China Tightens Restrictions on Insurance Purchases in Hong Kong

By Zheping Huang for the Quartz.com

China has issued new restrictions on citizens buying insurance in Hong Kong, the latest move to stem capital outflow and keep the renminbi strong.

Hong Kong insurers can no longer accept UnionPay, the massive Chinese state bank-card payment system that every Chinese credit or bank card runs on, insurers told Quartz and Bloomberg.

The restriction limits the ability of anyone holding one of these 5.3 billion cards (many Chinese citizens have multiple bank cards) from investing in Hong Kong insurance. Beijing already limits the amount of cash citizens can take out, and paper checks are rare in China, so this change essentially shuts down a popular avenue way to move money out of the mainland.

Chinese citizens worried about a weakening economy have been sending their money abroad, especially since the renminbi was unexpectedly devalued last August—an estimated $1 trillion fled China in 2015, seven times than the previous year. Hong Kong is a gateway for this capital flood, and investors from China turn to local real estate, money-changing shops, fake trade invoices, and other methods to transfer their net worth into another currency.

Hong Kong’s giant insurance industry has played a big part. The industry, which brought in 16% of Hong Kong’s GDP in the first half of 2015 and employs some 35,000 people, has increasingly catered to mainland clients, insurance agents tell Quartz. Mainland buyers were eagerly purchasing Hong Kong life insurance products, which were not included in China’s $50,000 per year of limit on capital citizens can take out of China.

A Hong Kong-based insurance agent from AIA, who asked not to be named, told Quartz that almost 95% of her customers come from the mainland, and policy sales have jumped since last August. “The rich people are sensitive to an economic downturn,” she said.

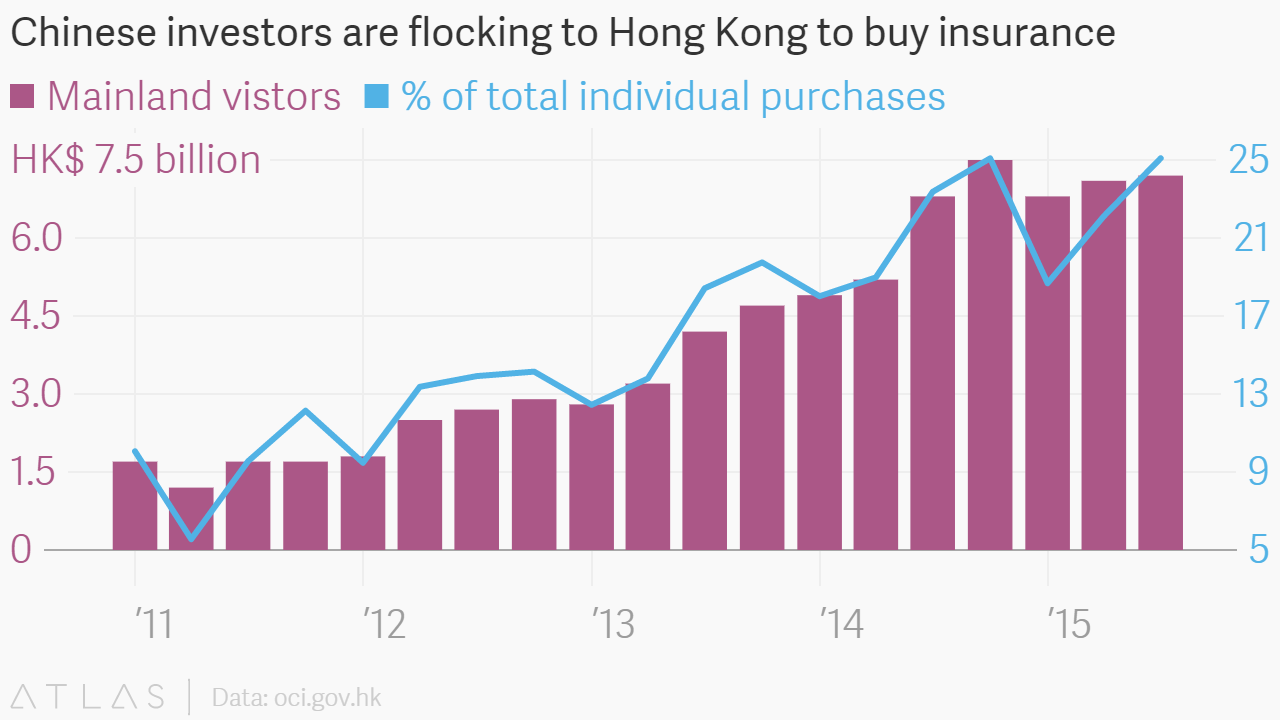

According to the latest figures from Hong Kong’s insurance commissioner office, mainland visitors spent HK$7.2 billion (nearly $1 billion) buying insurance policies in Hong Kong in the third quarter of 2015. That accounted for 25% of the total new premiums in individual policies during the same period, the highest over the past five years.

Notices viewed by Bloomberg show Hong Kong insurers stopped letting mainland customers purchase any life insurance and investment-related products via electronic payment system starting Mar. 12, based on advice from the People’s Bank of China, China’s central bank. Medical, accident, and transportation insurance are not limited, though, but have a cap of 30,000 yuan ($4,600), according to Bloomberg.

This is the second attempt to keep mainland cash from flowing into the Hong Kong insurance market. A February notice issued by China’s currency regulator limited insurance payments via UnionPay at $5,000 per transaction.

One notice issued by BOC Group Life Assurance, which is a subsidiary of the Bank of China, said any payments made by UnionPay bank cards through online payment provider All In Pay Network Services have been halted, a spokesman with the state-owned insurer told Bloomberg in a article that ran today (Mar. 14).

Not all Hong Kong insurance companies are banning UnionPay transactions yet, though. An employee with one of the major international insurers based in Hong Kong, who asked not to be named because he is not authorized to talk to the media, told Quartz his company accepts payments via UnionPay at up to $5,000 per transaction.

There is no limit at his company on mainland customers buying insurance products, he said. To get around the new ban, “one can have many bank cards” or “swipe a card many times” to pay, he said.

photo: Reuters/Bobby Yip

The article first appeaered in the Quartz.com