report from Javelin Strategy & Research, a financial services firm, found that peer-to-peer payments are especially popular with two key age groups in the US: 18-24 year olds, and 25-34 year olds. The goal will be to get these young people to use Apple Pay in stores, where Apple reportedly gets a slight cut of each transaction, and make iPhones even more integral in their daily lives.

An upcoming iPhone feature, which will let users send money to friends, is expected to be an unprofitable way to boost adoption of Apple Pay Silicon Valley is obsessed with a particular part of the finance business that involves sending cash to friends using an app. That’s led to a flurry of options that often aren’t profitable because they charge little to no transaction fees. PayPal and its subsidiary, Venmo, are among the most popular, though they face a growing list of competitors, including Google, Facebook, and Square.

The world’s most valuable technology company has been talking with banks about introducing its own feature to Apple Pay that will allow users to send money to friends. If Apple hopes to compete, it will also need to make its service free to use with debit cards. Apple isn’t likely to find a way to profit directly from the feature. Instead, the company will probably use it to increase adoption of Apple Pay in stores. The mobile tap-to-pay option hasn’t taken off as quickly as expected since it debuted about a year ago.

Owners of newer iPhone models used Apple Pay in 2.7 percent of Black Friday transactions at stores that support the feature, compared with 4.9 percent on the same day last year, according to data from tracking firm InfoScout.

Facebook introduced peer-to-peer payments through its Messenger service in March. Once a user adds a debit card to a Facebook account, the person can send money through the chat window. Google said it has allowed people to send money to each other via its Gmail service for a few years, but created an app called Google Wallet for people seeking a mobile option.

It allows users to send payments to each other via debit card through an emailed link. Square also allows peer-to-peer payments using debit cards to users who have created a “$cashtag” account with the service.

After a sluggish start in the U.S. since its debut more than a year ago, Apple Pay is ramping up in markets where people are more comfortable with so- called contactless payments. The service, which lets consumers pay in an app or by tapping their iPhone on store terminals, will be introduced next year not only in China, but also in Hong Kong, Singapore and Spain. Apple is counting on its brand recognition as it enters markets that are further along than the U.S. in all things mobile payments, particularly in advanced technologies needed to accept them in retail outlets. Still, it won’t be easy. The iPhone maker will compete with local banks and Internet companies that already offer the service — not to mention Samsung Electronics Co., the world’s leader in smartphones.

Adoption has been faster in the U.K., where Apple Pay was introduced in the summer. That’s partly because of agreements with merchants such as sandwich chain Pret A Manger and Twickenham Stadium that let customers use Apple Pay to ring up unlimited amounts in transactions. Also, Apple’s operating system, iOS, commands a strong market share, with 39.5 percent of smartphone sales in Great Britain in the three months ended in October, according to Kantar Worldpanel ComTech.

Apple Pay will be available to eligible American Express users in Hong Kong and Singapore next year, Apple said in October. Companies like Hong Kong Telecommunications and HSBC already let consumers in Hong Kong pay with mobile phones in stores. In Singapore, a consortium of mobile operators, banks and service providers has been working on enabling contactless payments in shops, restaurants and taxis for at least three years. But Apple is increasing its presence in the country, and recently announced it will open its first retail store in Singapore.

Google Wallet and Android Pay

In March 2015 at Mobile World Congress Google announced the launch of its wallet called Android Pay. Just imagine Apple Pay but customizable, open, free and completely white-label, that’s how Android Pay looks like. Confrontation of open and closed architecture principles, iOS vs Android – now and in the world of payment solutions.

In September 2015 Google rolled out a big update to its Google Wallet app for iOS, which brings a few nifty new features and a welcome redesign. Users can now send peer-to-peer payments, or cash out directly to a debit card — though Google is removing support for loyalty cards, gift cards, and offers with this update. “Send money to anyone in the U.S. with an email address,” Google said of the new service. “It’s fast, easy, and free to send directly from your debit card, bank account, or Wallet Balance.” “When you receive money, you can quickly cash out to your bank account using your debit card, or spend it instantly with the Google Wallet Card,” the company added.

In September 2015 Google rolled out a big update to its Google Wallet app for iOS, which brings a few nifty new features and a welcome redesign. Users can now send peer-to-peer payments, or cash out directly to a debit card — though Google is removing support for loyalty cards, gift cards, and offers with this update. “Send money to anyone in the U.S. with an email address,” Google said of the new service. “It’s fast, easy, and free to send directly from your debit card, bank account, or Wallet Balance.” “When you receive money, you can quickly cash out to your bank account using your debit card, or spend it instantly with the Google Wallet Card,” the company added.

Other features that Google wants users to take advantage of include splitting expenses (i.e. at a meal or on a trip), managing the Wallet Card (accepted wherever debit MasterCard is and at ATMs), placing limits on spending, and setting up recurring transfers from your bank account.

This is the same functionality that has been in the old Google Wallet app and Gmail’s “Attach money” feature, now in a standalone app. Other than that, there’s a way to look at your past transfers and even a section for managing your “Google Wallet Card,” which Google initially released as a stop-gap for when NFC didn’t work.

There is no NFC or loyalty card functionality here anymore. Those features will all move to Android Pay once the app launches. And the new Google Wallet app does not actually replace the old Google Wallet app—the upcoming Wallet app is a brand-new app under the package name “com.google.android.apps.gmoney” while the old Google Wallet—”com.google.android.apps.walletnfcrel”—will eventually be upgraded into Android Pay. Today, you can have both apps installed on your device and have “Wallet” and “Wallet” sitting right next to each other in the app drawer.

This is all a little confusing, isn’t it? There are two money apps now. This new Google Wallet app means Android Pay won’t be the one-stop-shop for transferring money on Android the way Google Wallet was. Android Pay will handle tap-and-pay and online transactions, but apparently not sending money to friends. So if you want to send money to a store, that’s Android Pay. Sending money to a website? That’s Android Pay, too. Sending money to a friend? That’s this other app.

Google bought Softcard’s point-of-sale tech and made some international advances for its money transfer service. Also customers that use Android apps from Dunkin’ Donuts and Seamless, and merchants that build online stores through Shopify, will able to access Google Wallet to make and accept quick payments.

PayPal

PayPal started trading on the Nasdaq at $41.46 per share. As an independently traded company, PayPal was already valued at roughly $50B. Compare that with eBay’s market cap of about $33.64B. It means, PayPal is now worth more than Netflix, eBay and Twitter.

As PayPal rebuilt itself for a post-eBay future, it took a fresh look at the vital statistics it was monitoring for signs of trouble. “Over four months, we did a lot of analysis to figure out which are the most high-value signals,” Shivananda says. “Even though we run the science across all 350,000 signals a second, the high-value signals, we put up on the walls. Everything else goes on an alert mechanism.”

As PayPal rebuilt itself for a post-eBay future, it took a fresh look at the vital statistics it was monitoring for signs of trouble. “Over four months, we did a lot of analysis to figure out which are the most high-value signals,” Shivananda says. “Even though we run the science across all 350,000 signals a second, the high-value signals, we put up on the walls. Everything else goes on an alert mechanism.”

The company is also beginning to automate some aspects of addressing common problems, in instances where it was confident that applying the same fix in the same way to the same type of flaw will work every time. Already, PayPal has created bots that are capable of patching servers on the network which have out-of-date software.

“The future of the ecosystem is not visual indications,” says Shivananda. “It’s basically the science that runs says ‘This application is throwing more errors, please roll back.’ And after that, it’ll go ‘I know the signal. I know what to do. I’ll just do it.” No matter what sort of technology PayPal comes up with, the fact that it has 350,000 data points a second to consider means that it’s not going to run out of opportunities to make the service more robust any time soon. “That data has all the signals,” Shivananda says. “The question is, are we listening to it?”

PayPal has acquired Paydiant, payment technology provider for eWallets – both for individual businesses (Subway, Harris Teeter supermarkets), and for universal wallets (CurrentC, which is supposed to compete with Apple Pay). Terms of the deal were not being disclosed, but according to Re/code, it was a $280M deal. As far as 80% of PayPal’s transactions happen to be online acquiring (with the rest accounting for mobile acquiring), their acquisition of the eWallet technology and team is a big step towards the leadership in a new sphere.

PayPal’s instant checkout service called OneTouch was being extended to support all merchants using the e-commerce platform Bigcommerce, as well as on mobile devices – even in cases where the consumer doesn’t have the PayPal native application installed. The service, which allows customers to check out from an online merchant without having to enter their username and password, launched publicly last fall on mobile devices then expanded to the web in April 2015. UK and Canada became first foreign markets[.

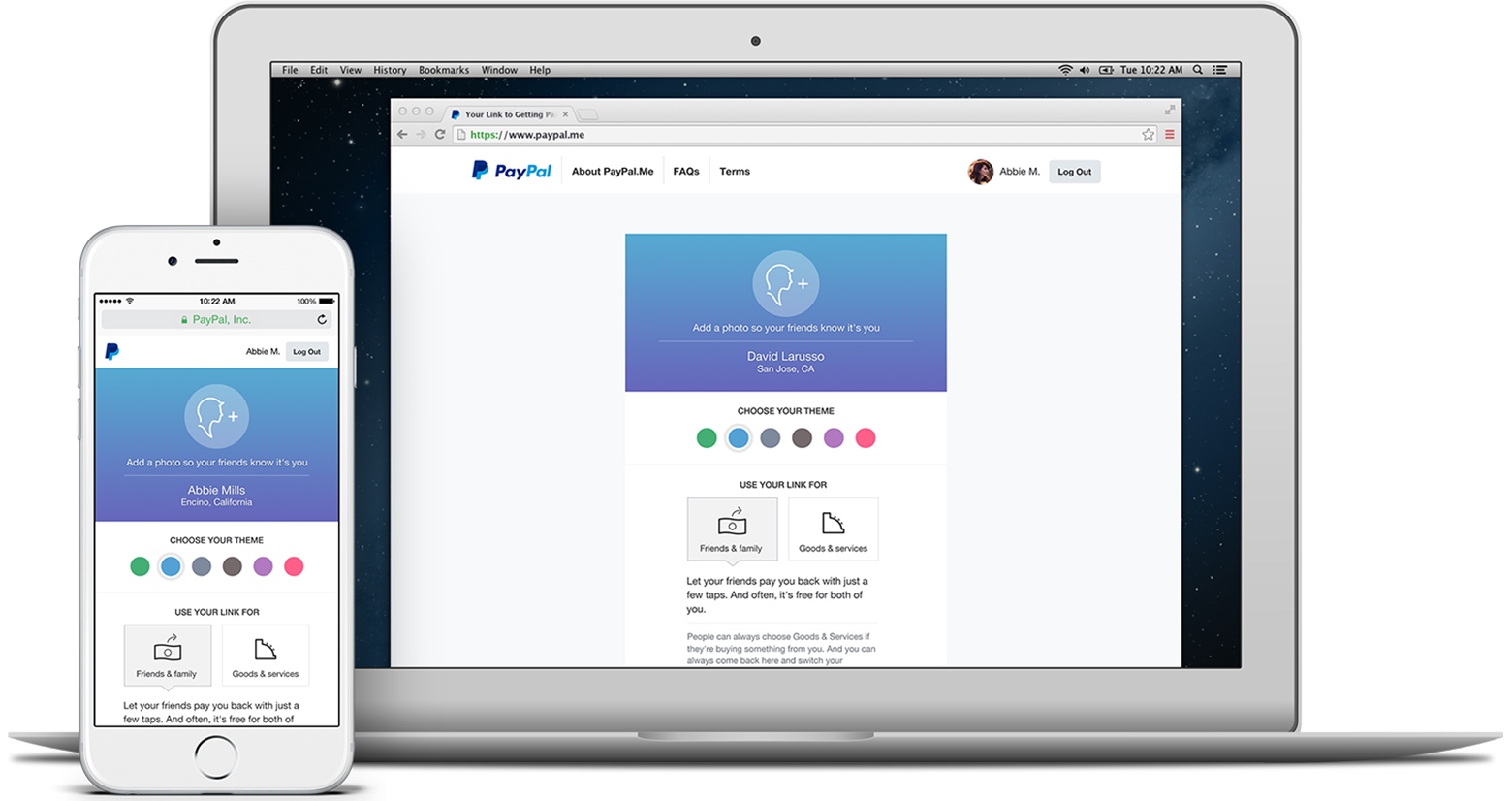

Around the world, we’ve reportedly loaned each other a staggering $51 billion, according to a study conducted by PayPal. PayPal launched a new feature aimed at making it easier to remind each other about those unpaid debts without things getting weird. PayPal.Me is a new, more effortless way to request money via PayPal using a short, customizable URL. Need your coworkers to pay you back for the cab you all shared from the office that happy hour the other night? The link will then redirect to a simple mobile interface that lets them do exactly what the URL suggests.

Target, CurrentC, Chase and Wal-Mart seek to disrupt mobile payments business in 2016 too

Companies like JPMorgan Chase & Co. and Wal-Mart Stores Inc. are rolling out their own products just as mobile-payment apps are catching on. At stake is a fight over money and consumer data. Retailers loathe paying fees to accept credit cards in their stores and have long sought better data on what their customers buy, and when. Banks similarly dislike paying fees for Apple Pay transactions. Thus, financial institutions and retailers have incentive to push out their own mobile-payment services.

JPMorgan Chase plans to introduce its own mobile wallet in mid-2016. Mobile-banking apps are already used by more than half of U.S. smartphone owners with bank accounts, according to the latest Federal Reserve survey. Chase plans to pre-load cards for 94 million customer accounts “so the customer doesn’t have to do anything but accept the terms and conditions,” Gordon Smith, CEO of consumer and community banking at JPMorgan Chase, said in a keynote at the Money20/20 conference in October. Chase still wants its cards in all mobile wallets, and has decided to support Apple Pay, Samsung Pay and other competing services.

Retailers like Walmart and Target likely prefer proprietary in-house systems for two reasons: They can save on processing fees for credit card transactions, which stores would otherwise have to absorb, and they gain deeper insight into consumer behavior. But Target may face challenges in rolling out a mobile wallet, even if it’s just a matter of optics: A 2013 hack led to criminals obtaining the credit card numbers and personal information of tens of millions of Target customers. And the company found itself back in the news due to a security flaw in its mobile app. Target’s decision to launch its own payment app is also one more piece of bad news for CurrentC, an erstwhile Apple Pay and Android Pay rival backed by Walmart and Target, among others. CurrentC’s release date has been rolled back repeatedly as backers have opted to create their own proprietary products instead.

Walmart will begin accepting payments through its mobile app in all U.S. stores in the first half of 2016. About 22 million Walmart shoppers already use the app, which compares prices and offers discounts on items and will now let customers store their credit- and debit-card information.

Walmart will begin accepting payments through its mobile app in all U.S. stores in the first half of 2016. About 22 million Walmart shoppers already use the app, which compares prices and offers discounts on items and will now let customers store their credit- and debit-card information.

Walmart is launching its own proprietary mobile wallet app, Walmart Pay. The company’s iOS and Android apps will allow users to pay at Walmart checkouts with any smartphone, through which they can charge purchases to their personal credit or debit cards, pre-paid cards, a Walmart gift card, or a store credit card. It essentially combines a checkout payment system with app functionality, which allows customers to also locate items in-store or pick up items they have reserved.

Walmart launching its own app is essentially a vote of no confidence in CurrentC, which has big backers (Target, Kohl’s, Rite Aid), but has been plagued by delays, a data breach, and withering beta reviews from customers.

Merchant Customer Exchange – a consortium founded in August 2012 by merchants including Wal-Mart and Target Corp. – is testing its CurrentC app with about 200 merchants in Columbus, Ohio. The service is not yet available nationwide. “There will be more than one successful player in the mobile-payments space, and we fully expect to be one of them,” said Brian Mooney, chief executive officer of MCX.

CurrentC, the payments app being created by a consortium of big retailers known as MCX, will begin a public pilot of its app in Columbus, Ohio, and will not rush a wider rollout if the product is not ready. CurrentC — backed by several dozen big merchants including Walmart, Target, Kohl’s, Dunkin’ Donuts and Exxon — is designed to work on all types of smartphones and let shoppers pay with the app instead of a physical payment card or cash. But while Apple Pay and soon-to-launch services Android Pay and Samsung Pay let users pay using account information from traditional credit cards like Visa, MasterCard and Amex, CurrentC does not. Instead, CurrentC’s beta users can only pay using one of three options: Gift cards, a store’s private-label payment card or direct hookups with their checking accounts.

Mainstream credit cards carry higher transaction fees than these options, which is a big reason why they aren’t currently part of the offering. For starters, there are not a ton of high-profile success stories in the tech world that are a result of joint ventures. One advantage they all have over CurrentC: They will be preloaded on millions of new phones over the next few years, while CurrentC will have to get people to download its app.

Mainstream credit cards carry higher transaction fees than these options, which is a big reason why they aren’t currently part of the offering. For starters, there are not a ton of high-profile success stories in the tech world that are a result of joint ventures. One advantage they all have over CurrentC: They will be preloaded on millions of new phones over the next few years, while CurrentC will have to get people to download its app.

Best Buy was the first big-name U.S. retailer to break ranks with a Walmart-led Apple Pay competitor, announced that it will accept Apple’s digital payment system in its U.S. stores. Best Buy has also started accepting Apple Pay as a payment method in its apps. The partnership is a big one for Apple, because it’s the first with a member of MCX, a consortium of retailers and food chains that is building a payment app called CurrentC that is expected to be competitive with Apple Pay.

Microsoft is preparing to follow Apple and Google into mobile payments, lining up the regulatory approvals needed for the launch of a host card emulation-based service. In March 2015 the firm showed off the tap and pay mobile payments system for handsets running its new Windows 10 operating system at a conference in China. As well as support for Secure Element-based payments, it also taps HCE.

Amazon’s General Manager of Payments, Matt Swann, has left the company after the failure of Amazon Wallet. Amazon has deleted its Amazon Wallet application from Google Play store and Amazon app store. Reasons: poorly elaborated app and partly related to this low popularity of the wallet.

AliPay

In July 2015 Ant Financial confirmed that it closed a Series A funding round which includes investment from China’s largest pension fund, the National Social Security Fund (NSSF). While it isn’t a traditional Series A — because most startup aren’t formed as an offshoot from a multi-billion e-commerce juggernaut — the deal is eye-watering. Ant Financial said the undisclosed round included capital from “major Chinese insurance corporations” and other investors.

TechCrunch understands from sources close to Ant Financial that it values the company at $45-$50 billion. The investment from NSSF — which we hear included a substantial discount — brings on an interesting strategic investor. China’s government recently relaxed regulations on how the fund can invest, and this deal with Ant Financial is the first such investment that NSSF has undertaken since that loosening. It’s also a huge validation for the business, and could help Ant Financial with legal and regulatory hurdles in the future.

TechCrunch understands from sources close to Ant Financial that it values the company at $45-$50 billion. The investment from NSSF — which we hear included a substantial discount — brings on an interesting strategic investor. China’s government recently relaxed regulations on how the fund can invest, and this deal with Ant Financial is the first such investment that NSSF has undertaken since that loosening. It’s also a huge validation for the business, and could help Ant Financial with legal and regulatory hurdles in the future.

Alibaba had the largest IPO in history because the hugely popular retailer benefits almost anytime someone in China spends money online. So now it’s trying to pump even more money into China’s online economy, by introducing the country’s consumers to the tools of modern finance. At least that’s one way to look at Ant Financial. Run by Alibaba cofounder Lucy Peng, the division—which was spun off into its own company in 2011—began as an outgrowth of Alipay, the company’s version of PayPal.

Since then it has expanded into a full-scale financial services firm. It now includes a money-market fund, a peer-to-peer lending service, and a microloan program for online entrepreneurs. In February it announced a fund to seed Hong Kong–based startups that want to do business on Alibaba’s platform. And the company is developing Sesame, which will assign credit scores based on Alibaba customer data, thus potentially making it easier for millions of consumers to get loans—and, from there, to start small businesses, many of which will likely set up shop on Alibaba’s platform.

Alibaba’s relationship with the Chinese government has always been fraught, but the two entities share an interest in increasing the purchasing power of the Chinese populace. Indeed, China granted Alibaba one of five licenses to establish a private bank, part of an effort to establish critical financial infrastructure in the as-yet underserved country. (Alibaba rival Tencent received one as well.) Erik Gordon, a professor at University of Michigan’s Ross School of Business who has studied Alibaba, says that if the company can become the default bank for China’s working and middle class, its financial services business could dwarf its current ecommerce enterprise. “I wouldn’t be surprised if in 10 years Ant was the largest financial institution in the world,” Gordon says. “Nothing would surprise me less.”

McDonald’s teamed up with Ant Financial to start accepting mobile payments in more than 2,100 of its restaurants in China, using Alipay. McDonald’s Shanghai chains will be the first to integrate the new mobile payment option, with the countrywide rollout to be completed by March 2016. The fast-food chain is also looking to partner with Alipay on “data technologies” to learn more about its customers, businesses, and ecosystems — essentially to compile big data on Chinese consumers in order to really take its business in the country to the next level.

In June 2015 MYbank, a startup backed by Ant Financial Services Group, launched a digital-only bank to provide “inclusive and innovative financial solutions” at lower cost to under-banked urban and rural consumers and small and medium businesses. The startup does not have a physical presence and so it can serve customers 24X7. It begin setting up accounts and accepting deposits, its initial strategy is to concentrate on issuing small loans of less than RMB 5 million (US$805,500) for SMBs, entrepreneurs and consumers.

Paytm

In September 2015 Alibaba has sharpened its focus on India after it made a second investment in Paytm, a mobile payments and e-commerce business. The investment was made by Alibaba and Ant Financial, the Chinese firm’s financial services affiliate, which made an undisclosed investment in Paytm in February 2015 via a deal that reportedly valued the Indian company at more than $1 billion.

This new deal is also undisclosed; however India’s Economic Times reports that Alibaba is spending $680 million to buy 20 percent of Paytm. That lowers Ant Financial’s stake from 25 percent to 20 percent, the report added. So, in essence, Alibaba is now making a firmer commitment having tested the water via the Ant Financial deal.

This new deal is also undisclosed; however India’s Economic Times reports that Alibaba is spending $680 million to buy 20 percent of Paytm. That lowers Ant Financial’s stake from 25 percent to 20 percent, the report added. So, in essence, Alibaba is now making a firmer commitment having tested the water via the Ant Financial deal.

Paytm, which grew and was spun out of mobile content company One97, bears much similarity to Alibaba’s own constellation of businesses, albeit that it is far less developed. It offers a range of financial-focused services in India, including a mobile wallet app (used by Uber, among others), online recharge (for topping up phone credit and more), and a shopping service.

The company said it has been working on “synergies” with Alibaba since taking funding in February, and its e-commerce marketplace is a particular area of focus given that Alibaba practically pioneered the genre in China with its Taobao site.

Paytm claims more than 100 million users of its wallet service, which helps Indians buy items online without the need for a credit/debit card or banking. The startup said the Paytm Wallet clocks more than 75 million transactions each month. Vijay Shekhar Sharma, founder and CEO of Paytm said the company is looking “to bring half a billion Indians to the mainstream economy and help millions of small businesses leverage this large m-commerce opportunity.”

“India is an important emerging market with strong e-commerce potential, and we look forward to partnering with Paytm to deliver innovative products and services to consumers… This investment will further expand Alibaba Group’s global footprint to India’s thriving mobile commerce market,” Alibaba CEO Daniel Zhang said in a statement.

Samsung Pay

In February 2015 Samsung acquired m-wallet LoopPay, mentioned in our previous annual research. It’s going to compete with Apple Pay, and the LoopPay’s payment solution compatible with merchants’ equipment installed to accept card payments (which makes 90% coverage in comparison with less than 10% for NFC-based wallets like ApplePay), will be helpful for the world’s largest smartphone manufacturer. According to Samsung representatives, it’s the company’s first step to building a full-fledged financial infrastructure on the basis of the Samsung Pay

Samsung begun rolling out its answer to Apple Pay in Korea in July 2015. The service was called Samsung Pay and it is powered by LoopPay, the Boston-based company. It’s due to launch in Korea and the U.S. first before expanding worldwide, but Samsung has nudged it into action with a pre-launch pilot program among Galaxy S6 and S6 Edge owners in its home country. They seem nearly identical, but Samsung Pay has a couple if differences compared to Apple Pay.

Samsung begun rolling out its answer to Apple Pay in Korea in July 2015. The service was called Samsung Pay and it is powered by LoopPay, the Boston-based company. It’s due to launch in Korea and the U.S. first before expanding worldwide, but Samsung has nudged it into action with a pre-launch pilot program among Galaxy S6 and S6 Edge owners in its home country. They seem nearly identical, but Samsung Pay has a couple if differences compared to Apple Pay.

Life.SREDA VC is a global fintech-focused Venture Capital fund with HQ in Singapore