As Challenger Banks Grow In Popularity, Incumbents Must Innovate

Using technology and digital channels, challenger banks are reimagining banking, delivering superior digital customer experience and challenging incumbents to reinvent themselves.

These are growing in importance and incumbents must “transform themselves from slow moving caterpillars to agile butterflies,” according to a report titled Bank X: The New New Banks by Citi Research.

These challenger banks that are also sometimes referred to as neo banks, are designed around meeting current customer expectations and leverage data insights to offer better personalization and fully digital banking experiences.

These tend to be quicker at incorporating new products and processes onto their platforms, and offer more choices to end users by connecting with third-party products.

The report, released in March, outlines three categories of challenger banks: the standalone challenger banks, the incumbent-led challenger banks, and the bigtech-led challenger banks.

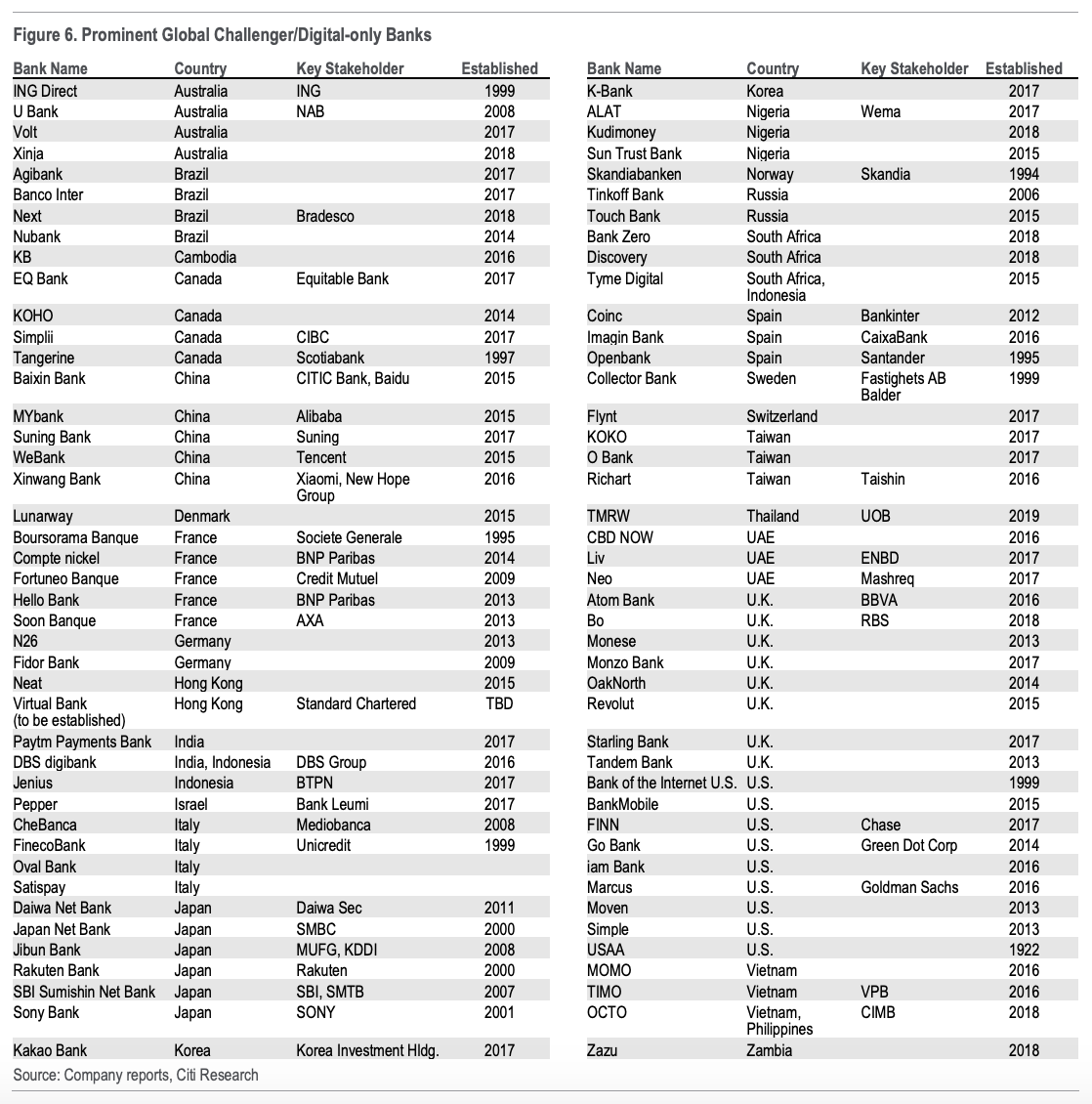

Prominent Global Challenger, Digital-only Banks, Bank X: The New New Banks, Citi GPS- Global Perspectives and Solutions, March 2019

Standalone Challenger Bank

The standalone challenger banks are primarily fintech companies leveraging technology and data to streamline retail banking by offering better convenience and pricing.

In the UK, these are for instance Starling, Atom, Tandem and Monzo, which all have banking licenses. Starling and Monzo Bank run on in-house developed technology, while Atom, Tandem, and others run on vendor solutions. Meanwhile, players like Revolut and Loot, also in the UK, are based on pre-paid cards and sit behind a third-party banking license.

Incumbent-Led Challenger Banks

The second category is the incumbent-led challenger banks. These are started within legacy banks through investment in technology and by creating new digital-only banks.

Examples of incumbent-led initiatives include ING Di-Ba, in which ING has owned a 100% stake since 2003. ING Di-Ba now has 8.8 million customers, including 1.7 million customer accounts.It has since rolled out similar models in Austria, France, Italy, and Spain.

Hello Bank, by BNP Paribas, is another prime example. It was founded in 2013 and now has more than 2.5 million customers across 5 countries.

Bigtech-Led Challenger Banks

Finally, the third and last category is the bigtech-led challenger bank. These are created through tech giants such as GAFA (Google, Apple, Facebook, and Amazon) and BAT (Baidu, Alibaba, and Tencent), which have been branching out into financial services. With their vast networks, the bigtech-led challenger banks are perhaps incumbents’ most daunting competition, the report states.

In particular, South Korea and China are successful examples of Internet companies venturing into banking. Citi GPS cites the case of South Korea’s popular social messaging app Kakao Talk, which launched a digital-only bank in 2017, acquiring two million customers in just two weeks from launch date.

Kakao Bank’s user base has continued to growth even in 2019, reaching around 6 million users, which accounts for about 15% of the country’s adult population.

In China, MYbank and WeBank, backed by Alibaba and Tencent, respectively, have seen strong user base growth following their launch in 2015. Leveraging Tencent’s social user base, WeBank now has 60 million customers in over 500 cities in China. Meanwhile, MYbank has leveraged Alibaba’s large merchant network on the e-commerce platform and has offered loans to over 5.7 million small and micro corporate users.

A Need for Banks to Reinvent Itself

To address the growing importance of challenger banks, Citi urges incumbents to reinvent themselves and reimagine banking.

This involves partnering with tech companies to create effective joint ventures as well as moving into more disruptive technology and business models to transform themselves into digital competitors, the report advises.

It cites the successful case of Goldman Sachs, which launched challenger brand Marcus to enter the mass market consumer financial services segment. Singapore’s DBS launched digibank in 2016 to enter the Indian and Indonesian consumer markets, and since then, other banks in Singapore have followed suits, including UOB and its new ASEAN challenger bank TMRW.

Regulators too seem to be reacting to this growing trend.

In Hong Kong, we’ve witnessed 8 licenses to issued to mostly incumbent-led and bigtech-led challenger banks. Similarly, Singapore is also considering issuing its own virtual banking license while its neighbour Malaysia is working towards launching its framework in November 2019.