The Top 10 Insurtech Trends For 2017 That Set The Digital Insurance Agenda

By Roger Peverelli and Reggy de Feniks

The beginning of the year is usually the time to predict key trends for the year to come, and so it goes with the insurtech sector as well. Most lists focus on the latest sexy technologies and applications, but after a year, we find these have hardly gained any traction, so cannot really be considered “trends”. To call something a key trend, new and innovative isn’t enough. It requires adoption at scale. We therefore decided to take a different approach, resulting in quite a different kind of list.

Being consultants for several blue chip insurers, speaking at conferences and attending boardroom meetings, we meet insurance executives on a daily basis. Consequently, we have a fairly good idea about what’s at the top of their agenda, as well as the pace in which change will take place, and in turn what insurtech solutions are most likely to fit into those plans. These insights resulted in our Top 10 Insurtech Trends for 2017, illustrated by some awesome insurtechs that joined us at the previous DIA event.

Trend 1 (continued). Massive cost savers in claims, operations and customer acquisition

Already a major trend of course, but one that will gain even more importance in 2017.

Quite a few insurers face combined ratios that are close to 100, or even exceed that number. Digitalising current processes is absolutely necessary, for operational excellence and to cut costs. Digital transformation of insurance carriers started in 2015, really took off in 2016, and will be mainstream by 2017 and beyond. Virtually every insurer, big or small, that takes itself seriously will continue to look for ways to operate more efficiently in every major part of the costs column: in claims expenses, costs of operations and customer acquisition costs. Technology purchases and investments by insurance carriers will further explode in these areas, as will the number and growth of insurtechs that cater to that need.

With OutShared’s CynoClaim solution more than 60 percent of all claims can be managed automatically, resulting in lower costs as well as increased customer satisfaction. Results of the first implementations: up to 50 percent decrease in costs, 40 percent increase in customer satisfaction. The solution takes 6 to 9 months to implement, whether it is from scratch or a migration of established operations to the platform, which is quite spectacular in the insurance industry. Check out http://bit.ly/2hOW1Vw

OutShared on stage at DIA 2016 Barcelona

Trend 2. A new face on digital transformation: engagement innovation

At the end of the day, digitalised processes and a lower cost base are table stakes. It is simply not enough to stay in sync with fast changing customer behaviour, new market dynamics and increasing competitiveness. No insurer ever succeeded in turning operational excellence into a competitive advantage that is sustainable over the long term, and that is something really differentiating. More and more carriers realize that engagement innovation is the next level of digital transformation. From a customer point of view this is not about a new lipstick or a nose job but about a real makeover. Engagement innovation not only includes customer experience, but customer-centric products, new added value services and new business models as well. Insurtechs that really innovate customer engagement for incumbents have a great 2017 ahead.

Amodo connects insurance companies with the new generation of customers. With Amodo’s connected customer suite, insurers leverage on digital channels and connected devices such as smartphones, connected cars and wearables to acquire and engage new customers.

Amodo collects data from smartphones and a number of different connected consumer devices in order to build holistic customer profiles, providing better insights into customer risk exposure and customer product needs. Following the analysis, risk prevention programs, individual pricing as well as personalized and “on the spot” insurance products can be placed on the market, increasing the customer’s loyalty and customer lifetime.

Trend 3. Next level data analytics capabilities and AI; to really unlock the potential of IoT

Many insurance carriers have started IoT initiatives in the last few years. In particular, in car insurance it is already becoming mainstream, with Italy leading the pack. Home insurance is lagging and health and life insurance is even more behind. All pilots and experiments have taught insurers that they lack the right data management capabilities to cope with all these new data streams. Not just to deal with the volume and new data sets, but more importantly to turn this data into new insights, and to turn these insights into relevant and distinctive value propositions and customer engagement. Insurtechs that operate in the advanced analytics space, machine learning and artificial intelligence hold the keys to unlock the potential of IoT.

2016 DIAmond Award winner BigML has built a machine learning platform that democratizes advanced analytics for companies of all sizes. You don’t have to be a PhD to use its collection of scalable and proven algorithms thanks to an intuitive web interface and end-to-end automation. Check http://bit.ly/2iai2gq

Trend 4. Addressing the privacy concerns

To many consumers big data equals big brother, and insurers that think of using personal data are not immediately trusted. Quite understandable. Most data initiatives of insurers are about sophisticated pricing and risk reduction really. Cost savers for the insurer. However, the added value of current initiatives for customers is limited. A chance on a lower premium, that’s it. To really reap the benefits of connected devices and the data that comes with it, insurers need to tackle these data privacy concerns. On the one hand, insurers need to give more than they take. Much more added value, relative to the personal data used. On the other hand, insurers need to empower customers to manage their own data. Because at the end of the day, it is their data. Expect fast growth of insurtechs that help insurers to cope with privacy issues.

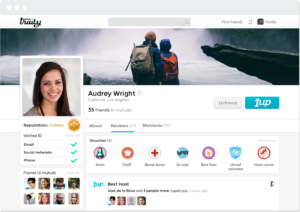

Traity (another 2016 DIAmond Award winner) enables consumers to own their own reputation. Traity uses all sorts of new data sources, such as Facebook, AirBnB and Linkedin, to help customers to prove their trustworthiness. Munich Re’s legal protection brand DAS has partnered with Traity to offer new kinds of services. Check http://bit.ly/2hlOFrm

Trend 5. Contextual pull platforms

Markets have shifted from push to pull. But so far most insurers have made hardly any adjustments to their customer engagement strategies and required capabilities. In 2017 we will see the shift to pull platforms, as part of the shift to engagement innovation. Whereas push is about force-feeding products to the customer, pull is about understanding and solving the need behind the insurance solution and being present in that context. Risk considerations made by customers usually don’t take place at the office of an insurance broker. Insurers need to be present in the context of daily life, specific life events and decisions, and offer new services on top of the traditional products. Insurtechs that provide a platform or give access to these broader contexts and ecosystems help insurers to become much more a part of customer’s lives, be part of the ecosystem in that context and add much more value to customers.

VitalHealth Software, founded among others by Mayo Clinic, has developed e-health solutions, in particular for people with chronic diseases such as diabetes, cancer and Alzheimer’s. Features include all sorts of remote services for patients, insurers and care providers collaborating in health networks, access to protocol-driven disease management support. All seamlessly integrated with electronic health records. VitalHealth Software is used by insurers that are looking to improve care as well as reduce costs at the same time. Among other OSDE, the largest health insurer in Argentina and Chunyu Yisheng Mobile Health, a fast-growing Chinese eHealth pioneer with around 100 million registered users that is closely linked to People’s Insurance Company of China (PICC).

Trend 6. The marketplace model will find its way to insurance

Marketplaces; we already see the model emerging in banking, and insurance will follow fast. Virtually every insurer offers a suite of its own products. Everything is developed in-house. More and more carriers realise that you simply cannot be the best at everything, and that resources are too scarce to keep up with every new development or cater to each specific segment. In the marketplace model, the insurers basically give their customers access to third parties with the best products, the most pleasant customer experience and the lowest costs. The market place business model cuts both ways. Customers get continuous access to the best products and services in the market. And costs can be kept at a minimum through connecting (or disconnecting) parties almost in real time to key in on new customer wishes and anticipate other market developments. In 2017 we will witness all sorts of partnerships between insurtechs and incumbents that fit the marketplace model.

AXA teamed up with the much praised 2016 DIAmond Award winner Trōv to target UK millennials. Trōv offers customized home insurances by allowing coverage of individual key items rather than a one-size-fits-all coverage set with average amounts. Check http://bit.ly/2gGwiBK

Trend 7. Open architecture

A new ecosystem emerges. With parties who capture data (think connected devices suppliers), and parties that develop new value propositions based on the data. Insurers will have to cooperate even more than they are currently doing with other companies that are part of the ecosystem. When an insurer wants to seize these opportunities in a structural way, then it is no longer only about efficiently and effectively organizing business processes , but it is also about easy ways to facilitate interactions between possibly very different users who are dealing with each other in one way or another.

Again, banking is ahead of insurance. For our new book, ‘Reinventing Customer Engagement. The next level of digital transformation for banks and insurers’, we spoke to many executives in banking as well. German Fidor Bank has set up an open API architecture called fidorOS, enabling fintechs to develop financial services themselves on top of an existing legacy system. Citi says that ‘any financial institution that doesn’t want to rapidly lose market share, needs to start working in a more open architecture structure.’

The Backbase omnichannel platform is based on open architecture principles. It leverages existing policy administration systems capabilities and adds a modern customer experience layer on top. Creating direct-to-consumer portals and giving the opportunity to integrate best of breed apps as well as improving agent and employee portals. Swiss Re, Hiscox and Legal & General are some of the insurers that use the Backbase platform. Check http://bit.ly/2hlZWZ2

Backbase DEO Jouk Pleiter on stage at DIA 2016 Barcelona

Trend 8. Blockchain will come out of the experimentation stage

When Goldman Sachs, Morgan Stanley and Banco Santander decided to leave the R3 Blockchain Group many thought this was proof that blockchain technology apparently was not as promising as initially expected. The contrary is true. It is not uncommon to join a consortium to speed up the learning curve, and then drop out and use the newly acquired knowledge to build your own plans and gain some competitive advantage. Especially with a technology as powerful as blockchain. We believe a similar scenario will not take place in the B3i initiative launched by AEGON, Allianz, Munich Re, Swiss Re and Zurich. Thinking cooperation and ecosystems are just much more in the veins of the insurance industry. Plus there are plenty of use cases that cut both ways: improve operational excellence and cost efficiency as well as customer engagement. Which is good news for the insurtech forerunners in blockchain technology.

Everledger tackles the diamond industry’s expensive fraud and theft problem. The company provides an immutable ledger for diamond ownership and related transaction history verification for insurance companies, and uses blockchain technology to continuously track objects. Everledger has partnered with all institutions across the diamond value chain, including insurers, law enforcement agencies and diamond certification houses across the world. Through Everledger’s API, each of them can access and supply data around the status of a stone, including police reports and insurance claims. Check http://bit.ly/2ialGHp

Trend 9. Use of algorithms for front-liner empowerment

Algorithms that are displacing human advisers generate headlines. Robo advice will for sure impact the labor market’s landscape. For a costs perspective this may seem attractive. But from a customer engagement perspective this may be different. To relate to their customers, financial institutions need to build in emotion. Humans inject emotion, empathy, passion, creativity, and can deviate from the procedure if needed. Banks and insurers need to create a similar connection digitally. With so many people working at financial institutions there is also an opportunity to create the best of both worlds. We see the first insurers that deploy robo advice to empower human front-liners. This is resulting in better conversations, higher conversion and finally, greater solutions for customers.

AdviceRobo provides insurers with preventive solutions combining data from structured and unstructured sources and machine learning to score and predict risk behavior of consumers. For instance predictions on default, bad debt, prepayments and customer churn. Predictions are actionable because they’re on an individual customer level and support front-liners while speaking to customers.

Trend 10. Symbiotic relationship with insurtechs

Relationships between insurers and insurtechs will become much more intense. All the examples included in the previous nine trends make this quite clear. Insurers will also look for ways to learn much more from the insurtechs they are investing in. Whether it is about specific capabilities or concrete instruments they can use in the incumbent organization, or whether it is about the culture at insurtechs and the way of working. We see an increasing number of insurers that are now using lean startup methodologies and who have created in-house accelerators and incubators to accelerate innovation in the mothership.

The Aviva Digital Garages in London and Singapore are perfect examples. They are not idea labs, but the place where Aviva runs its digital businesses. Varying from MyAviva to some of the startups Aviva Ventures invests in – all under one roof to build an ecosystem and create synergies on multiple levels.

This Top 10 of Insurtech trends that we will witness in 2017 sets the stage for the Digital Insurance Agenda. It reinforces the need to connect insurance executives with insurtech leaders which is basically our mission. It helps us to create an agenda for DIA 2017 Amsterdam that is in sync with what insurers need and what the latest technologies can provide.

DIA Amsterdam will take place on 10 and 11 May 2017.

DIA Amsterdam will take place on 10 and 11 May 2017. Life.SREDA relations enjoy a special 200 euro additional discount. You can use the discount code DIA2017LIFESREDA200 during the registration process to redeem this offer.