15 Useful Personal Finance Management Services

Here are 15 budgeting and personal finance apps that shape the way we spend.

Read our full research “Money of the Future”. Download PDF (20MB)

People are more than just their credit scores. This opportunity moves us beyond the credit score to a more nuanced, shared measurement of peoples’ financial health. In this view, traditional credit scores are but one indicator of overall well-being. But there are other measurements that also matter to both consumers and providers. How are people doing managing their daily finances? Do people use systems and products that make them resilient to unexpected financial challenges? Are people able to achieve major financial objectives — such as buying a house or retiring comfortably?

Taking a “financial health” lens is what consumers already do naturally. They’re already thinking about their daily financial management, how resilient they are over time and how they’re preparing for long-term opportunities. Providers could adopt both this language and this lens to meet consumers where they are, help them quantify their financial health and give them the tools to improve their lives over time.

The focus is not, then, on a number — the focus is on peoples’ livelihoods. This benefits financial services providers.

Knowing more about customers’ systems and financial health trajectory can help providers make better decisions about credit worthiness. A change in financial health can trigger marketing moments for providers to reach out the customers — and help avoid emergencies by offering other product options. Plus, using a broader measurement can open a door for millions of people without scores, with low scores or with mis-understandings about their scores. When consumers and providers alike take a financial health perspective, the challenges associated with credit score exclusion, awareness and financial impact diminish.

Whether you could use some help managing your email inbox, keeping your spending under control or maybe just earning a higher interest rate on your savings, there are several tools that can make money management easier. As long as entrepreneurs hunt for ways to disrupt the traditional financial industry by offering more customized products that make it easier to save, consumers stand to benefit. “The financial space has been dominated by legacy institutions for a long time,” Prism’s Griffin says. “Consumers are going to be pretty delighted over the next two to five years with products coming out that make finance not so scary, not so intimidating and are very aligned with their needs.”

LearnVest (US)

For providing comprehensive personal financial planning at an affordable price. Do you have enough saved for a rainy day? Should you pay down your credit cards? These are the kinds of questions that everyone encounters at some point—but individuals with big questions and small bank accounts often have a hard time finding anyone to give them good advice.

LearnVest fills this niche, estimated at 40 million U.S. households, with a blend of technology and human touch. For $299, one of LearnVest’s 50-plus planners will speak with a client on the phone, draw up a financial plan, and then walk the client through it. For $19 per month, users get continued support via email, plus access to premium educational tips.

LearnVest also has a website and an app to help users track their progress; the company grew out of the initial website, which was launched in 2009 as an education resource by Financially Fearless author Alexa von Tobel, and now draws 1.5 million visits per month. LearnVest just forged a deal with Fidelity Institutional to make its services available to individuals with workplace retirement plans.

Alexa von Tobel (the guest of “Money of the future” conference) , whose startup LearnVest was featured on our list of the world’s Most Innovative Companies, has sold her company to Northwestern Mutual for what sources tell Fortune is more than $250 million. The startup raised $75 million in venture capital, with Northwestern Mutual investing in its most recent round.

Von Tobel, a business-school dropout, launched the New York-based company in 2009, and originally targeted it toward women to help them better understand and manage their finances. The site eventually expanded beyond those early ambitions and eventually grew its user base to around 1.5 million visits per month, offering a personalized and education-focused alternative to competitors in the space such as Mint.

LearnVest offers some free applications, but also charges for premium services. For example, users can pay to consult with one of the company’s on-staff financial planners to get a fuller picture of their financial outlook and how to more smartly budget their money.

Northwestern Mutual gets a fresh sheen of branding, which is likely to help the 158-year-old financial firm appeal to younger generations. While this partnership may seem unlikely at first, it actually makes a lot of sense for both parties.

Northwestern Mutual gets a fresh sheen of branding, which is likely to help the 158-year-old financial firm appeal to younger generations. While this partnership may seem unlikely at first, it actually makes a lot of sense for both parties.

The acquisitions market is thriving as well. Intuit acquired bill pay app Check for $360 million last May and budgeting platform Mint.com for $170 million back in 2009. More recently, Capital One bought budgeting app Level for an undisclosed amount.

The success of LearnVest and other fintech startups provides a number of valuable lessons for young companies in any sector. To start, LearnVest picked a pain point that really needed a solution. Americans are drowning in debt. U.S. consumers owe $11.52 trillion to lenders and creditors. An astonishing one in three American adults with a credit history are delinquent on their debt and the average family has $7,630 in revolving debt.

LearnVest’s growth also stemmed from the fact that its target audience was millennials. By focusing on millennials, LearnVest tapped into a valuable and underserved group of consumers.

LearnVest also leveraged data science in order to better serve its customers, building it into the company from the get-go. Data science is essential to building a successful company today. Advancements in big data, advanced analytics, and machine learning have enabled companies to gain greater insights about their customers than ever before, not to mention about providing personalized recommendations and even make predictions.

In addition to solving a big pain point, catering to millennials, and leveraging data science, LearnVest also mastered the art of communicating its overarching vision. Alexa von Tobel is more than the CEO of LearnVest — she has emerged as a well-known thought leader in the financial tech space. She authored a New York Times bestselling book titled Financially Fearless, actively contributes to prominent news outlets, and regularly speaks at conferences.

She has also been named to scores of “top” entrepreneur watch lists and is widely known as an expert on and advocate for financial health. Her vision and persona have been a major driver in the success that LearnVest has achieved.

The company plans to continue operating independently and Northwestern Mutual will use LearnVest’s technology with its own clients and financial representatives. It may seem like a surprising partnership, but as Northwestern Mutual CEO John Schlifske told Forbes, “this was very clearly a match made in heaven.”

Aviva Druyan, head of talent acquisition, shares what she’s looking for in new hires.

“We look for people who want to learn and can scale with LearnVest’s incredible growth. Outside of the obvious—experience, ability, a good fit with the team and company culture—we value candidates that deeply care about our mission of empowering people nationwide to make good decisions with their money. We look positively on candidates who will challenge the status quo and who are able to both think strategically and execute.”

“Between our New York headquarters and planning hub in Scottsdale, Arizona, we have over 150 employees, and we’re adding to that number frequently. We are in constant hiring mode. We have many open positions, and we’re moving into new offices in New York City in 2016 to support this growth.”

Level Money (US)

In early 2015, Capital One announced it had purchased Level Money. The startup will now continue on as a part of Capital One, but will remain a standalone application. The Level Money team of 11 will also stay together, including co-founder and CEO Jake Fuentes. Terms of the deal were not disclosed. The startup had raised $5 million in Series A funding led by Kleiner Perkins Caufield & Byers.

In early 2015, Capital One announced it had purchased Level Money. The startup will now continue on as a part of Capital One, but will remain a standalone application. The Level Money team of 11 will also stay together, including co-founder and CEO Jake Fuentes. Terms of the deal were not disclosed. The startup had raised $5 million in Series A funding led by Kleiner Perkins Caufield & Byers.

When Level Money co-founder Jake Fuentes graduated from college, he had $33,000 in student loan debt and $11,000 in credit card debt. He wasn’t happy with the financial tools he had at his disposal to help manage those debts.

“We’re surrounded by money management tools that for lots of people are way too complicated. We take all that information and simplify it down to its essence,” he says. Managing your money should feel as simple as opening up your wallet and seeing how much cash you have left, he adds.

Level Money attempts to do that by connecting to your accounts. The app then reviews your expenses, recommends a savings rate (for most people, it’s around 7 percent of income) and advises you on how much you have left to spend. If you walk into a grocery store, the app might inform you that you have $23 left to spend today and $67 for the week.

“What we’re trying to deliver is confidence,” Fuentes says. “We think we can deliver a sense of peace and Zen about decisions and take away the sense of stress and anxiety that exists around money for a lot of people.” Most customers are millennials, he says, and the company, which launched in October 2013, was recently acquired by Capital One. The app has been used by about 750,000 people, and has helped its customers manage over $12 billion in transactions.

“Level is dedicated to rewriting the financial rulebook to create a secure future for the next generation.” That’s budgeting app Level Money’s stated mission, which can be found on their website’s “About Us” page. But even as lofty as that objective sounds, Jake Fuentes says the company’s sights are set even higher. “Basic everyday money management,” he suggests, could be “the first step toward changing—or creating—the next generation’s banking structure.”

Jake wants to relegate money to a place where it’s “not the center of our lives.” According to Fuentes,

“There’s a gulf between the way that financial institutions communicate”—through accounts, transactions and interest rates—“and the way that humans understand their money.”

Level wants to bring the old-school wallet back, packaged in the form of a highly sophisticated but elegantly simple app. Its central feature, the “Spendable” page, estimates how much you have left to spend today, this week and this month. The Spendable number is generated initially by populating three inputs: our monthly Income, recurring Bills and the desired AutoSave amount we choose to set aside. The balance is our Spendable cash flow.

NerdWallet (US)

NerdWallet had raised $64 million in May 2015 in its first round of funding, far more cash than it needs to run the personal finance startup, in part to underscore its growth and show it has the potential to one day be valued at over $1 billion. NerdWallet also has a $36 million revolving loan from Silicon Valley Bank. Venture firm IVP led NerdWallet’s funding round, with participation from RRE Ventures, iGlobe Partners and others. NerdWallet was founded in 2009.

NerdWallet had raised $64 million in May 2015 in its first round of funding, far more cash than it needs to run the personal finance startup, in part to underscore its growth and show it has the potential to one day be valued at over $1 billion. NerdWallet also has a $36 million revolving loan from Silicon Valley Bank. Venture firm IVP led NerdWallet’s funding round, with participation from RRE Ventures, iGlobe Partners and others. NerdWallet was founded in 2009.

The funding round values NerdWallet in the mid-hundred millions. Since the beginning of 2014, just eight U.S. startups have raised Series A funding rounds of $50 million or more, according to CB Insights, a consultancy. The cash, an outsized sum for initial funding, will serve as a signaling device as much as it will help NerdWallet expand, said founder and Chief Executive Officer Tim Chen.

“I really think that winning in this market is about attracting the best talent out there,” said Chen about his personal-finance advice company. “The more talent, the better.”

While the San Francisco-based company has already attracted top engineers and product managers from companies such as LinkedIn Corp and Twitter Inc, having such a large first check from a top-tier venture capital firm, IVP, will help it recruit more in Silicon Valley’s tough job market, he said.

A recruiter says the strategy makes sense. “It’s like a seal of approval,” said Karen Myers, co-founder of the Talent Farm. When helping recruit for Lytro, the industrial camera company, the ability to tout the company’s $50 million initial funding round helped considerably. “It was a big deal,” Myers said.

NerdWallet, whose competitors include companies such as Bankrate Inc and Credit Karma, makes money from fees earned by matching consumers with appropriate financial products, such as credit cards. It is profitable, Chen said. The company helps consumers understand how to pick the best life insurance, say, or financial decisions they need to make around a major life event such as buying a house or having a baby.

Last year, 30 million people used NerdWallet to get financial advice on a range of subjects. The company offers comparison shopping tools on financial products including: healthcare; mortgages; life insurance; banking; credit cards; financial services and wealth management; small business tools, and college loans.

“To be honest, I want to cover every substantial financial decision that anyone can make in their life,” said Tim Chen. “We’re talking about a shitload of big decisions there.”

Chen’s company is squarely focused on the content business for now, but NerdWallet may have eventual aspirations to provide financial tools as well as financial advice for a new generation of financial services consumers. Already other companies like Credit Karma and Feex, have seized on NerdWallet’s mission to provide unbiased information to consumers about the financial tools that they use. But unlike those companies, Chen’s vision is all-encompassing.

The company would not comment on its revenue except to say that it would look to grow its staff from 200 to 300 employees by the end of the year and that the hiring push could be done without touching the new $64 million in cash sitting in the bank or the $36 million revolving loan the company received from Silicon Valley Bank as part of the latest financing.

According to the company, it has partnerships with eight undisclosed banking and credit card companies and has managed to scoop up high level executives from companies like Box, J.P. Morgan, LinkedIn, Visa, and Zynga. As a result of the investment Jules Maltz from IVP and Tom Loverro from RRE Ventures will take a seat on the board. Soo Boon Koh, iGlobe’s managing partner and founder will have a seat on the board of advisors alongside James Robinson III, former American Express CEO, Vikram Pandit, the former CEO of Citigroup, and David Henke, the former SVP of engineering and operations at LinkedIn and Yahoo.

Qapital (ex-Sweden, now – US)

Millennials aren’t saving money. When you’re living paycheck to paycheck, Excel spreadsheets are not always the first thing on your mind. Services like Mint give you a broad look at your finances, but there’s something missing in the app-focused millennial toolbox for saving toward goals.

Millennials aren’t saving money. When you’re living paycheck to paycheck, Excel spreadsheets are not always the first thing on your mind. Services like Mint give you a broad look at your finances, but there’s something missing in the app-focused millennial toolbox for saving toward goals.

Swedish startup Qapital launched its saving service in March 2015 to help you regularly put away money for big-ticket items and trips, but today they’re releasing something new: IFTTT (If This Then That) functionality. Now you can set up savings triggers to automatically put money toward savings goals every time you buy from Starbucks or walk another mile. Qapital hopes this new feature gets more millennials saving toward their goals—and maybe paying more attention to just what they’re spending their money on.

Qapital grew out of the Swedish financial tech scene, built by ex-bankers who saw opportunity in millennials’ irregular saving behaviors. Qapital first built a Mint-like service for Swedish users to track their finances, but decided to build a completely new product in the U.S. The U.S. market was a better pitch for venture capitalists, says Qapital CEO and cofounder George Friedman, but U.S. financial startups had already created data access pipelines to data from big U.S. banks. Qapital partnered with one of these, Plaid, so Qapital could focus on their service.

“American banks are much more open to innovation, believe it or not. The API for bank data is available in the U.S.,” says Friedman. “So [partnering with Plaid] helped us go to market, because in Sweden, we would have had to build in all funnels to banks ourselves. With partners, we can be the front end layer, and now we’re 100% focused on the U.S.”

If millennials were any better at saving money or any worse at game-playing, the team behind Qapital might not have created its new personal finance app quite the way it did. “Behavioral finance has been talked about this for years— it’s about defaulting and trying to come up with ways that work for you in a personal level,” Qapital CEO and cofounder George Friedman told.

Qapital will release its own branded Visa debit card through the bank that backs all Qapital accounts, the Iowa-based Lincoln Savings Bank. Qapital partnered with Intuit (which makes the finance software behind Quickbooks), which expanded Qapital’s dynamic IFTTT recipe features to users with accounts at over 20,000 smaller banks across the U.S.

American users can set up separate FDIC-insured Qapital-branded savings accounts into which they can automatically drop money from their existing checking accounts. Being able to use IFTTT recipes to link Qapital users’ walking, buying, or even web surfing behaviors with financial planning expands the saving service into something of a lifestyle app. Rewarding yourself with a deposit every time you reach a goal creates a positive feedback loop, while depositing money in your savings account every time you buy a latte can really make you think twice before you pony up for fancy coffee.

Setting up a savings goal on Qapital’s mobile app (available for just iOS for now, but on Android by the end of the year) is simple: Name a goal and a financial target, and choose a photo (this is key to helping you emotionally invest in your goal). Boom, you now have a bucket to catch deposits for your particular financial goal.

Setting up a savings goal on Qapital’s mobile app (available for just iOS for now, but on Android by the end of the year) is simple: Name a goal and a financial target, and choose a photo (this is key to helping you emotionally invest in your goal). Boom, you now have a bucket to catch deposits for your particular financial goal.

Setting up a rule to trigger a deposit toward that goal is a little more involved: Choose a savings model and log in to Qapital’s IFTTT page to choose what “recipe” actions—like posting on Facebook or closing an issue on Github or achieving your daily step goal—triggers a money transfer from your personal debit account toward that specific goal on your Qapital account. Note that the action’s platform (Facebook, Github, your phone’s step counter) must have IFTTT functionality—you can look up which services do on IFTTT’s website.

Qapital has only been testing the IFTTT functionality within its team and a handful of outsiders; so far, it can only guess which recipes and saving methods will be most popular—or, indeed, if behavioral saving will push millennials to save more than they currently do. That Qapital is aiming straight for millennials is certain: The app is a lean, pretty tool (built by designer twins Daniel and Andreas Källbom of Studio Källbom, who helped build Spotify’s mobile apps) with plenty of real estate devoted to photos that represent your goals.

But it’s Qapital’s positive approach to saving that speaks most to cash-strapped millennials: Instead of the restrictive negativity of budgeting, Qapital focuses on goals, on saving while you spend.

Basically, Qapital connects to 184 apps, including Facebook, Twitter, Dropbox, Uber, GitHub, ESPN, and Instagram, and prompts users to save money in an online account using a variety of “recipes.” For example, you can trigger a few dollars worth of savings each time you do something you want to do, like walk a mile or remember to turn down a connected thermostat.

With social apps, you can “fine” yourself for doing too many updates on Facebook, or reward yourself by saving money for using a specific hash tag on Twitter, or posting a photo on Instagram. You can save a few bucks every time the temperature dips below 30 degrees in the winter and see how close you are to your savings goal for that trip to Thailand with an image of a beach in Phuket, or say the temples of Bangkok to rev up your savings.

“We realized kind of early that the data and the picture you painted for people was pretty depressing—it was like ‘I’m spending too much money,’ and ‘No more please,’” Friedman said.

Yet a full one-third of millennials had no savings account, with those under 35 found to be saving at a negative 2 percent rate, meaning they spend more than they’re making and are either going into debt or depleting their savings, according to Moody’s Analytics.

Nobody enjoys filing taxes. But for freelancers and contractors, the process is even more complicated, in part because they can be required to pay estimated taxes on a quarterly basis, and face steep penalties if they miss those deadlines.

Dubbed the Freelancer Rule, Qapital’s new tool will automatically take a predetermined percentage out of your paycheck—say, 30%—and set it aside for estimated taxes. (It’s not too different from how your employer withholds taxes from your paycheck if you’re a full-time staffer.) When the IRS comes knocking, Qapital users simply have to fork over that money, rather than scrambling to make the payment.

Qapital is by and large targeting a younger crowd: The app was founded to capitalize on uneven millennial saving practices. In June 2015, the company introduced IFTTT (If This Then That) functionality, which meant users could set up savings goals based on their spending habits or other actions; if they spent x number of dollars on coffee, they should then put away y number of dollars into their savings account. “It’s moving away from calculation and toward that goal you emotionally care about,” Qapital CEO George Friedman told Fast Company earlier this year.

About 38% of millennials are freelancing now, as compared to 32% of the rest of the U.S. population, making Qapital’s latest move yet another play for the under-35 set.

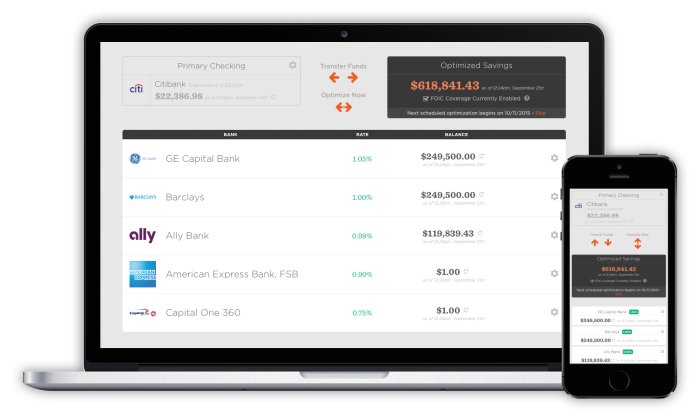

MaxMyInterest (US)

When Gary Zimmerman sold his apartment to work overseas, he stashed the proceeds in his bank account. He soon realized not only was he above the $250,000 FDIC insurance limit, leaving his money potentially at risk, but he was also earning close to nothing in interest. He started spreading out the funds to different banks, keeping accounts below the FDIC limit at any single institution, and also seeking out the highest interest rate possible.

When Gary Zimmerman sold his apartment to work overseas, he stashed the proceeds in his bank account. He soon realized not only was he above the $250,000 FDIC insurance limit, leaving his money potentially at risk, but he was also earning close to nothing in interest. He started spreading out the funds to different banks, keeping accounts below the FDIC limit at any single institution, and also seeking out the highest interest rate possible.

After managing the money with the help of a spreadsheet for several years, he realized he had made an extra $40,000 by being such an active manager of the bank account funds. He wanted to continue reaping those rewards without spending so much time moving the money by hand, and that’s what gave him the idea for MaxMyInterest, which automates that manual process. “I realized this wasn’t just a solution for me, but a lot of people would benefit,” he says.

“It’s effectively free money, so it’s a massive opportunity to earn cash,” he says, adding that given how much money Americans keep in cash, they could collectively earn an extra $50 billion in interest a year if everyone pursued this strategy. While high-net worth individuals with a lot of cash have the most to gain, Zimmerman calculates that a person with $50,000 in savings could earn an extra $450 a year with the tool, while someone sitting on $200,000 would keep an extra $2,200.

MaxMyInterest doesn’t disclose its number of users, but Zimmerman says the average customer in the system has about $700,000 in cash, and amounts range from $50,000 to $5 million. The company also has plans to expand, starting with helping users collect all their 1099 tax forms. “We’re trying to make online banking much simpler,” he says.

PFM from neobanks Moven (US) and Fidor (Germany)

This debit account calls itself the “anti-budgeting” app that helps people make smarter spending decisions. “We wanted to create an experience where people could be in control of their money and build better behaviors,” explains Alex Sion, co-founder of the Moven. Users can see their remaining funds after each purchase, and purchases can be made with mobile payment technology, so you don’t need your wallet. “It’s giving you real-time feedback,” Sion says, unlike a credit card, with which you might review your purchases weeks after making them, if at all.

This debit account calls itself the “anti-budgeting” app that helps people make smarter spending decisions. “We wanted to create an experience where people could be in control of their money and build better behaviors,” explains Alex Sion, co-founder of the Moven. Users can see their remaining funds after each purchase, and purchases can be made with mobile payment technology, so you don’t need your wallet. “It’s giving you real-time feedback,” Sion says, unlike a credit card, with which you might review your purchases weeks after making them, if at all.

After launching in March 2014, Sion says app users have been growing at about 100 percent each month, with tens of thousands of customers now in the U.S. Partnerships with banks are also extending the app’s reach and are expected to help the number of app users reach 4 to 5 million by the end of this year.

After launching in March 2014, Sion says app users have been growing at about 100 percent each month, with tens of thousands of customers now in the U.S. Partnerships with banks are also extending the app’s reach and are expected to help the number of app users reach 4 to 5 million by the end of this year.

For creating a social bank that leverages cutting-edge technology to respond to customer wishes. At first glance, Fidor seems crazy. It’s an online-only bank that would set the interest rates it paid on deposits according to the number of likes received on its Facebook page. Pretty meshuggener. But that’s not the only thing different about Fidor: It got its start as an online financial chat group. Frank Schwab, who runs technology for the bank, recalls the year was 2009 and financial institutions were crumbling one after another.

The online chat group was fed up with all the banking choices, and so the company began evolving based on its users’ ideas. Today, Fidor is something of a lab for social banking: It says it is now the biggest aggregator of web 2.0 services, including P2P lending and social trading, as well as classic bank products. Active Fidor users get bonuses for participating on the website, like ranking products or offering advice on the Fidor community forum.

“We have been updating our systems every two weeks for four years,” says Schwab. Global banks can’t hope to compete with that techno-nimbleness, and so tiny Fidor is leaping over the legacy systems. Last spring, it became the first bank to join forces with Ripple, a back-end Internet service that enables bank customers to send and receive any kind of currency, including Bitcoin, anywhere on the planet within seconds—all without the help of pricey middlemen.

Prism (US)

![]() Tyler Griffin wants to make it easier for people, especially millennials, to pay their bills each month. He co-founded the app Prism, which helps people pay their bills on time each month without having to sign up for automatic payments, which can lead to overdrawn fees if there’s not enough money in a checking account. “You don’t have to remember when bills are due. We figure it out and present it in a visual way, so people have the tools to pay bills as they want,” he says.

Tyler Griffin wants to make it easier for people, especially millennials, to pay their bills each month. He co-founded the app Prism, which helps people pay their bills on time each month without having to sign up for automatic payments, which can lead to overdrawn fees if there’s not enough money in a checking account. “You don’t have to remember when bills are due. We figure it out and present it in a visual way, so people have the tools to pay bills as they want,” he says.

The app connects to users’ bank accounts and bill paying accounts; payments are posted in less than an hour, he says. Automatic safeguards also help users avoid both late and overdraft fees. The app currently pays about $500,000 in bills each day, and 40,000 people are using the free product every month.

Credit Sesame (US)

Personal finance company Credit Sesame has raised an additional $16 million in an oversubscribed Series D round of funding, with plans to raise more – as much as $20 million – in the near future. The new round was led by Syncora Alternative Investments, with IA Capital Partners as its advisor, and also included participation from investors Menlo Ventures, IA Capital, Globespan Capital, Inventus Capital, and other high-profile angels.

Personal finance company Credit Sesame has raised an additional $16 million in an oversubscribed Series D round of funding, with plans to raise more – as much as $20 million – in the near future. The new round was led by Syncora Alternative Investments, with IA Capital Partners as its advisor, and also included participation from investors Menlo Ventures, IA Capital, Globespan Capital, Inventus Capital, and other high-profile angels.

This brings Credit Sesame’s total raise to date to over $35 million. The company was one of the first to market with solutions that allow consumers to monitor their credit and score, protect themselves against identity theft, and reduce their debt through credit and loan management services.

While many in the personal finance space have focused on helping people manage their money and investments, Credit Sesame has instead targeted the liability side of the balance sheet, explains CEO Adrian Nazari. That has put it in competition with others offering consumer debt management or credit monitoring, like Credit Karma or ReadyForZero, for example.

Credit Sesame’s service, which is available online and on mobile, offers consumers a way to track their debt, their credit, and their loans. And, when applicable, it can recommend savings after it analyzes a consumer’s individual debt situation, by pointing to other credit cards and loans that have better terms or lower interest rates, for instance. The company now has $50 billion in active user loans under management, up from $20 billion in 2012, and over $2 billion in consumer loan originations by its partners on the platform, which helps it to monetize. And that growth is accelerating.

The additional capital is being put to use to speed up customer acquisition, plus expand its credit and loan management services as well as the Credit Sesame team, which is now over 50, and will roughly double in size in the next 12 months. The company is also expanding its offices in San Francisco.

UK: Money Dashboard and Nutmeg

![]() Money Dashboard, the UK personal finance app that helps you understand why you’re broke, has raised some additional capital of its own. It’s secured a further $3.7 million in funding, meaning that the Scottish startup has raised $8.3 million in the last year. Private equity fund, Calculus Capital, led the round, while Ariadne Capital, Par Equity, and The Scottish Investment Bank also participated.

Money Dashboard, the UK personal finance app that helps you understand why you’re broke, has raised some additional capital of its own. It’s secured a further $3.7 million in funding, meaning that the Scottish startup has raised $8.3 million in the last year. Private equity fund, Calculus Capital, led the round, while Ariadne Capital, Par Equity, and The Scottish Investment Bank also participated.

Launched in 2010, Money Dashboard’s free app lets you monitor your online bank and credit card accounts and, in turn, keep tabs on your spending. It does this by automatically tagging items in your online statements, such as ‘grocery’ or ‘travel’, letting you get a better (and aggregated) view of expenditure and income by category, with the broader aim to help you budget more effectively. Its USP is that, unlike each bank’s own mobile app, Money Dashboard provides a consolidated view of your spending across multiple bank accounts and credit cards, supported by a central and somewhat smart dashboard.

Additionally, Money Dashboard sells anonymous spending data and trends to market research companies.

Nutmeg also was making good on its plan to provide a personal pension service for investors in the U.K. “We have listened to our customers and delivered what they truly want,” Nutmeg CEO Nick Hungerford said. “In an industry embroiled in hidden charges, fees and complexity, our transparency promise will be a welcome reassurance to customers.” The service is a partnership between Nutmeg, which will invest and manage the pensions, and Hornbuckle Mitchell, which will provide technology to serve and administer the pensions.

Nutmeg also was making good on its plan to provide a personal pension service for investors in the U.K. “We have listened to our customers and delivered what they truly want,” Nutmeg CEO Nick Hungerford said. “In an industry embroiled in hidden charges, fees and complexity, our transparency promise will be a welcome reassurance to customers.” The service is a partnership between Nutmeg, which will invest and manage the pensions, and Hornbuckle Mitchell, which will provide technology to serve and administer the pensions.

Founded in London in 2011, Nutmeg was recently named to the FinTech 50 and the KPMG Fintech Innovators for 2014. The company, whose name we saw on buses in London during our recent visit, raised $32 million from new investors a year ago in June, bringing its total capital to more than $50 million. Nutmeg was a Best of Show winner at Finovate Europe 2012.

MX aka MoneyDesktop (US)

MX, the personal finance startup formerly known as Money Desktop, has inked a $30 million Series A funding deal led by a subsidiary of USAA. Tokyo-based VC firm Digital Garage also participated in the round. MX previously raised a healthy seed round from various early-stage investors for $20 million late last year. This brings the total amount of funding to $50 million for the startup. MX founder Ryan Caldwell was hesitant to talk about the valuation, but we’ve heard it’s about triple the previous $100 million valuation. According to Pitchbook*, MX was worth $243 million pre-money and is now worth $273 million.

MX, the personal finance startup formerly known as Money Desktop, has inked a $30 million Series A funding deal led by a subsidiary of USAA. Tokyo-based VC firm Digital Garage also participated in the round. MX previously raised a healthy seed round from various early-stage investors for $20 million late last year. This brings the total amount of funding to $50 million for the startup. MX founder Ryan Caldwell was hesitant to talk about the valuation, but we’ve heard it’s about triple the previous $100 million valuation. According to Pitchbook*, MX was worth $243 million pre-money and is now worth $273 million.

Most of these competitors work by scraping financial data and connecting to APIs to offer a snapshot of where you are financially. MX differs in that it powers a backend money-management solution to the existing infrastructure of these financial institutions. This allows customers of those institutions to see all their financial information in one place within their own banking platform, rather than on a third-party site like Mint.

This latest round was a strategic one that will help MX to rapidly build out this backend with larger financial institutions, according to Caldwell. As an investor, USAA, one of the largest banking institutions in the United States, has incentive to help the startup work with its more than 10 million customers. In return, MX offers USAA a simplified personal finance solution that can “enhance the customer experience,” according to USAA.

The investment from Digital Garage offers another strategic opportunity for MX – helping it go overseas. Digital Garage was instrumental in helping other technology companies like Twitter and Path expand internationally and can offer a possibly lucrative opportunity for MX to get into the Japanese banking market – one of the leading centers for finance and banking in the world.

Social Money aka SmartyPig (US)

Q2 Holdings Inc., an Austin, Texas-based cloud-based banking software company, has acquired West Des Moines-based Social Money, the company that developed the SmartyPig social savings product. Q2 acquired all of the outstanding interests of Social Money in exchange for $10.6 million cash payable at closing, subject to a customary working capital adjustment. A Q2 spokeswoman said Social Money’s 12 employees will remain with the company at the West Des Moines office.

Q2 Holdings Inc., an Austin, Texas-based cloud-based banking software company, has acquired West Des Moines-based Social Money, the company that developed the SmartyPig social savings product. Q2 acquired all of the outstanding interests of Social Money in exchange for $10.6 million cash payable at closing, subject to a customary working capital adjustment. A Q2 spokeswoman said Social Money’s 12 employees will remain with the company at the West Des Moines office.

Social Money was founded in 2008 by Jon Gaskell and Michael Ferrari to roll out SmartyPig, a goal-based savings program in which savers use social media to announce goals and solicit participation from friends and family members. Its client list includes H&R Block and Sallie Mae.

Social Money will continue its relationship with existing clients while working directly within Q2’s research and development team to continue to establish innovative offerings for its digital banking channels, the company said. Q2 is evaluating the integration of Social Money’s portfolio and plans to begin offering a rebranded suite of Social Money technologies to its customer base starting in 2016.

Previously a West Des Moines financial company has joined a Bill and Melinda Gates Foundation mission to increase the savings power of low-income individuals. The Gates Foundation awarded Social Money a “seven-figure” grant to expand the use of its savings and banking platform in India.

Digit (US)

It’s only been a few short months since automated savings startup Digit opened to the public, but it’s already garnered serious interest from consumers who want more money in their bank accounts, as well as investors who think the service could eventually be a huge hit. Digit operates a simple platform for helping consumers to save money, by simply connecting to their bank accounts and gradually funneling money into a non-interest-bearing savings account. The service uses algorithms to track users’ spending behavior and moves money into savings in an automated fashion.

It’s only been a few short months since automated savings startup Digit opened to the public, but it’s already garnered serious interest from consumers who want more money in their bank accounts, as well as investors who think the service could eventually be a huge hit. Digit operates a simple platform for helping consumers to save money, by simply connecting to their bank accounts and gradually funneling money into a non-interest-bearing savings account. The service uses algorithms to track users’ spending behavior and moves money into savings in an automated fashion.

To keep growing, the company received $11.3 million in new funding led by General Catalyst, with participation from existing investors Baseline Ventures and Google Ventures, as well as former Visa President Hans Morris. The company has now raised a total of $13.8 million, and with the latest round, Taneja has joined its board. The company has seen pretty tremendous growth since then, with its user base increasing by 10x and its savings under management up 5x.

According to CEO Ethan Bloch, users are mostly coming to the service by word of mouth and referrals, although Digit has seen some coverage in the mainstream lifestyle press, as well as among some notable finance bloggers.

But the way they’re interacting with Digit shows the promise of the system: So far, only about a quarter of users have ever withdrawn funds that Digit has set aside for them. And another quarter of the company’s users set aside more money — usually when prompted to do so via one of Digit’s SMS messages.

Digit doesn’t have a mobile app for managing a budget or viewing your balance. Instead, its website is decidedly barebones, and most communications happen with users only through text. Users send SMS messages to view their balance, find out why their checking account balance changed, and also to withdraw or save more money.

While it plans to continue offering the same sort of simplified communications interface, Digit sees itself expanding its services and features to offer new options to users.

For instance, the company is working on creating a compliant way in which it could pay interest on its savings accounts. It’s also considering the ability to add overdraft protection to its suite of offerings. But the ultimate goal would be for Digit to automate all your financial needs, whether it be managing a savings account, paying recurring bills, lowering a user’s debt, or putting money away for retirement.

By monitoring a linked checking account’s spending patterns, Digit uses contextual analytics to determine when and how much to pull out of the linked bank account into a FDIC-insured Digit custodial account held at two of its partner banks, Wells Fargo and BofI Federal Bank. According to Digit’s 29 year old founder, Ethan Bloch, the app looks at the linked bank account balance every few days and considers a series of factors, including:

Is this a high or low balance based on how this person makes and spends money?

Do they have any bills coming due in the next several days?

Will they have any income in the next several days?

How much money did they spend yesterday?

How much did they spend over the previous several days?

How much have they saved so far this month?

“After answering questions like these, Digit tries to arrive at a small amount of money it knows the user won’t need, but more importantly, might not feel is missing based on recent spending and income,” states Bloch. Digit also has a ‘no overdraft’ guarantee, meaning if they accidentally overdraw the linked account, they’ll pay for any fees.

Photos: getty, Company profiles, fortune mag

Life. SREDA VC is a global fintech-focused Venture Capital fund with HQ in Singapore