Leveraging Fintech to Achieve Financial Inclusion in Indonesia

by Ghiyazuddin Mohammad and John Owens (reposted from MicroSave’s blog)

“Fintech” – an intersection of financial services and technology – is taking the traditional financial world by storm. Indonesia is no exception, with a fast-evolving ecosystem that includes a host of financial services offered by new generation fintechs.

The diagram below, by no means exhaustive, highlights a few of the fintech players covering a myriad of financial services like payments, credit, savings, insurance, and financial management.

Indonesia – Perfectly Placed to Reap “Fintech”

Indonesia – Perfectly Placed to Reap “Fintech”

Indonesia is the fourth largest mobile market in the world with 339.9 million connections – a SIM penetration of 131%! 43% of Indonesians already own a smartphone. Furthermore, Indonesia is going “mobile-first” with 64.1 million out of a total of 88.1 million users accessing Internet through mobile devices. This is fuelling social media usage by platforms such as WhatsApp, Facebook, Blackberry, Line, Path, etc. This trend is also leading to explosive growth in electronic and mobile commerce, with big names such as Alibaba, Softbank, Sequoia, Rocket Internet, and Temasek backing local ventures. In contrast, only 36% of 250 million Indonesians have access to formal financial services.

Keeping these technological advancements in context, Indonesia is well placed to leverage “fintech” towards the cause of financial inclusion. Fintech innovations are providing a range of new opportunities to dramatically change four main financial service areas – payments, remittances, credit and deposit-taking.

Leveraging Savings

Without access to formal financial services, many poor Indonesians continue to utilise informal services such as Arisan (ROSCAs), package saving schemes, and savings with individual agents.1 The bank deposit-to-GDP ratio in Indonesia (an indicator of deposit mobilisation) stands at 34.55% – much lower than Malaysia (130.25%), Cambodia (42.97%), and the Philippines (54.38%). This presents a big opportunity to all financial service providers, but especially new fintech players.

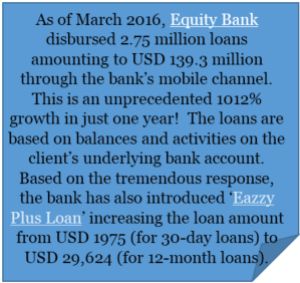

If we look at examples from other countries, Equity Bank in Kenya is one of the best examples of deposit mobilisation through digital banking services. After starting agency banking in 2011, the bank now mobilises 20%2 of its total deposits through a channel network of 25,388 agents, spread across the country. A dedicated team focusing on agency banking business and a client-centric business model based on the philosophy of “listening to customers” has made this possible. Other examples include, M-Pawa’s interest-bearing savings account in Tanzania, developed in collaboration between Vodacom and CBA and the Lock Savings Account offered to M-Shwari users in Kenya, where clients can move money from their M-Pesa account to save through a fixed deposit account that earns higher rates of interest.

Other examples include rural banks in the Philippines which were one of the first financial service providers to offer SMS reminders for commitment savings that allowed for dramatic increases in savings rates.3 This has been followed by new fintech players supporting banks to support increased savings behaviours in low-income customers such as Juntos. Similarly, there is also a significant potential to utilise SMS technology and/or messaging platforms to support goal-based savings in Indonesia. A case in point, is the common practice of saving to meet expenditures for major religious events like Ramadan.

Enabling Payments

A booming e-commerce sector, fuelled by large international investors, needs an intuitive online and offline payments infrastructure. However, a 2015 Bank Indonesia study documented that 89.7% of the transactions in Indonesia are in cash. This provides a tremendous opportunity. Consider the following payment process in order to make a purchase through a leading e-commerce portal for those with bank accounts:

Navigation through multiple websites makes the payment process clumsy, leading to poor user experience. In addition, most online portals limit payment options to those with bank accounts or provides cash-on-delivery options which are costly to operators. Using mobile/electronic wallets for payments, an option available for leading e-commerce portals such as Tokopedia and Elevania, can provide a more seamless experience to customers as well as reduced expenses for operators.

Further, offline payments through mobile/electronic wallets also present a significant use case. Kopokopo―a leading merchant aggregator in East Africa with more than 10,000 merchants―is a successful example of providing a mobile-based small value merchant payment platform. Apart from acquiring merchants, the organisation focuses on providing value-added services such as merchant cash advances, transaction analysis tools, and merchant/customer engagement initiatives to ensure merchants remain active. Easypaisa in Pakistan and PayTM in India are other notable examples for merchant payments. Closer home – players like TCash, Tapp Commerce and Dimo Pay are catching up fast. The idea is to integrate the payment and financial service habits of users through a single e-wallet/account. This could then be used for a variety of payments whether making purchases online, pay for Gojek/Uber, restaurant bills, or bill payments.

Easing Remittances

Remittances–both domestic and international–are a big market in Indonesia. However, most domestic remittances are largely informal and cash based. In a research conducted by Gallup, 50% of the Indonesians said that they sent money to their family or friends in the preceding 12 months, in “cash”. An average of US$ 87.40 is sent about 1.6 times a month! Evidently, a huge untapped market waiting to be facilitated via fintech players. This is especially relevant to mobile/e-money users where 71.5% of all transactions (by value) are person-to-person transfers.

Indonesia provides a US$10.5 billion international remittance market – an opportunity for new fintech players to add value to a market heavily dominated by money transfer operators such as Western Union. This is especially the case with remittance prices, averaging 5% to 8.60% of the amount sent.4 Notable fintech players in this segment such as WorldRemit have already partnered with Dompetku – a mobile money service offered by Indosat Ooredoo. However, there is a compelling need for focused players to cater to Indonesian migrant workers, predominantly based in Malaysia, Taiwan, Saudi Arabia, Hong Kong, Singapore, and the United States.

Access to Credit

The World Bank estimates that only 13.1% of the Indonesians have borrowed from a formal financial institution. Further, domestic credit to GDP ratio in Indonesia is 43.5%, lower than its neighbours including Malaysia (140.5%), Vietnam (113.8%), the Philippines (55.8%) and China (169.3%). Online, fintech-based lending can play a pivotal role in narrowing this credit gap. Micro and MSME loans based on alternate credit assessment models are growing across the developing world.

(55.8%) and China (169.3%). Online, fintech-based lending can play a pivotal role in narrowing this credit gap. Micro and MSME loans based on alternate credit assessment models are growing across the developing world.

Mshwari in Kenya offers small/instant loans in collaboration with Central Bank of Africa (CBA). Credit assessment is built on data generated on the basis of airtime usage, M-Pesa usage, length of association, etc. Tigo Tanzania (Tigo Nivushe), MTN Ghana (Mjara loans) and Equity Bank (Eazzy loan) are other examples of this model.

Given the market size in Indonesia, there is huge scope for growth. Following global cues, fintech credit players such as Uang Teman, Mekar, and Modalku have already emerged in Indonesia.

To read the entire article click here