Cashless society and Fintech hubs

The world dreams of a cashless society. And as it acquires a multitude of non-cash payment options, this dream only comes closer. The progress of economies varies, though. In Hong Kong, one can purchase tickets or eat in fast food outlets using the Octopus value card. In Sweden, the homeless no longer ask passers-by for loose change; they have card readers instead.

Read our full research “Money of the Future”. Download PDF (20MB)

While the cashless journeys of some may be advanced, those of most, especially developing nations like the Philippines, have only just begun.

If you had asked anyone in the region about fintech just a couple of years ago, you would have been met with blank stares – and not the eyes-glazing-over kind that some people get when someone mentions finance. Today, it’s the fancy, shiny sports car that just pulled up in the town square; it’s all everyone seems to be talking about, and they’re all wondering if they can hitch a ride.

US is still homeland of fintech. New York is rapidly growing as one of the world’s hubs of innovation. Some of the hottest fintech startups are represented in New York and new entrants can find endless opportunities in the global trading center. The New York fintech industry has companies working in a variety of sectors. Lending, marketplace, investment management and trading are denser than others, which create more opportunities for startups aiming to enter into sectors such as accounting, insurance and payments.

There are about 22 hottest fintech startups from Silicon Valley (and many smaller, for sure). 7 best fintech companies in Silicon Valley highlighted by 2015 Silicon Valley 100 list are Square, Lending Club, Stripe, Robinhood, 21 Inc., CoinBase and CardSpring.

In Global Startup Ecosystem Ranking Silicon Valley slips, while Southeast Asia gains traction. Singapore, for example, is the 10th best startup ecosystem in the world, and may be an alternative to Silicon Valley. There are some new fintech’s dark-horse cities like Singapore, Berlin, Madrid, Sydney and Amsterdam.

Also, for example, APAC is the best region for living in the Monocle Quality of Life Survey 2015: Tokyo (1), Melbourne (4), Sydney (5), Fukuoka (12), Singapore (13), Kyoto (14), Auckland (17), Hong Kong (19). (In the Mercer’s Quality of Living Rankings you can see other view: 26 – Singapore, 70 – Hong Kong, 72 – Seoul (South Korea), 98 – Chenoa (South Korea), 99 – Taichung (Taiwan), 142 – Chongqing (China), 142 – Xian (China). Moscow is rated 167th, Kiev -176th and Minsk – 189th.)

500 Startups, a leading global venture capital seed fund and startup accelerator from Silicon Valley managing $200M in assets and having invested in 1300+ technology startups, is launching a FinTech-exclusive batch comprised of eight companies starting from January 19, 2016. In May 2014, this California-based accelerator announced the launch of a bitcoin and fintech investor syndicate on AngelList. Founding partner of 500 Startups, Dave McClure, has a fintech background. Sheel Mohnot, General Partner at 500 Startups, leads fintech investments at 500 Startups.

Indeed, investment in fintech companies is growing faster in the U.K. than it is anywhere else in the world. Last year, London’s fintech startups attracted £343 million, triple the amount invested in the previous year, according to London & Partners, a firm set up by London Mayor Boris Johnson to promote the city. U.K. fintech companies raised £306 million in the first half of 2015 alone.

London is known to be one of the world’s hubs of innovation with a wide range of well-known disruptive startups coming from the UK’s disruption center. Along with Silicon Valley and New York, London is a place of tremendous opportunities for bright entrepreneurs. In last five years, out of $9.8 billion of investments in fintech across the European region, 55% are invested in UK fintech.

London is one of the most advanced cities when it comes to innovation adoption. Elimination of tickets and contactless payments adoption rates are speaking in favor of it. Transport for London (TfL) passengers can travel using contactless payment cards across the Underground and most of the other London transport. Nearly 50% of London’s population already has contactless debit or credit cards which can conduct transactions under £20 without the need for a PIN number or a signature. Contactless payments have been in use in London buses since December 2012. There are currently about 70,000 contactless payments being made on buses in a day.

London is one of the most advanced cities when it comes to innovation adoption. Elimination of tickets and contactless payments adoption rates are speaking in favor of it. Transport for London (TfL) passengers can travel using contactless payment cards across the Underground and most of the other London transport. Nearly 50% of London’s population already has contactless debit or credit cards which can conduct transactions under £20 without the need for a PIN number or a signature. Contactless payments have been in use in London buses since December 2012. There are currently about 70,000 contactless payments being made on buses in a day.

London is also the city where an 800-year-old tradition was broken two years ago. December 2013 saw the breaking of an 800-year-old tradition of cash-only payments at Covent Garden’s arts and craft market in central London. Stallholders at the venue were fitted with PayPal’s mPOS card readers which enabled them to accept credit and debit card payments over the Christmas shopping period. Over 8 million shoppers turned up for the event.

The year 2015 was a successful one for London fintech as some of the most promising fintech startups raised significant funds. Funding Circle secured the highest deal among other fintech companies by scoring $150 million in funding. WorldRemit and TransferWise followed with $100 million and $58 million respectively.

European fintech ecosystem consist not only from UK startups. Behind London and Berlin, the Dutch startup scene is already considered to be one of the most prominent in Europe. If it feels unfair to weigh an entire country against individual cities, consider that the Netherlands has 17 million people crammed into an area half the size of South Carolina. Startup Juncture reported 75 major deals in 2014, for a total of roughly $560 million in investment. Ten companies raised over $9 million.

Denmark‘s government is planning to help usher in the long-awaited cashless society by giving restaurants, gas stations and some shops the option to refuse notes and coins.

France launched French Tech Ticket, a startup visa for foreign entrepreneurs. Also France creates National FinTech Program to rival London and New York. Not wanting to be left behind in the global fintech engineering race, corporate leaders from around France have banded together to create the France FinTech association. In the same time the government trying to attract new startups arrested CEO of one of the biggest – Uber. Right reaction could be: Boris Johnson, major of London, defends telling black cabbie to “fuck off and die” saying the irate driver had heckled him first in row over Uber app.

Switzerland is one of the European’s major financial hubs, which creates tremendous opportunities for the development of fintech innovation. Fintech Fusion are calling for applications for their 2015 class, which will be their first. Sébastien Flury, the incubator’s program director, believes that banks have to ‘”reinvent themselves” and they have started to recognize this fact. Also SwissFinanceStartups.com – a new Swiss government fund to support fintech-startups has been launched.

Competitor of Paris – Stockholm – is staking a claim as a major European fintech hub after recording $266 million in startup investments over the past year, leaving it trailing only London as a magnet for VC inflows. While the Swedish capital lacks an extensive financial ecosystem of accelerators, incubators, and niche investors compared to other European financial centres, it nonetheless accounted for 18.3% of all fintech investments in Europe over the past five years, according to figures from the Stockholm School of Economics.

With Sweden staking a claim as a fintech hotspot, Stockholm-headquartered Nordea has moved to grab a slice of the action by setting up an accelerator programme with Finnish innovation agency Nestholma to nurture small businesses developing digital banking services across the Nordics.

Banks are ripping out ATMs. Even panhandlers accept credit cards. The end of cash in Sweden brings many benefits—and a few concerns. Several major banks in Sweden no longer carry cash, and if you want to buy a candy bar at the corner store, you pull out your phone. Even homeless people selling newspapers on the street take credit cards. By the end of last year, four out of every five transactions in the country were cashless. And new research has found that the amount of money in circulation has dropped around 40% to 50% over the last six years.

Banks are ripping out ATMs. Even panhandlers accept credit cards. The end of cash in Sweden brings many benefits—and a few concerns. Several major banks in Sweden no longer carry cash, and if you want to buy a candy bar at the corner store, you pull out your phone. Even homeless people selling newspapers on the street take credit cards. By the end of last year, four out of every five transactions in the country were cashless. And new research has found that the amount of money in circulation has dropped around 40% to 50% over the last six years.

Sweden has a history of being quick to adopt financial innovations. The country installed its first ATM machine in 1967, two years before the U.S. Now they’re ripping the machines out (between 2010 and 2012, banks removed around 900 ATMs). The move to digitize everything has been happening for awhile—Sweden was also early to adopt direct deposits and paying with plastic. By this century, unions started pushing to get rid of cash as a way to protect workers like bus drivers from robberies—if you get on a bus now, you can’t pay with paper money.

“There is also a demographic development behind this,” says Niklas Arvidsson, a professor at Sweden’s Royal Institute of Technology who studies the transition away from cash.

“Younger people do not start using cash but instead move directly into new services, while older people—who are the most frequent users of cash—reduce their spending as they get older and older.”

Of course, even in hyper-connected Sweden, not everyone has a smartphone or a debit card. “The main challenges is to create a payment service system that allows everyone in a society to make a payment and to receive money in a convenient way,” Arvidsson says.

“There are people without bank accounts, mobile phone subscriptions and access to Internet, and there must be solutions also for them. Cash is a good solution for this group and there must be solutions also in a cashless society.”

The country won’t become 100% cash-free immediately—the country’s central bank would have to change the law and say that cash is no longer legal tender. “This is not likely to happen before 2030,” says Arvidsson. ”

There are no indication that politicians are considering that move. The introduction of new Swedish bills and coins, which is happening now, actually points to the conclusion that the central bank and politicians plans for the possibility that cash will be around until at least 2040. Then there will be a need for a decision that either says that we should introduce new bills and coins or to make the step into a 100% cashless society.” Still, the country may get close to eliminating cash much sooner and could be practically cashless in 8 to 10 years.

In Asia alone, at least 5 cities – Singapore, Hong Kong, Sydney, Shanghai, Tokyo and more – can claim for various reasons to be the region’s fintech hub. To be the landing and resting place for the world’s best fintech ideas to access Asia and the rest of the world. Some of these cities have terrific infrastructure – government and industry support in Singapore, huge and close market access in Shanghai, active and involved banking industry in Sydney – others have an active startup scene – vibrant entrepreneurial activity in Jakarta; financial know-how and capital to invest in Hong Kong; creative ideas, technologies and brands in Tokyo and Seoul.

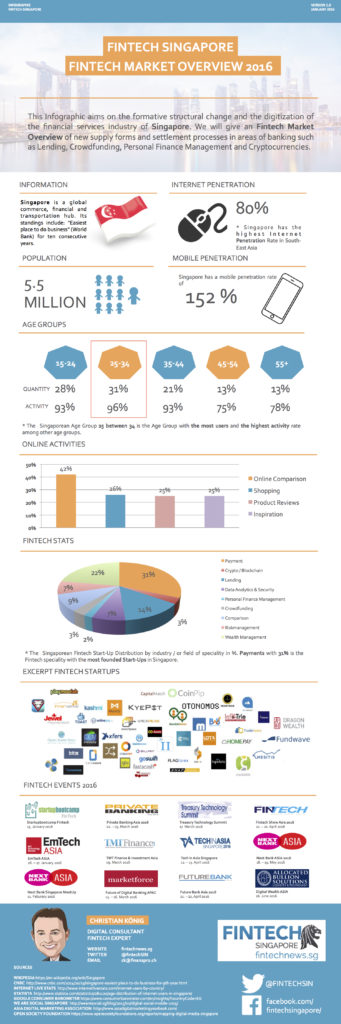

It’s an exciting time for Southeast Asia-based startups and there is no doubt that Singapore sits at the epicentre of a diverse range of markets rich with opportunity. New success stories are emerging throughout the region, such as GrabTaxi, which is experiencing explosive growth and attracting substantial investment. Singapore is one of the gateways of the Asian financial market with a rich fintech ecosystem. Global financial services companies have their Asian satellites operating from Singapore. AmEx, Citibank, JP Morgan Chase, HSBC and numerous other international financial organizations operate in Singapore.

It’s an exciting time for Southeast Asia-based startups and there is no doubt that Singapore sits at the epicentre of a diverse range of markets rich with opportunity. New success stories are emerging throughout the region, such as GrabTaxi, which is experiencing explosive growth and attracting substantial investment. Singapore is one of the gateways of the Asian financial market with a rich fintech ecosystem. Global financial services companies have their Asian satellites operating from Singapore. AmEx, Citibank, JP Morgan Chase, HSBC and numerous other international financial organizations operate in Singapore.

Compared by the index for financial center rating, in which a multitude of factors are integrated, Singapore and Hong Kong represent the most attractive spots in the region to enter the financial industry. Important areas of competitiveness are, among others, business environment, human capital, taxation and infrastructure. As demonstrated by the chart, Singapore and Hong Kong are the leading financial centers in Asia-Pacific region.

Speaking of the financial industry, there are around 200 banks with total assets of $2 trillion with operational headquarters in Singapore. IT procurement budgets of those banks reached $485 billion last year, according to the Asian business magazine Nikkei Asian Review. With global trends towards tight collaboration among traditional financial institutions and fintech ecosystem, Singaporean financial services providers also made a step forward nurturing incubation and fintech ecosystem development. Global banking giants are building an innovation conveyor to ensure a leading position as a global financial market.

Some of the examples are UBS, DBS Bank and Citigroup, which launched their innovation labs in Singapore. In 2012, MasterCard launched an R&D innovation center in Singapore to enhance research and development through MasterCard Labs, Technologies Operations and a Chip Centre of Excellence (CCoE), covering the full range of upstream research, hardware and software solution development. The CCoE in Singapore was crucial for MasterCard to leverage the benefit of skilled engineers, access to latest innovation and the ability to service the rapid growth in Asia-Pacific, the Middle East and Africa.

A variety of fintech startups across sectors are building the Singaporean fintech ecosystem. Among them are: Numoni (online-bank for unbanked), M-DAQ (cross-border securities), Quoine Exchange (bitcoin exchange), ApexPeak (a nonbank capital provider offering early payments on receivables), BillPay (a free unified billing and payment service), Call Levels (real-time alert notification on current market prices in forex, commodities, equities and indices), Capital Match (provides short-term financing to SMEs), CoAssets (a business network for property investment and equity crowdfunding enthusiasts), CoinHako (a cryptocurrency wallet), CoinPip (uses blockchain technology to send money internationally quickly and easily to freelancers), Dragon Wealth (the world’s first app to enable investors to compare their portfolios across managers, portfolios, countries, and with other investors, giving investors greater control over their investments), SoftPay (mPOS), Mobikon (POS-management), MatchMove (bank-as-service), Fastacash (social based remittances) and many others.

Singapore remains one of the hubs for fintech activity – business-friendly regulations mean founders eye the city-state as a base from which to expand to the rest of Asia.

The Prime Minister of Singapore has urged the country’s banks and regulators to keep up to scratch with technological developments such as blockchain technology. Speaking at the United Overseas Bank 80th anniversary dinner held in Singapore yesterday, Prime Minister Lee noted the challenges currently facing the financial industry and highlighted the importance of keeping abreast with technological developments in order to remain competitive.

MAS created FinTech & Innovation Group in August 2015. The new group in the Monetary Authority of Singapore will be responsible for regulatory policies and development strategies to facilitate the use of tech to better manage risks, enhance efficiency and strengthen competitiveness. The Monetary Authority of Singapore (MAS) has poached Citi exec Sopnendu Mohanty to head up a new fintech and innovation group.

The Monetary Authority of Singapore wants to cultivate this growth as part of its Smart Financial Centre initiative. $225 million has been recently invested into fintech by the MAS. As Singapore pushes on to be a Smart Nation, it is important that industries keep ahead of the curve. This is especially true for the finance industry, where new technologies are challenging the way business is being done. Embracing new technology is also important for Singapore to maintain its status as a regional financial hub, and MAS recognises that Singapore needs to be a Smart Financial Centre. Said Mr Thomas Zink, a research manager at IDC Financial Insights:

“It will strengthen its position, it will create new jobs and it will grow their expertise in the market. For start-ups, it also makes a lot of sense because of the ease of doing business in Singapore as well as the access to a lot of financial institutions that are headquartered here as well as Singapore’s geographic location at the heart of ASEAN.”

“Lastly for financial institutions, it will make sense to have access to new ideas, new businesses, new concepts that will help them to transform their business in light of the digital change we’re going through.”

“MAS will most likely follow through with the approach that (MAS managing director) Ravi Menon pointed out – that we are very supportive of banks partnering with fintech but it’s ultimately the responsibility of banks to make sure that everything is in order, they are compliant, they assess the risk properly that comes from such a solution,” said Mr Zink.

Between HSBC’s annual Expat Explorer survey Singapore ranked the first. Last year’s number one, Switzerland, dropped to 10, India jumped way back from nine to 17, and new countries entered the top 20 ranking. Ranking second in economics and third in both experience and family, Singapore is the most desirable place for expats.

“One of the cleanest and safest cities in the world, Singapore is a multicultural hub that’s worked hard to earn its place among the thriving Asian Tiger economies,” HSBC declares. The country is ranked first in school quality. In fact, in 2012, British education minister Michael Gove suggested that Britain adopt a similar system to Singapore’s. But to make it in Singapore, you have to be career-driven; the country scored extremely low for work-life balance. And while 65% have more disposable income, Singapore is one of the most expensive cities. In the next 2-3 years Singapore may become an international fintech hub.

Australia may well be known for its cuddly koalas and lethal spiders, but beyond these tourism-fuelled images lies a country, which is quickly proving to be an attractive nesting ground for SEA-based tech startups. At just over seven hours’ flight from Singapore to Sydney, it’s also the perfect amount of time to clear your inbox and get a few of those documents finalised that you’ve had to keep pushing to the side. Scoot’s cheap flights have helped to make the two markets all the more accessible and they even have Wi-Fi on the plane!

Australia may well be known for its cuddly koalas and lethal spiders, but beyond these tourism-fuelled images lies a country, which is quickly proving to be an attractive nesting ground for SEA-based tech startups. At just over seven hours’ flight from Singapore to Sydney, it’s also the perfect amount of time to clear your inbox and get a few of those documents finalised that you’ve had to keep pushing to the side. Scoot’s cheap flights have helped to make the two markets all the more accessible and they even have Wi-Fi on the plane!

While Australia is relatively small by population — it is a large market by potential revenue. Australia has a stable, prosperous economy with a regulatory environment favourable to innovation and competition. The local startup community in Australia at the moment is white-hot. If you consider the current economic climate in Australia, there is a high-level concentration of legacy industries and structural issues within key market sectors such as banking, aviation and transport. It also means that these industries are ripe for disruption.

With increased competition, disruption is everywhere and Asia-based investors are beginning to see the opportunity in the Australian market. An example is Softbank’s US$50 million investment in BigCommerce, a Sydney based e-commerce platform provider that has achieved impressive traction in markets beyond Australia’s shores. Australian fintech ecosystem is also very fast growing.

We’ve also seen increasing examples of SEA-based technology companies, such as Patrick Grove’s listing of iProperty Group, iCar Asia and Ensogo listing on the Australian Stock Exchange (ASX) and accessing one of the largest pools of investment funding in the region, fuelled by Australia’s compulsory retirement savings scheme.

There has never been a better time to invest in the Australian market or expand a business into this market. The Australian Securities Exchange has made things a little easier. The rules for listing on the ASX aren’t as stringent as they are in other stock exchange operators in the region. In Australia, companies don’t have to float a minimum percentage of stock in order to list, while Hong Kong has a minimum of 25 per cent and Singapore ranges from 12-25 per cent. Listing on the ASX is often a more appealing option, given its favourable listing requirements for early-stage companies. If you need a cash injection – consider going public on ASX (it is much easier than on NASDAQ) like AHAlife.

Furthermore, with Australian resource companies in a downturn, there is a developing trend of tech startups undertaking reverse takeovers into mining shell companies. Given backdoor listings are considerably less prescriptive than IPOs, Asian early-stage companies can follow the path of Singapore-based mobile social network MigMe to get to an ASX listing faster, cheaper, and with fewer investors. Ten years ago, high tech observers complained that China didn’t have enough bold innovators. There were, of course, wildly profitable high tech firms, but they rarely took creative risks and mostly just mimicked Silicon Valley: Baidu was a replica of Google, Tencent a copy of Yahoo, JD a version of Amazon. Young Chinese coders had programming chops that were second to none, but they lacked the drive of a Mark Zuckerberg or Steve Jobs.

Ten years ago, high tech observers complained that China didn’t have enough bold innovators. There were, of course, wildly profitable high tech firms, but they rarely took creative risks and mostly just mimicked Silicon Valley: Baidu was a replica of Google, Tencent a copy of Yahoo, JD a version of Amazon. Young Chinese coders had programming chops that were second to none, but they lacked the drive of a Mark Zuckerberg or Steve Jobs.

The West Coast mantra—fail fast, fail often, the better to find a hit product—seemed alien, even dangerous, to youths schooled in an educational system that focused on rote memorization and punished mistakes. Graduates craved jobs at big, solid firms. The goal was stability: Urban China had only recently emerged from decades of poverty, and much of the countryside was still waiting its turn to do so. Better to keep your head down and stay safe.

That attitude is vanishing now. It’s been swept aside by a surge in prosperity, bringing with it a new level of confidence and boldness in the country’s young urban techies. In 2000, barely 4 percent of China was middle-class—meaning with an income ranging from $9,000 to $34,000—but by 2012 fully two-thirds had climbed into that bracket. In the same time frame, higher education soared sevenfold: 7 million graduated college in 2015.

The result is a generation both creative and comfortable with risk-taking. Now major cities are crowded with ambitious inventors and entrepreneurs, flocking into software accelerators and hackerspaces. They no longer want jobs at Google or Apple; like their counterparts in San Francisco, they want to build the next Google or Apple.

Anyone with a promising idea and some experience can find money. Venture capitalists pumped a record $15.5 billion into Chinese startups in 2014 (US venture capital pool was $48 billion), so entrepreneurs are being showered in funding, as well as crucial advice and mentoring from millionaire angels. Even the Chinese government—which has a wary attitude toward online expression and runs a vast digital censorship apparatus—has launched a $6.5 billion fund for startups. With the economy’s growth slowing after two decades of breakneck expansion, the party is worriedly seeking new sources of good jobs. Tech fits the bill.

The new boom encompasses both online services and the hardware arena. Homegrown firms have distinct advantages, namely familiarity with local tastes, the ability to plug into a first-class manufacturing system built for Western companies, and proximity to the world’s fastest-growing markets in India and Southeast Asia. The combination of factors is putting them in a position to beat the West at its own game.

The success of copycat firms paved the way for “little dragons”—creative, upstart Web 2.0 firms that emerged in the late ’00s. The big dragons provided role models, but even more significantly, they built the infrastructure crucial for today’s high tech boom, including the cloud services that allow any twentysomething to launch a business overnight and immediately start billing customers.

Corruption is just one of the many challenges China faces. The country’s leaders and investors also contend with nontransparent banks, government regulators on the take, rampant pollution, fierce crackdowns on political speech, and a rural population yearning for better jobs in the cities. It’s not clear whether the party can solve all these messy problems.

The high tech gold rush has produced manic and fierce competition among the swarms of entrepreneurs. There’s also been a hackerspace movement in China. The first one—Shanghai’s XinCheJian—was cofounded in 2010 by Chinese Internet entrepreneur David Li, when he noticed how cheap prototyping tools were allowing kitchen-table inventors to produce increasingly slick prototypes. Western entrepreneurs now flock to hardware and software accelerators in China’s coastal cities. China’s creative generation, in other words, has proven it is ready to compete head-on with the world’s top high tech brands. Moreover, China’s digital banking customers are expected to triple by 2020, reaching 900 million. China is the largest worldwide crowdfunding market with a potential of $47 billion.

Alibaba and its two giant Chinese Internet rivals–search engine Baidu and gaming/messaging firm Tencent–a trio known as BAT, are pouring money into all manner of firms at every stage from seed to late rounds. Since 2012 we count more than 50 investments totaling $2.3 billion. In the past 18 months alone Alibaba has plowed more than $1 billion into just ten U.S. firms.

The three BAT companies each monopolize a sphere of China’s desktop-style online behavior, but they risk falling behind in mobile. This is a problem in a country where tens of millions of people skip PCs entirely. (China as itself has almost 1.3 billion mobile users, and half of them are on 3G or 4G.) Hence the landgrab–the Big Three don’t much care where the innovations on this new intertwined platform come from or, it seems, how much they have to shell out to secure them. The bulk of Alibaba’s revenue still comes from China, but the e-commerce giant will focus aggressively on growing its global business this year.

Daniel Zhang, who took over as chief executive officer last week, told employees in in a recent speech that not only will Alibaba pour money into its global businesses, but also transform its company culture. “We need to have global talent.“

The Shanghai Stock Exchange is on track to inaugurate a new market for small, innovative companies, which will challenge the wildly successful Nasdaq-style startup board in Shenzhen. New market to host firms in sectors favored by Beijing for building an innovation-driven economy.

Hong Kong is known to be one of the world’s major financial centers with a wide range of international financial industry giants having their Asian hubs in the city. Barclays, HSBC, Lloyds Bank, RBS, BBVA, UBS, Citi and Wells Fargo represent almost an endless list of international banks that have chosen Hong Kong as an Asian satellite location. It’s no surprise that some of the largest banks are represented in Hong Kong since it is the leading financial center in the Asia-Pacific region. Moreover, according to BI, Hong Kong is leading the fintech adoption market as 29% of the digitally active people in Hong Kong reported that they have used at least two fintech services in the last month.

Hong Kong is known to be one of the world’s major financial centers with a wide range of international financial industry giants having their Asian hubs in the city. Barclays, HSBC, Lloyds Bank, RBS, BBVA, UBS, Citi and Wells Fargo represent almost an endless list of international banks that have chosen Hong Kong as an Asian satellite location. It’s no surprise that some of the largest banks are represented in Hong Kong since it is the leading financial center in the Asia-Pacific region. Moreover, according to BI, Hong Kong is leading the fintech adoption market as 29% of the digitally active people in Hong Kong reported that they have used at least two fintech services in the last month.

Hong Kong’s Financial Secretary (the counterpart of our Finance Minister) John C Tsang in his budget speech announced a strong focus on financial sector development (80% of Hong Kong’s GDP) and support of fintech startups (paragraphs 38-48) . The regular InvestHK’s newsletter also covered this news, as well as the expansion of the government fund Stratmeup HK to India. Bloomberg has made a list of the best countries for startups, where Hong Kong was the first and Singapore ranked as 4th.

According to HK FinTech, in 2013, over $3 billion of investments in fintech have been made worldwide and this is set to triple by 2018. In fact, within APAC, fintech provides one of the most cost-effective methods of delivering banking services to the 1.2 billion people without a formal bank account. Global Financial Centers Index of 2014 placed Hong Kong among the world’s “big four”—New York, London, Hong Kong and Singapore.

According to Hong Kong’s official government website, at the end of April 2015, there were 157 licensed banks (LB), 23 restricted license banks (RLB) and 21 deposit-taking companies (DTC) in Hong Kong, together with 64 local representative offices of overseas banking institutions in the banking sector. These institutions come from 36 countries and include 71 of the world’s largest 100 banks. The daily turnover in the Hong Kong interbank market averaged $31 billion in February 2015.

Hong Kong’s stock market was the fifth-largest in the world and the third-largest in Asia in terms of market capitalization as at the end of April 2015. Hong Kong was also one of the most active markets for raising initial public offering (IPO) funds; $29.8 billion were raised in 2014.

Hong Kong fintech is a rich and rapidly evolving ecosystem with very promising fintech startups striving to compete in the international arena. The Government is committed to transforming Hong Kong into a hub for innovation and entrepreneurship. This was the message from Secretary for Commerce & Economic Development Gregory So speaking at a symposium in Chicago yesterday. He said Hong Kong strives to provide a vibrant ecosystem for innovation and technology to grow, and creates an enabling environment to help startups and tech enterprises succeed.

According to Bloomberg’s “The fastest growing economies of the world” South Korea is the first (China (3) Malaysia (6), Thailand (11) Philippines (17) and Indonesia (20)). The Korean Government also announced “Plans for Boosting Investments” at the 8th Meeting Promoting Trade and Investment chaired by the President Park in July 2015. The plans are developed to encourage investments in sectors such as tourism, venture, and construction where growths can be accelerated. The presentation can be summarized into six categories and one of it is the ‘Promotion of Venture Entrepreneurship’.

It includes the government’s plan to promote tech entrepreneurship and attract talents to this sector. The government also plans to support M&A and venture investments from the private sector. For example, crowdfunding is officially open for Korean startups. Korea’s National Assembly passed a package of economic stimulus bills, including one that makes crowdfunding and crowdfunding websites legal in Korea. There are several interesting fintech Korean startups already exist and successful.

Japanese e-commerce giant Rakuten launched $100 million global fund for fintech startups. The fund, and its Managing Partner Oskar Mielczarek de la Miel, already have been busy doing deals for some time — including a $12 million Series B round for Latin America-based Uber rival Cabify, a Series C for UK-based Currency Cloud, and bitcoin enabler Bitnet. Rakuten already runs Rakuten Ventures, a $100 million fund that invests across a range of verticals, but now it is literally doubling down on finance. Rakuten Ventures has done most of its deals in Asia but it is global in scope.

The fintech fund, however, is more focused on Western markets, with plans to follow-on and invest in portfolio companies as well as find and back new mid-stage startups. “While the fund’s immediate focus will be on companies based in fintech centers such as London, San Francisco, New York and Berlin, Rakuten FinTech Fund plans to gradually expand operations around the globe,” Rakuten added.

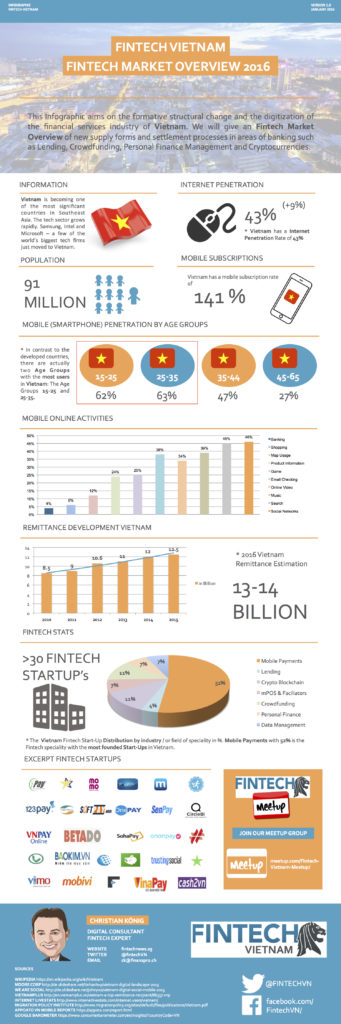

For almost a decade, Vietnam’s startup scene has faced shortage of quality startups, lack of legal support and inadequate funding. All this is set to change with a new wave of entrepreneurs and investors re-shaping the country’s startup ecosystem. Several changes were already visible during Techfest, the first national event for startups. Fintech ecosystem of Vietnam also started to grow.

In the Philippines, the government launched an initiative to create a single electronic payments platform for all transactions in the country. Dubbed the e-peso, the platform is envisioned to be a B2B, B2C, and C2C system for epayments. The initiative is part of a bilateral agreement between the Philippine and US governments. The USAID has awarded a US$25 million, five-year project to a company called Chemonics to support the Philippine government in the promotion and adoption of epayments in the Philippines.

The overarching goal, really, is simple: to eliminate, if not substantially reduce, the use of cash in financial transactions; turning the Philippines into a “cash-lite” economy within 20 years. Here’s the problem with the use of cash: it’s inefficient, costly, and can be dangerous for consumers and businesses. “Long queues, long distance traveling, and time wasting characterize the predominant payment for goods and services in the Philippines, as elsewhere in developing countries. The opportunity cost of using cash versus electronic means has real economic consequences, in terms of lost business activities and overall economic development,” says USAID in the draft statement of work for the ambitious project.

The USAID says epayments will also allow for the poor and unbanked to participate more broadly in the formal economy. “The poor benefit from too few financial instruments to manage their low, uneven cashflows. As such, epayment systems have the potential to help the Philippines reach development goals faster and make those gains sustainable.” It states that only 26 percent of Filipinos enjoy access to formal financial channels, and 610 out of 1,635 municipalities in the Philippines do not have banks. Moreover, as much as one‐half of mobile users in the Philippines are unbanked.

But on the other hand, it’s also true that Filipinos spend a bigger chunk of their lives online: the Philippines has the eighth largest base of Facebook users in the world, one of the reasons why it is touted as the world’s social media capital. And smartphone penetration is predicted to grow fast from 25 percent of the population to 50 percent by 2017. Because of high mobile penetration, the Philippines leads Southeast Asia in mobile phone payments, some reports claim. Taking all these into account, consumer readiness for digital payments in general is there.

Ralph Santos, founder of fintech startup VMoney, shares the same view. “Filipinos are tech savvy already. They love technology, they love gadgets, they love using it. They’re very open to modern methods, if you’ll look at what has happened in the last five years. They’re using technology for transactions. They use it to send money to each other. But it’s on a personal basis. Now we should allow for a holistic solution – borderless, ubiquitous, agnostic.”

The Indian government published proposals to encourage greater take-up of electronic payments in a country where cash still rules. It suggested a range of measures, including tax benefits to merchants if at least half of their transactions are handled electronically. Consumers could also receive income tax rebates if a certain proportion of their spend is cashless. Another idea is for government itself to drop certain surcharges it levies for making card payments.

The Indian government published proposals to encourage greater take-up of electronic payments in a country where cash still rules. It suggested a range of measures, including tax benefits to merchants if at least half of their transactions are handled electronically. Consumers could also receive income tax rebates if a certain proportion of their spend is cashless. Another idea is for government itself to drop certain surcharges it levies for making card payments.

As well as encouraging users to make electronic payments, the government wants more means to accept such transactions. It would like greater deployment of POS\mPOS- terminals, which represent only a small percentage of total debit/credit cards in circulation. In addition, leading operators Bharti Airtel and Vodafone, as well as newcomer Reliance Jio Infocomm, will also look to take advantage. Earlier this year, Vodafone, Idea Cellular and Reliance Industries all applied to become so-called payments banks — cutdown versions of traditional banks which the Indian government hopes will boost financial inclusion.

India will pass U.S. to become world’s second largest smartphone market by 2017. The rise of e-commerce in India has triggered a wave of startups that are leveraging the increasing adoption of smartphones to provide mobile payment solutions. Alibaba invested in Paytm at an apparent billion dollar valuation earlier this year, and now MobiKwik is the latest to be flushed with new cash. New Delhi-based MobiKwik has pulled $25 million in funding, led by Singapore-based hedge fund Tree Line Asia. The deal included participation from a couple of interesting strategic investors — Cisco and American Express. Existing investor Sequoia Capital was also in the heavy-hitting Series B round. MobiKwik raised a $5 million Series A in 2013, and it is targeting a $100 million Series C which it aims to complete in the second half of this year.

The Indian e-commerce market has a new superhero — cashback. Move over discounts, cashback is the hottest new trend in business. Cashback is the newest trend to rock the entire Indian e-commerce game. Big players, emerging players, almost everybody in the e-commerce niche is embracing cashback culture, compelled by thick audience demand, surging market competition and latest funding rounds. It remains to be seen if the new fad stays strong in the long run or fizzes out in an industry that has been enveloped with deep discounting since its inception. Indian women online shoppers in the age bracket of 18-24 are the most active and comprise of 52 % as compared to 20 percent between the age group of 25-34, 6% above the age of 34 and 2% less than the age of 18 years. On an average, most of the women prefer shopping online between 9 – 11 pm that too on Mondays and Fridays. Also, 80% women prefer Cash on Delivery payment option while only 20% opt for online transactions, said the survey. Also India now Uber’s second largest market. Consumer Internet continues to lead in India – fintech the next big wave.

The runaway success of mobile money products like M-Pesa, which first took off in Kenya, has inspired dozens of copycats around the world. Many countries in Africa, Asia, and Latin America now have services allowing people to store and transfer money using their cellphones. But there’s something different about Ecuador’s new Sistema de Dinero Electrónico. It’s being operated not by a private phone carrier or financial company, but Ecuador’s left-leaning government. Diego Martinez, an economist in Ecuador’s central bank, says the government wanted its own service, because it thinks it can reduce the transaction costs that come with private offerings.

“We did it from the government because we wanted it to be a democratic product. In any other countries, it is provided by private companies, and it is expensive. There are barriers to entry, like [expensive fees] if you transfer money from one cellphone operator to another. What we have here is something everyone can use regardless of the operator they are using,” he says.

Under the program, anyone can walk into a participating bank and exchange their cash for electronic money that is stored on their phone. They can then use that to make payments to other people or to buy goods and services. For example, taxi drivers in the country’s capital, Quito, accept payments through the system.

In theory, it would be possible for countries to completely rid themselves of cash and all the disadvantages that go with it. But Martinez thinks it will be decades before that happens in Ecuador, because cash still accounts for about 40% of payments and use of cash among the poor, particularly in rural communities, is high. Whether Dinero Electrónico ultimately takes off will depend on whether banks or other agents agree to covert cash, and whether people have places where they can use digital money. Despite the success of M-Pesa, many mobile money systems haven’t grown as dynamicallybecause people either haven’t seen the benefits or they’ve been wary of moving away from cash. As with any financial product, the decisive factor isn’t necessarily technology. It’s whether people trust it.

Tunisia may to be the first country in the world to issue its national currency via advanced Blockchain technology according to Monetas CEO Johann. Today more than 3 million Tunisians are excluded from the financial system, but more than 600,000 are already using the official digital eDinar. With the La Poste Tunisienne app powered by Monetas, eDinar will be used to make instant mobile money transfers, pay for goods and services online and in person, send remittances, pay bills, manage official government identification documents, and more.

Total transaction fees will be of negligible cost, even from amounts less than a fraction of a dinar, and in most cases fees are paid by merchants. The maximum fee paid on a transaction will be less that 1 dinar. La Poste Tunisienne will strictly control the issuance and circulation of the eDinar in order to prevent it from being used for illegal transactions. “Tunisia is the first country to use Monetas technology and we are currently working with several African partners to provide coverage to 12 markets in 2016. These partnerships will bring more than 300 million people into an incredible future of financial inclusion.”

Photos: Getty, shutterstock

Life.SREDA VC is a global fintech-focused Venture Capital fund with HQ in Singapore

{kind=link}

{kind=link}

{kind=link}