KPMG Report: Robo Advice Platforms Will Manage US$2.2 trillion Worth of Assets by 2020

By KPMG report, first publieshed by Fintechnews.ch

KPMG surveyed 1,500 bank clients about their awareness of and interest in digital wealth management, or robo-advisors.

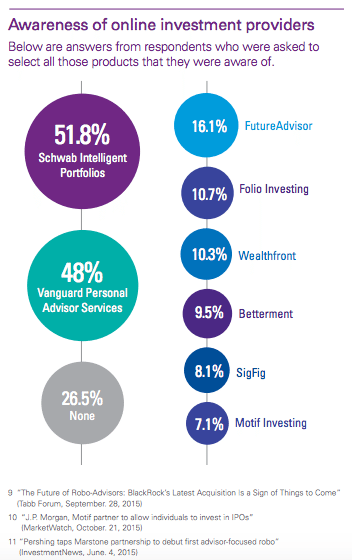

The firm found that while awareness of the robo advising services of popular fintechs including SigFig, Betterment, Wealthfront and FutureAdvisor (8% to 15%) was relatively low, interest in robo-advisor services was high, with 75% of respondents who said they were “very likely or somewhat likely” to consider robo advising services from their banks.

The factors that contributed to the growth of digital advice, according to KPMG, include the fact that these solutions provide increased transparency, increased accessibility through low or no minimums and fees, enhanced customer experience, as well as their use of exchange-traded funds to build diversified portfolios.

Hence, robo advisors often appeal to less-wealthy investors, given the availability of low-minimum and low-cost portfolios. These solutions also coincide with expanding interest in passive investing.

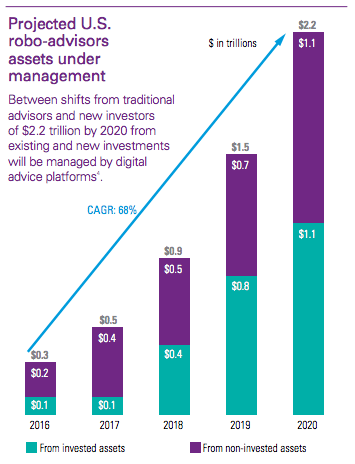

Digital wealth management is changing the investing landscape, the firm said. KPMG estimates that by 2020, robo advisors will be managing US$2.2 trillion in the US.

One population that is particular keen on online wealth management solutions is the millennial generation: 80% of respondents aged between 18 and 34 years old said they would be “very likely or somewhat likely” to consider using robo advisors.

Interesting fact:

“People spanning the financial spectrum are buzzing about “robo advisors,” automated, digital wealth management solutions that have proven attractive to both high net-worth clients and mass market customers. A quick Google search on the term produced more than 683,000 hits and 31,000 news results.”

KPMG advises banks:

“The opportunity for banks is ripe, but you must act now to capture your share of the market. Otherwise your clients will eventually look for these solutions at other institutions.”

Banks should address these points when considering launching a robo advising solution:

Competitive realities: Robo advising might not be right for every traditional bank. How critical is it for a bank to respond to rapidly changing market dynamics? How will the organization differentiate its digital advice offering?

Product options: Digital advice providers generally offer diversified portfolios of low-cost ETFs across multiple asset classes. What product solutions will be offered? What specific bank-brokerage capabilities can a bank leverage to provide compelling and competitive products?

Client opportunities: Existing bank clients are prime targets for robo advising services. What portion of banking clients have investing accounts with an affiliated brokerage?

Cultural capabilities: Banks are expanding investing access to more of their clients and are introducing broader bank-brokerage offerings. Hence, there needs to be increased cooperation and coordination to create a seamless, unified customer experience.

Investing approach: Digital advice is a strong fit for passive investing as executed through a wide range of ETFs. Do internal stakeholders and clients understand the passive investing philosophy and the role ETFs can play? Are they familiar with ETF securities or interested in learning about them? How can a firm’s asset management expertise be leveraged to create competitive and differentiated portfolio offers?

Digital strategy: Access to banking and investing products and services are expanding, and clients are increasingly expecting a unified user experience. What degree of Web and mobile integration currently exists? Do clients have a single sign-on to their accounts via the Web and mobile applications or multiple and distinct platforms?

Partnership opportunities: In many cases, partnerships are be the best approach to debuting robo investing solutions. What potential partners are available to work with?

The article was first published in Fintechnews.ch