Southeast Asia sees record startup funding in 2017

By Judith Balea for Tech in Asia

Funding for Southeast Asian startups hit yet another record in 2017, as late-stage companies attracted more investor backing. Activity also picked up in the series B or growth stage.

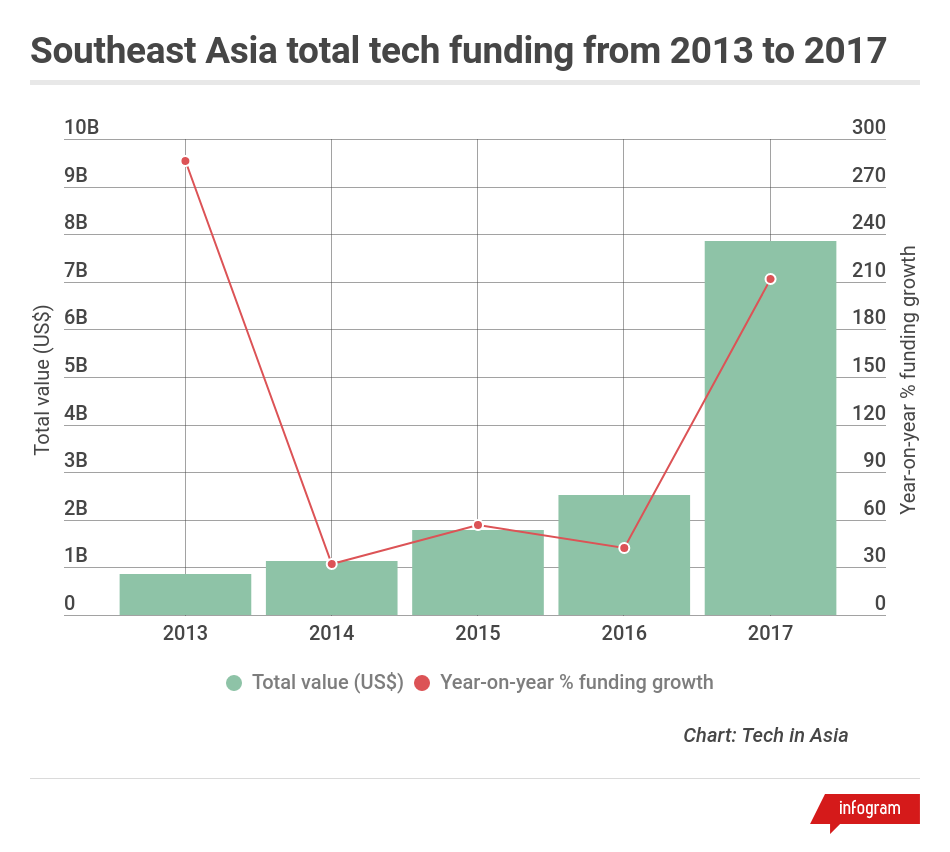

The region’s startups pulled in US$7.86 billion from investors last year, an over threefold rise from 2016’s US$2.52 billion, according to Tech in Asia’s data. That’s the highest growth since 2013 and came about despite the number of deals falling to 320 from 335.

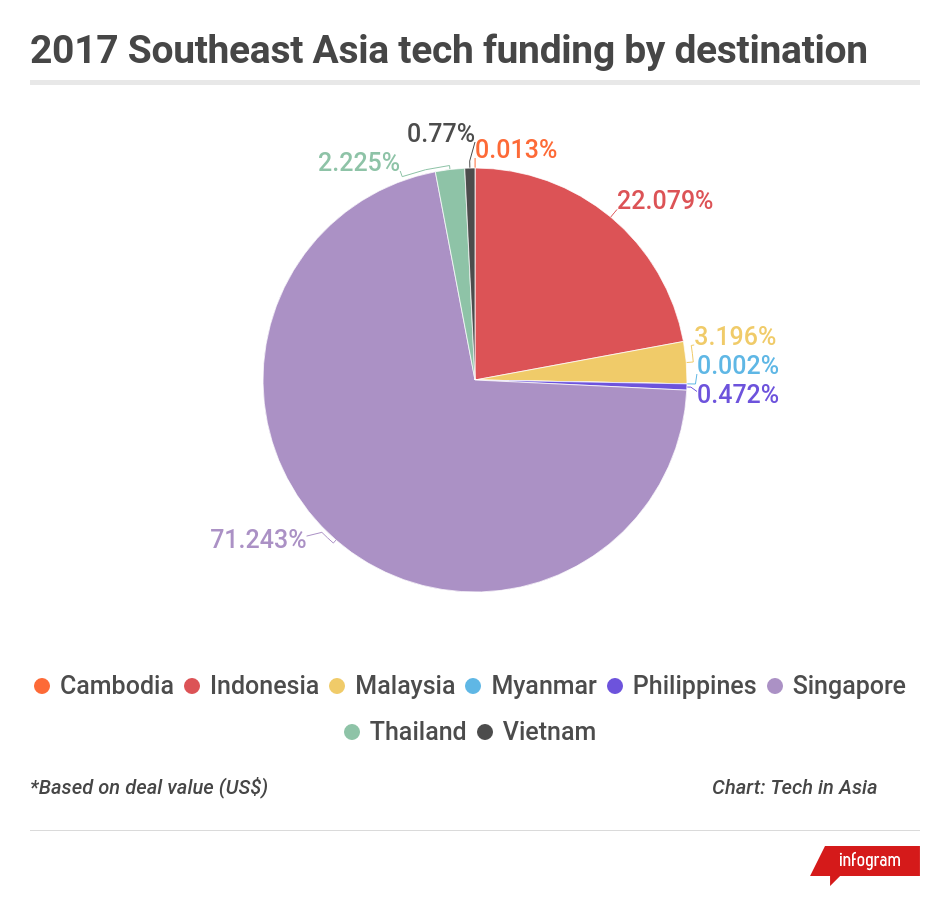

Singapore and Indonesia continued to figure prominently on investors’ radar, while fintech (US$3.18 billion), ecommerce (US$2.87 billion), and gaming (US$553 million) attracted the most investments.

Which stages performed well?

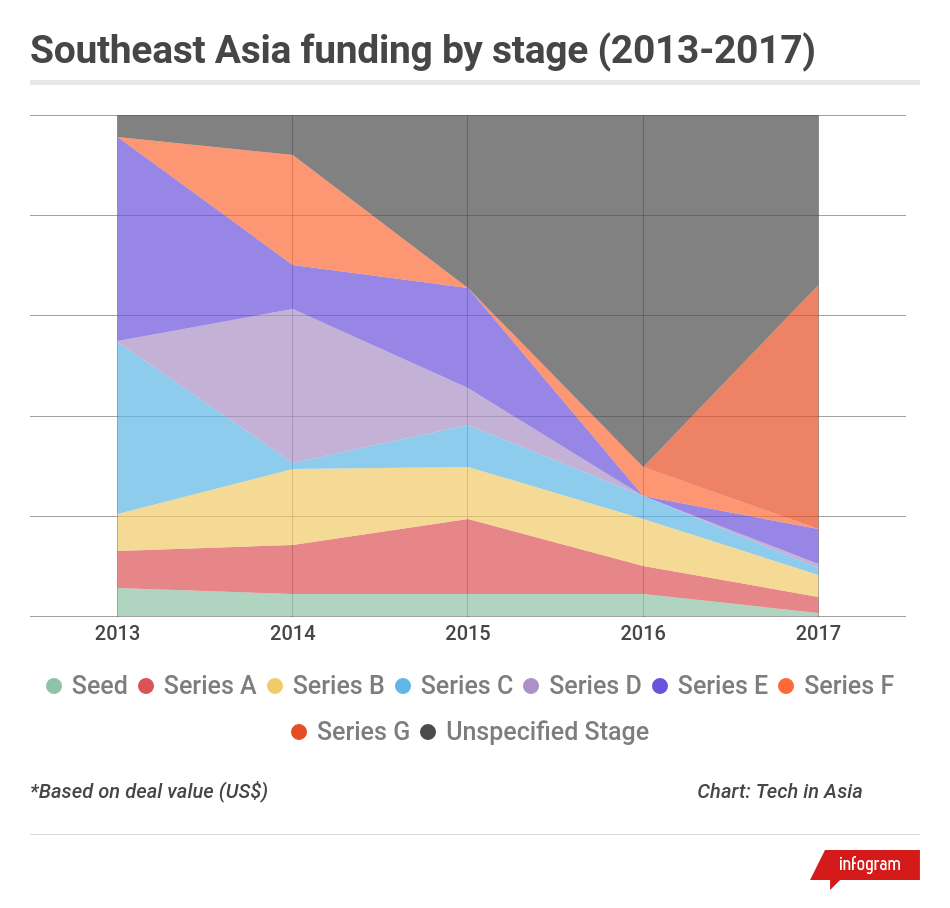

Similar to what we’ve seen in 2016, late-stage mega funding rounds accounted for bulk of the 2017 tally. Those deals involved the likes of ride-hailing firm Grab and consumer-to-consumer marketplace Tokopedia – which both raised their series G rounds, as well as publicly listed Sea, which raised its series Eprior to its initial public offering last year.

Large chunks of funding with unspecified stage were injected into the likes of Lazada, Traveloka, AirTrunk, and iflix.

Series B funding, where a gap was observed in the past years, went up.

Accordingly, seed and series A rounds appear to have peaked in 2015 and slowed down since – either in terms of deal value or volume.

“SEA is a relatively newer market, and we saw the same thing happen in China’s venture industry,” Pan-Asia VC Gobi Partners’ founding partner Thomas Tsao said in an interview with Tech in Asia. He said investors were keen to put money into early-stage startups in recent years, and those businesses that managed to survive were now looking for growth capital.

“If you look at the numbers for 2013 and 2014, there were so many seed and series A deals happening – whether that’s money coming from governments that increased entrepreneurship, or VCs. As those companies get to the next stage, you start seeing the B and C rounds getting done,” he explained. “It’s a natural function of time.”

It doesn’t necessarily mean that funding for the early stages has dried up. ICOs, otherwise known as coin or token offerings, have emerged as a new popular method to raise seed funding, Tsao noted.

CoinDesk’s ICO tracker shows that from January to late November 2017, nearly US$3.48 billion was raised through token sales globally. A previous report from Goldman Sachs said money from ICOs had surpassed early-stage VC funding in the first half of last year. In Southeast Asia, Tech in Asia’s data included only a handful of ICOs.

Addressing the ‘funding barbell’

The past years have witnessed a “funding barbell,” with money gravitating towards early stage deals or late, big-ticket rounds, giving the critical series B and C phases a miss, according to Tsao. Yet there’s no shortage of companies to invest in, he said. The issue is lack of institutional funding.

“It’s easier to start a US$5 million early-stage fund than raise a US$200 million growth fund […] there aren’t many funds with that mandate,” he argued.

Previously, Vickers Venture Partners co-founding partner Finian Tan expressed the same view. “There are a lot of early stage funds – US$30 million, US$50 million, US$80 million funds – that have recently sprouted,” he told Tech in Asia in October. “And then at the late stage you have strategics like Tencent, Alibaba, SoftBank Vision – the big boys, including private equity, coming in” to do transactions in the tens of millions of dollars. “When it comes to US$50 million to US$500 million funds – it’s empty.”

Both Tsao and Tan see a huge opportunity in filling the gap. That’s why Gobi just launched its Meranti ASEAN Growth Fund, which has so far raised US$50 million of its US$200 million target, while Vickers closed a new US$230 million fund that would target deals falling in the series A to C range.

“I think 2018 could be the year where more growth-stage funding happens,” Tsao said. Indeed, other VCs such as 500 Startups might also be looking to do more mid-stage deals.

‘All the big fish have been caught’

Tsao thinks late-stage funding could slow down this year “just because the big startups have all been funded.”

He said the startup ecosystem would probably have to wait two to three years to see other companies close the same deal sizes made by the likes of Grab. “We need a whole new generation of companies to get to that scale.”

That’s why growth stage funding will be crucial. “The pond needs to be replenished. All the big fish have been caught, we need a new generation,” he stated.

As for seed and series A investments, new funds were also launched in the region last year, among them:

- Vertex Ventures’ $210 million fund

- Kejora’s US$80 million fund

- Former Sequoia partner Yinglan Tan’s $25m debut fund

- East Ventures’ US$28 million fund

For startups in those stages, valuations might get pushed up with too much capital chasing few good deals, Tsao concluded.