Open Banking: Open for Business or Closed to Progress?

By Pau Velando – Strands

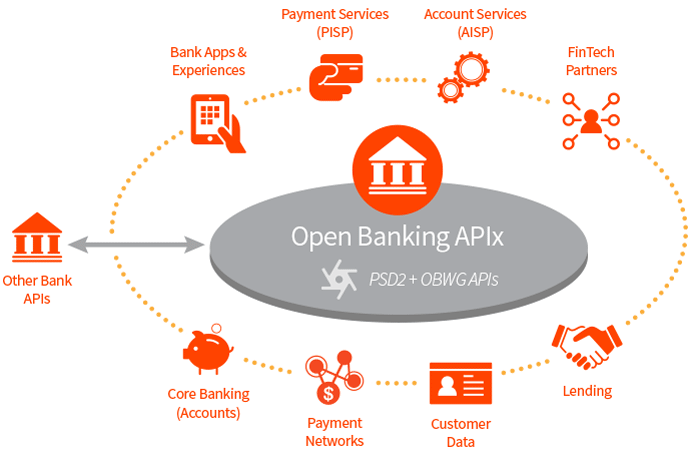

The future of banking is indisputably Open Banking. Open in all senses of the word: transparency, ease of access to information and a place at the table for new market players.

Open for everyone, without exception.

A straightforward concept in theory, with several underlying practical complexities:

The first: the overall playing field. With the term ‘open’ also comes increased competition and the need for all affected parties to up the ante. Competition in this new setting doesn’t come solely from banks, so the implication is that smaller, considerably more analogue banks are being pitted against inherently digital companies the likes of Facebook, Twitter and Weibo who have a head-start in terms of following –their user base figures are in the millions -, advanced customer insight and vastly superior technology.

Many banks are still reluctant to relinquish their tight grip on their customers’ data,

forced to step outside their comfort zone, never to return. The reality is that no one bank holds all the coveted information anyway; transactional data for the average customer spans more than 1 bank account, PayPal and often even pre-paid cards, so banks are only working with a third of the bigger picture at best.

Many banks are still reluctant to relinquish their tight grip on their customers’ data,

forced to step outside their comfort zone, never to return. The reality is that no one bank holds all the coveted information anyway; transactional data for the average customer spans more than 1 bank account, PayPal and often even pre-paid cards, so banks are only working with a third of the bigger picture at best.

Intelligent Banking, A Smart Move

Intelligent banking is redefining the banking sector, and indeed what it means to be a bank at all. Customers have become so used to convenient, real-time applications and solutions, that the reality for banks is that services must be quick, mobile, personalised and more importantly, relevant, to secure their future.

Internet giants are forging their own path, unfazed by the bank and their antiquated business models, yet banks must begin on their own quest for new revenue streams, value-added services, keeping the big guy firmly in their rear-view mirror as they push for takeover.

Times have changed and for those who have waited until now to catch up, there’s a way to go. Customers are mobile, expect convenience and apps that are powerful, intelligent and predictive. They dictate the who, the how and the why – the what is open territory and anyone’s game.