Should Startups Care About Profitability?

By Mark Suster from Upfront Ventures

There are certain topics that even some of the smartest people I talk with who aren’t startup oriented can’t fully grok. One of them is whether profitability matters.

It’s common cocktail party chatter to hear people confidently pronounce that some well known startup is sure to blow up because, “How could they succeed when they’re not even profitable!”

Or you know the other one — the one where Snapchat lost $2 billion in just one quarter. Two-fucking-billion! What a disaster! Except that they didn’t actually lose $2 billion in cash. It was a stock option incentive related “expense” but I bet you didn’t know that because in an era where we only read the headlines — they must be a train wreck losing billions. (They actually lost about $175 million in cash in that quarter, FWIW. See appendix if you want to know more on this.)

In any tech startup there is a healthy tension between profits & growth. To grow faster businesses need resources today to fund growth that may not come for 6 months to a year. The most obvious way to explain this is with sales people.

If you hire 6 senior sales reps in January at $120,000 / year salary then you’ve taken on an extra $60,000 per month in costs yet these sales people might not close new business for 6 months. Your profitability will go down for 2 quarters while your growth may increase dramatically in quarters 3–12.

I know this seems obvious but I promise you that even smart people forget this when talking about profitability. 70–80% of the costs of most startups are employee costs so what you’re really talking about when a company is unprofitable is that they are growing their staff ahead of their revenue.

If you don’t have a strong balance sheet and can’t hire more people that’s fine — but understand this may lead to slower growth. Thus the trade off between profits & growth.

I often ask entrepreneurs to consider, “What’s your objective? Are you looking to potentially sell the company in the next year or two? Do you plan to run this as a smaller business but maintain healthy profits? Do you imagine eventually raising VC and trying to build a faster growing company?”

Venture capital isn’t right for many business but if you do want to raise from a VC at some point you need to understand that often investors care more about growth than profits. They don’t want high burn rates but they will never fund slow growth.

Revenue

When I look at an income statement I start by focusing on the revenue line. I want to understand how many units the company is selling, whether this is increasing over time and how well they’re doing at retaining the customers that they do acquire. My first priority is to understand “growth drivers.”

If you had two companies each with $10 million in revenue today they might have vastly different prospects for the future. One company might be growing its revenue at 50% per year and the other might be growing at 5% per year.

Of course when you think about it it’s kind of obvious but when people make snap judgments about information they hear about companies or read about in the press they often don’t take the time to start to consider the details.

The Nature of Revenue Matters

Of course revenue alone won’t tell you enough. You need to understand the “quality” of the revenue.

- Is it one product line or multiple?

- Do 20% of the customers make 80% of the revenue or do the top 3 customers represent 80% of the revenue. (This is called “revenue concentration” and the more concentrated your revenue the higher the risk that your revenue could decline in the future.

- Is the revenue dependent on a concentrated set of distribution partners or platforms that put future revenue at risk?

- etc

Revenue is Not Revenue is Not Revenue

It’s also not as simple as just looking at revenue growth in dollar terms. For example, look at the following graph. You’ll notice that although both companies have the same revenue every year, Company 1 has much higher gross margins than Company 2 because the cost of sales (COGS) is much lower.

“COGS” represents the amount that each sale costs you. For example, if you sell your product through a third-party reseller who charges 30% of any sale then your COGS will be 30% of revenue (assuming no other costs of sales).

The example chart is not actually atypical. The first company represents a normal software company that sells its products directly (either via sales staff or directly off of the internet). Many software companies have 85–90% gross margins, which is why it has historically been a very attractive industry.

Company 2 might represent an “ad mediation company” where the company gets paid by ad networks for running ads on publisher websites and the company in turn must pay the publisher 85% of the revenue it collects. This is not atypical for “middle men” who often take 15–30% of the value of the sale

If you’re shaking your head and thinking, “duh” I promise you that even some of the most sophisticated people I know get off track on this issue of “gross revenue” versus “net revenue.”

We get the revenue argument, but shouldn’t all companies want to be profitable?

Not necessarily.

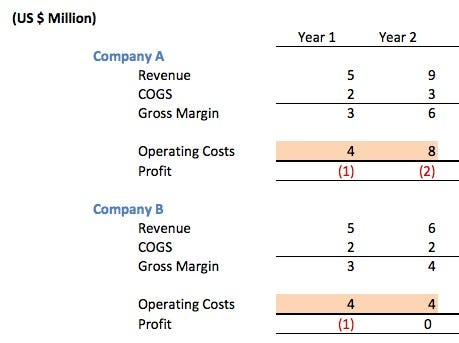

Let’s consider the following two competing software companies, both of which have 66% gross margins and they decide to run their company exactly the same in year one.

They both raised angel / seed money of $1.5 million to fund operations in their first year of operations. Both companies lost $1 million in their first year and thus finished the year with $500,000 in the bank. Company A lost $2 million in Year 2 while Company B broke even.

So which company is better run?

The answer is that you have no way of knowing. On quick glance a person might lament the fact that Company A is “not profitable” or is being a typical Internet startup. After all, they doubled their operating costs when they weren’t even profitable.

What did they actually do? They raised $5 million in venture capital to fund growth. They used the money to hire a bigger tech team so they could roll out their second product line. They hired a marketing team to promote their products more broadly.

They hired a biz dev team to work on deals where their product could be embedded in other people’s products as a way to increase customer demand. They got a bigger office space so their employees would feel comfortable and they could improve employee retention.

If there was strong market demand for their product then this investment might pay off handsomely.

I also wouldn’t be so quick to say that Company B is run worse than Company A. That management team might have decided that they wanted to maintain more control of their company, didn’t want new board members and didn’t want to take dilution.

The answer may not be known for many years. If the market they are targeting is very large and fast growing then the venture-backed businesses often make it harder for the non-venture-backed businesses to compete in the long-term. If the markets aren’t large then the company who managed its costs may be able to get a modest exit at a fair price and make the team wealthy precisely because they didn’t take on venture capital. The VC-backed businesses sometimes “blow up.”

As is often the case — there are no obvious or right answers.

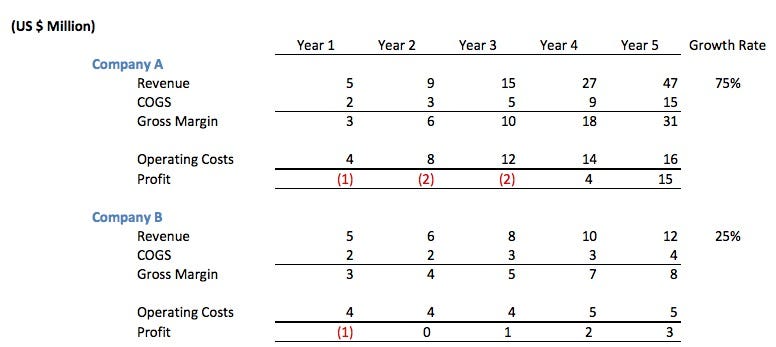

Let’s look at years 3–5 of these two companies.

In this scenario even though Company B initially looked prudent, it turns out that the investment that Company A made in people led to a higher annual growth rate. At the end of year 5 Company A had earned $19 million in cumulative profits (gains — investment years) while Company B had made only $6 million.

You could actually argue that both companies may have good futures and often this is true. But in other cases Company A uses its growth rate to attract more capital, innovate more on its products, do more marketing, capture more customers, lure away employees and often drive down profits for its competitors over time.

This is precisely why large Internet categories often produce “winner takes most” outcomes.

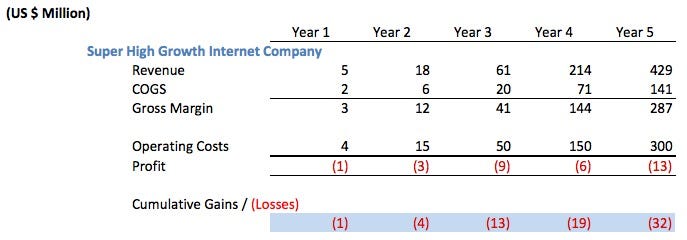

So let’s consider an even more aggressive “super high growth” Internet company. You know, the kind that unknowing commentators would be quick to lambaste as being wasteful because they’re not profitable.

The company would have had to raise at least $35 million in venture capital to have funded operations like this. More likely they raised $50 million or more.

Crazy? Stupid? Should they have slowed down operating costs in order to “make a profit.”

Again, it depends. If the growth is as spectacular as it is here and if they have access to cheap capital then they’d be crazy not to have raised VC money. Most likely after year 4 they began filing for their IPO to go public and journalists would be lining up to write stories in year 5 about how “they had never turned a profit in their 5 years of operations” and how “they were going public but still losing money.”

This is the trade-off between profits & growth!

The next time somebody wants to slam Amazon for not being more profitable please explain this. Amazon is continuing to grow at such a rapid pace that of course it should take some of today’s profits and reinvest them in growth (or acquisitions).

If there is a company that can’t grow fast enough then they should do other things with their profits, like return it to shareholders.

Appendix:

Early I discussed why stock option incentive expenses are not really cash losses and how people often misunderstand this leading to people proclaiming that Snap lost $2 billion! when they didn’t actually lose that in cash.

I don’t want to pretend that stock-option grants have zero impact on you as a shareholder. Stock option grants dilute your ownership in the company. They work a little bit like inflation. Inflation doesn’t “feel” like you’re losing value because if you have $10,000 in the bank you still have $10,000 after a year of 20% inflation but it actually buys you less when you want to spend it. Stock-option incentives are similar in that they dilute your ownership but you still own the same number of shares. It may impact you in ways you don’t understand because the institutions who drive the price of your shares may push down the share price but you probably won’t understand the correlation.

Executives explain these incentives as necessary to motivate top talent to stay at the company, innovate and in turn drive the value in your stock and of course this is true to an extent. Like all things of course there is a trade-off between payout out rewards to owners and paying out rewards to management. In some public tech stocks the size of the payout to top executives — even when they don’t perform well and eventually get acquired — the payouts are ridiculous.

Photo credit: -Snugg- via Visual Hunt / CC BY-NC

First appeared at his blog