On the move

Speacial by the Economist

Much hangs on mobile money

FROM HIS SHACK in Kangemi, a slum at the western edge of Nairobi, Gilbert Onduko sells bare essentials to his neighbours. A blackboard above the hatch lists prices for ugali(maize cooked into a sort of porridge), farina (similar to semolina) and cooking oil. On the roof of the shack is a small solar panel, about the size of a tea tray, which powers two lights inside and a mobile phone. Since he got it, about a month before your correspondent visited, Mr Onduko has been able to keep his shop open until midnight rather than just in the daytime. He has also cut down his kerosene bill by 100 shillings (about $1) a day—a hefty saving in a Nairobi slum. “And now my phone is always charged,” he grins.

Mr Onduko’s story shows how electricity can improve Africans’ lives. But it also shows what access to credit can do. It was not technology that was stopping shopkeepers in Nairobi’s slums from having electricity. Indeed, power lines run within sight of Mr Onduko’s shop. The problem has been that connecting to the grid, and paying the bills, is beyond the means of most slum-dwellers. To get his solar panel, all Mr Onduko needed was a mobile phone and a deposit of about 3,500 shillings. The rest he can pay for on tick. Each day he sends 50 shillings via his mobile to M-Kopa, the firm that provides the solar panels. That keeps the machinery going, and within about a year he will own it. M-Kopa, which means “to borrow” in Swahili, has made its name selling solar panels, but it is rapidly becoming one of east Africa’s most innovative financial companies.

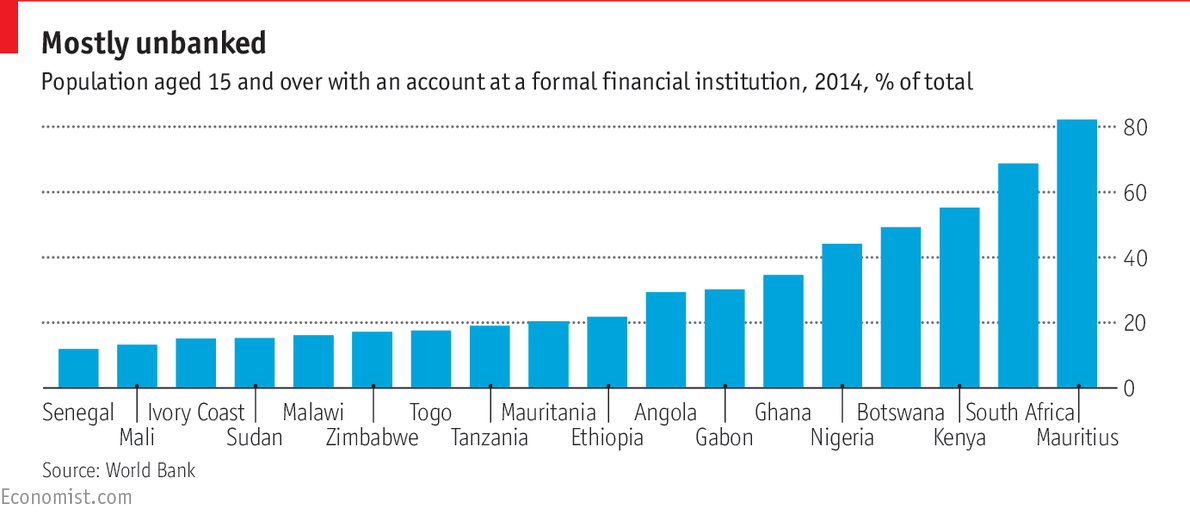

Mobile and internet technology is transforming industries across the world, but Africa has more potential than most because the existing infrastructure falls so far short of people’s needs. Executives talk exuberantly about how the continent is “leapfrogging” the West through technology. A lot of this is wishful thinking. Drones, for instance, seem unlikely to become a substitute for roads. But the revolution in finance is real. According to the World Bank, between 2011 and 2014 the proportion of adults in sub-Saharan Africa who have a mobile-money account increased from 24% to 34%.

East Africa is one of the most developed markets. Some 58% of Kenyans use mobile-money services, overwhelmingly M-Pesa. And as M-Kopa shows, such mobile services offer more than just a means to transfer money. Mobile phones can provide an address book, a credit rating and a distribution network all in one. Together, those things can allow even very poor people to acquire assets with their earnings, setting them on the path to becoming middle-class.

M-Kopa’s offices in Nairobi show all the signs of a tech startup. Table-football and table-tennis sets glow in the equatorial sun. The adjacent call centre is alive with the sound of employees touting for new business. When customers are reaching the end of their loan terms, M-Kopa agents call them to see if there is anything else the company can sell them. If customers wish, they can extend their loans and upgrade their solar set to a bigger one that can support a television.

M-Kopa also sells fuel-efficient cooking pots and smartphones, and would like to supply a small refrigerator, too. It has sold around 325,000 solar panels so far, and 50,000 of their buyers have already paid off their loan and then bought a cooking pot, a television or a smartphone. The customers’ repayments records offer an effective way of judging their creditworthiness. Pay off your solar panel quickly and you are probably worth lending more to, explains Jesse Moore, the firm’s American founder.

M-Kopa is far and away the most successful of the African firms innovating on top of mobile technology, but it is not the only one. Insurance is one promising area. Milvik, a multinational microfinance firm known outside Africa as Bima, now sells life insurance in four African countries, Tanzania, Uganda, Ghana and Senegal, partnering with insurance businesses and telecoms providers. Agents sign up customers, and the premiums—typically about 2 US cents per day—are taken automatically from mobile-phone top-ups. Over 95% of customers earn less than $10 a day. The policies promise a $1,000 payout in the event of an unexpected death.

The mobile-telecoms operators are not doing much to promote innovation. Though most Africans now own mobile phones, these are generally cheap and dumb, and since most Africans are poor, they do not spend much on accessing the internet. Unlike in the West, therefore, it is hard to reach a mass market with a good app. Instead, mobile operators load apps directly onto SIM cards and keep the data they generate in-house.

By far the most successful is Safaricom. It has a loans service called M-Shwari, and has worked with Kenyan banks to try to integrate its service. But even the firm’s executives admit there is far more it could do. Safaricom has declined to turn itself into a bank, but says it is opening up M-Pesa to other developers. It wants to become a “platform” rather than just a mobile-telecoms provider, but it has a long way to go, and its monopoly does not provide the best incentive.

Keep innovating

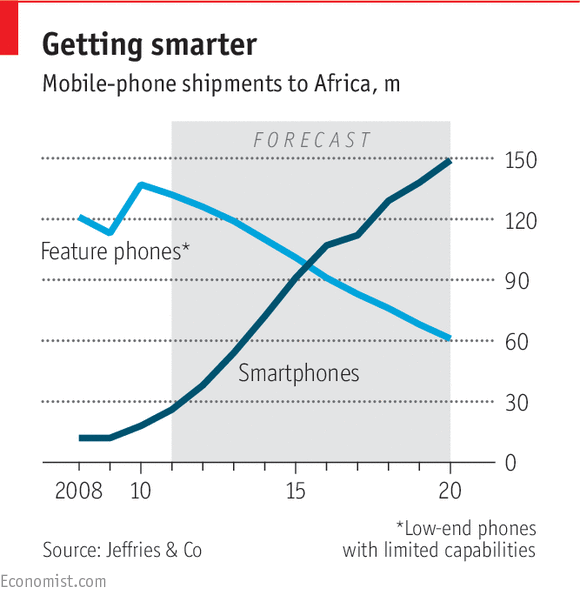

In the meantime the best hope is any innovation that gets around M-Pesa’s monopoly power. The rise of smartphones and feature phones (which can be preloaded with apps) will help. By 2020 over half of Africans will have access to smartphones with mobile broadband, reckons the GSMA, which represents mobile-phone operators worldwide. But given the right technology, even dumb phones can be useful. Counterintuitively, a promising source of innovation could be the banking sector, which has a strong interest in not letting mobile-telecoms operators steal its actual or potential customers.

In the Democratic Republic of Congo, one of Africa’s largest and least functional countries, the number of people with bank accounts has increased from just 50,000 in 2005 to over 3m in a population of about 80m. A government programme to pay state employees by bank transfer instead of in cash has helped. But so too has innovation. Trust Merchant Bank (TMB), the country’s biggest, has developed a voice app for its customers that works a little like telephone banking in the West: customers can carry out a mobile transaction by making a phone call or sending a text message, avoiding the need for an app. In Congo, unlike in much of east Africa, mobile-money transfers have not so far taken off, probably because the infrastructure is missing. TMB is hoping that it can beat the telecoms firms to the chase.

Another innovator is Equity Bank, a Kenyan firm with operations across east Africa. In Kenya it has launched its own mobile-phone company, Equitel, which uses the network of Airtel, another mobile operator, but exists mainly to provide banking services. It offers a “thin SIM” which can be overlaid onto an existing SIM card so that a phone can access two networks at once. That allows banking to be carried out through a dumb-phone SIM app without giving up the benefits of making phone calls and sending text messages through the dominant provider.

So far, this innovation looks better on paper than in practice. The reason why Equitel’s thin SIM has not been taken up in huge numbers, observers of the bank reckon, is probably that it costs 500 shillings to buy, which for most Kenyans is a hefty sum. But Equitel now has some 1.5m subscribers, all of whom also have a bank account with Equity. TMB has not released numbers for users of its app. But increasing access to banking—not just to mobile money—will be key to opening up other businesses such as M-Kopa.

There are other areas that phone companies could usefully tackle. For example, mobile money has not yet made much progress in international money transfers, where it could lower the cost of remittances. And even money-transfer services within national borders are still very expensive. Few in the West would use Safaricom’s M-Pesa to send money to relatives and friends: the transaction fee can eat up as much as 10% of the value of the transfer. The only place where mobile money is often preferred to cash for small transactions is Somaliland, the autonomous and peaceful northern part of Somalia. The main system there is on a network run by Dahabshiil, a firm that started as a remittances business and bank rather than as a telecoms provider. In contrast to almost everywhere else in Africa, making payments in Somaliland is free.

Mobile money has been one of east Africa’s great successes over the past decade. Not only has it created business opportunities, it is a big revenue generator for government: in Kenya, Safaricom pays more taxes than any other firm. But if growth is to continue, telecoms firms will either have to open up voluntarily or have their monopolies broken. Most Africans still do not have access to proper loans, insurance or savings facilities. Even the wealthy keep their money in cash and property; the poor rely on buying physical assets. Firms such as M-Kopa have made a start, but there is plenty more to do.